Enterprise Risk Management

Population Health Management: Opportunities and Challenges for Captives

Published

December 5, 2018

2:16 pm

|

Updated

December 18, 2024

4:52 pm

To succeed with population health management, a provider organization must fully understand the risks involved and take strong steps to mitigate that risk, which can include forming a captive health plan and obtaining reinsurance to protect it against catastrophic loss.

Many healthcare provider organizations are responding to the industry’s shift to value-based payment by undertaking population health management (PHM) initiatives in which the focus is on coordinating and managing medical care delivery to a defined population to improve clinical outcomes at a lower cost of care. One of the most prominent aspects of this trend is providers’ widespread development of accountable care organizations (ACOs), characterized by a payment and care delivery model that seeks to tie provider payment to quality metrics for the designated patient population.

PHM poses unique risks that have prompted the provider organizations to form their own, internal health plans, termed captives, to provide coverage for those risks. These captives are presented with both opportunities and challenges in this evolving healthcare environment.

Core Competencies

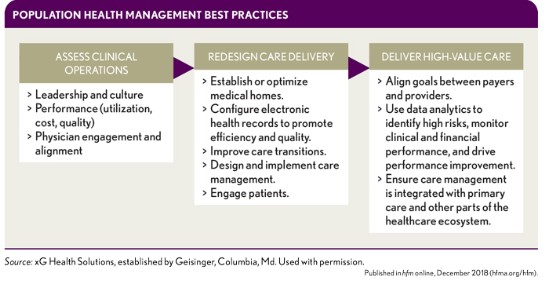

To accomplish what is increasingly referred to as the quadruple aim of healthcare reform—which adds an improved work environment for providers to the much-cited triple aim of improved health, better patient experience, lower costs of care—providers engaged in PHM require key health plan competencies that include the abilities to identify and stratify health risk and to deliver of care in lowest-cost setting that yields high-quality outcomes with a focus on prevention and outreach. Care redesign for PHM should be focused on improving chronic disease management and providing better care management across the full care continuum. The steps required for this transformation are depicted in the flow chart at left.

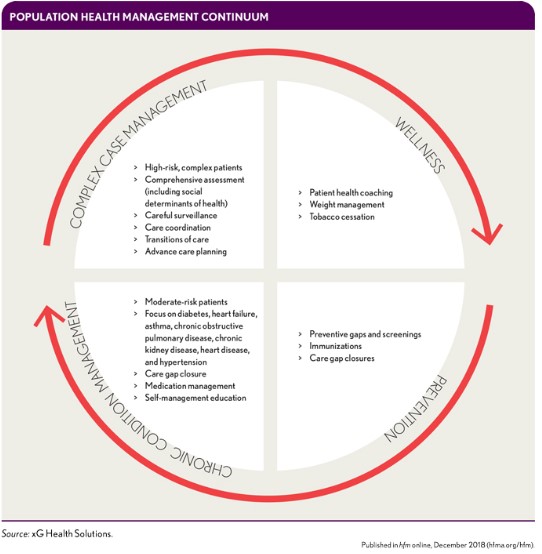

Executing a successful PHM managed care continuum cycles through four ongoing phases, as shown in the exhibit below left.

This quality-assurance care model is customized for given populations based on the nature of the value-based payment contract, the interventions needed to drive contract performance, and the current state of the physician practice operations. It is further personalized for patients based on their disease states, utilization patterns and risk factors, goals and readiness for change, and socioeconomic factors and family situations. An effective PHM model gives providers strong incentives to address gaps in care and to use quality metrics when doing so.

A health system with a captive for PHM does not have to go it alone. Many health plans that take on population health risk look to partners for a wide variety of managed care programs and services with the goals of mitigating claim severity and frequency while providing high-quality, cost-effective health care to the designated population of insured members. Such partners can supplement and complement a health plan’s programs and services in a broad range of areas, including the services listed in the sidebar below.

Many of these services help providers manage certain types of claims (e.g., cancer, neonatal, transplant). Others are designed to review the cost-effectiveness of care (e.g., bill review or national preferred provider “wrap” network). And still other value-added services relate to medical management program protocols and training needs (e.g., operations evaluations or benchmarks). Important objectives of services include positive identification of all potential high-dollar catastrophic cases, verification of diagnoses, validation of treatment plans, and comparative review of costs.

The Nature of Risk Under PHM

Where there is potential reward, there is risk. Value-based provider agreements can entail three basic types of risk:

- Contract risk, which can adversely affect the provider if the contract structure and pricing targets are not in line with the actual costs for in- or out-of-network services for the covered population.

- Performance risk, which a provider can incur if the ACO falls short of the quality metrics, clinical efficiencies, and cost controls outlined in the provider agreements covering the assumed population.

- Insurance risk, stemming from random claim fluctuation for both severity and frequency of claims in or out of network for the assumed population.

There are numerous ways in which a provider organization can prepare a newly formed or previously existing captive to participate in assuming PHM risks. Two approaches are most common:

- Reinsuring a licensed health plan (e.g., HMO)

- Expanding the captive’s traditional lines to cover the ACO via provider excess specific and/or aggregate coverage for participation as a Next Generation or Medicare Shared Savings Program ACO.

A new area of emphasis for provider-owned captives is to write the specific and aggregate stop-loss coverage on the self-funded employer health plan benefits for employees and their dependents.

Unbundled risk services for captives include of the following:

- Providing fronting services that allow a risk-bearing entity to cede risk to the captive via insurance policy or reinsurance treaty

- Appropriately pricing and underwriting stop loss coverage on medical risks placed into the captive

- Evaluating the actuarial adequacy and pricing of stop loss coverage provided through ACO contracts

- Providing medical case management support for excess medical risks on large claims inside or that leak outside a health plan’s contracted provider network

- Calculating premiums and executing billing

- Adjudicating claims

- Issuing insurance or reinsurance for non-retained risk

The Need for and Benefits of Integrated Healthcare Risk Management

Hospital and physician value-based payment models increasingly require practitioners to assume greater financial risk for managing their patients’ care, and the growth of these models has been a major driving factor in increased adoption of captive insurance plans and reinsurance of those plans by healthcare providers. This trend also has been fueled by numerous perceived benefits from such a strategy, some of which are listed in the sidebar below.

Risk contracting has been shown to reduce costs and improve the quality of care, but catastrophic claims can undermine the long-term viability of providers’ value-based agreements and threaten the financial solvency of their organizations. Consequently, health plans or contracted providers often need excess-of-loss protection for catastrophic medical risks. If the health plan or provider organization takes an enterprisewide view of risk, its insurance/reinsurance carrier should do so as well, thereby affording the health plan or provider early access to integrated and coordinated product offerings. The insurance and reinsurance company Zurich North America cites the following advantages of such integrated healthcare risk management: a

- Reduced losses as a result of ongoing communication

- Flexibility for sharing among different lines of business

- Potential for reduced coverage gaps and lapses

- Ability to allocate risk engineering/loss control service budget dollars to the points where they are most needed

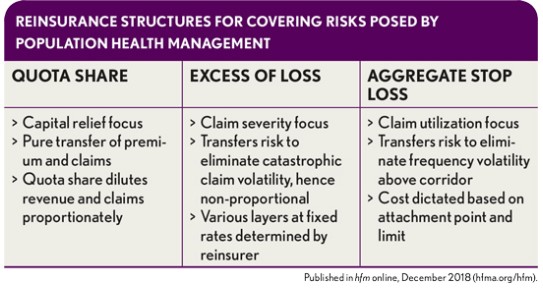

Three common reinsurance structures for covering PHM risks by type, motivation, and financial impact are shown in the exhibit below.

A quota share coverage makes the provider entity and the reinsurer partners in risk on all individual member claims, large or small.

An excess of loss coverage leaves the risk for smaller claims with the provider entity and shifts the risk to the reinsurer only for large claims per individual member.

An aggregate stop-loss coverage is not concerned with large or small claims per individual member; rather, it is focused on whether the utilization of the total membership exceeds some threshold of expected claims (e.g., 125%). Even in a situation where one individual member has a large claim but the experience in the aggregate is still reasonable would the individual large claim not be reimbursed.

Quota share and excess of loss coverages provide protection for claim severity per individual member, often referred to as vertical risk. The aggregate stop-loss coverage focuses on frequency of claims for the group, and often is referred to as horizontal risk.

Case Examples

Reinsurance can be designed to provide claims savings by reviewing certain billed charges by type prior to payment. Billed charges thresholds may vary by claim type. For example, the threshold for inpatient care might amount to $100,000 per stay, whereas the thresholds for outpatient and pharmacy might be $25,000 and $50,000 per month, respectively.

The coinsurance payment provided by the reinsurer varies (plus or minus 10 percent) depending on whether the health plan submits large bills above these thresholds for prepayment review and follows the recommendations of the bill review vendor. Some health plans also receive a reinsurance premium discount for the chosen plan design and compliance with appropriate claim review levels and protocols. Hence, the reward to the provider group for having bills reviewed in advance of paying them to make sure they are appropriate can be found in the form of increased reinsurance claim payment (i.e., higher coinsurance) and/or a discount on the monthly premium rate charges to the provider group for such coverage. It is much more difficult to save money on claims after the provider has been paid for its services because the health plan assuming the risk has more leverage if it hasn’t made payment yet. The author acknowledges that the health plan provider may also be the reinsurer up to some level for the amount of risk retained in the captive. However, reinsurance should be structured only to cover random and unpredictable claims that constitute appropriate charges according to the reinsurance contract and medical service protocols (e.g., medically necessary, nonexperimental, and appropriate coding of the claim).

These savings can inure to the first-dollar claims costs as well as the catastrophic claims costs.

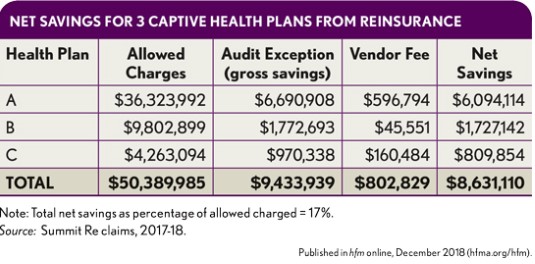

The exhibit at left shows net savings for three actual captive health plans under PHM initiatives with reinsurance coverage requiring prepayment review.

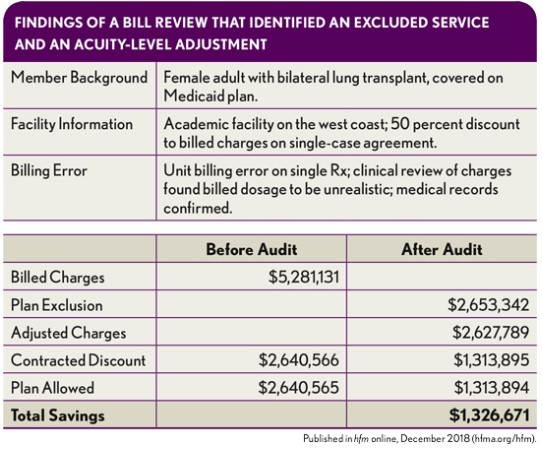

To illustrate how savings are identified at the level of an individual claim, consider the exhibit below. Specialty pharmaceuticals are among the major culprits behind the dramatic increase in catastrophic claims. These pharmaceuticals include the well-known “factor drugs” associated with treatment of hemophilia and new biosimilar drugs, breakthrough therapies, and orphan drugs. In this situation, the number of units billed was not consistent with the actual standard of care and actual illness and treatment plan.

Conclusion

With the shift to value-based payment and the creation of ACOs, prompted in large part by the Affordable Care Act, PHM has emerged as a critically important and expanding form of managed care. Yet PHM also imposes increased medical risk on provider organizations that it is incumbent on them to address in to ensure their ongoing financial solvency. The best way for organizations to mitigate that risk is through effective PHM processes and care coordination that are protected from catastrophic loss via insurance or reinsurance.

Footnotes

a. Zurich North America, “Zurich Integrated Healthcare Approach: Infographic,” Sept. 1, 2015.