Why hospitals should develop a billable supply policy

By following a clearly outlined policy that specifies when medical supplies can or cannot be separately billed, a hospital can achieve efficiencies that otherwise are often out of reach for organizations.

The question of how best to charge and bill medical supplies to insurers has long been fraught with uncertainty for U.S. healthcare providers. The uncertainty arose from the decision by Congress in 1983 to implement the inpatient prospective payment system (IPPS) and, in 2000, the outpatient prospective payment system (OPPS), with the goal of controlling Medicare costs by moving payment away from a cost-based to a fee-for-service (or episodic) payment methodology.

This shift created a significant challenge for hospitals and health systems. Previously, they had been able to charge individually for all medical supplies based on separate charges listed in the chargemaster, regardless of cost. But under IPPS and OPPS payments, a hospital’s payment to cover the cost and expense for medical supplies is often packaged into the larger, procedure-based payment, creating a challenge for the hospital in being able to track whether and to what extent this cost and expense is covered by the larger payment.a

The need for a billable supply policy

To effectively address this challenge, hospitals need a clearly defined billable supply policy that enables them to determine which supplies are routine versus which are not and are therefore separately billable.

Such a policy can alleviate confusion among the staff who are responsible for ensuring medical supplies are charged to the patient’s account, when appropriate.

Confusion can arise, for example, among hospitals and other large organizations that use a unit cost threshold to account for routine items and supplies, which can have an impact on their charging practices. This cost threshold addresses only low-cost items — typically ranging in price from $0.01 to $25 and packaged by the manufacturer as a bulk supply. These typically are supplies readily available across the hospital on floors/units and found in department closets. Having such a policy means the costs of all other items exceeding the threshold are deemed billable. But it is not necessarily so simple.

Case example: Ambiguity about when a supply should be billed separately

Consider, for example, the case of indwelling foley catheters (IFCs). A physician typically will order an IFC for toileting management of a bed-bound patient or for a patient who is experiencing urinary incontinence for a specific condition.

Depending on the manufacturer’s IFC packaging, the unit cost can range from $1.99 to over $50. If the hospital’s threshold policy is set at a maximum unit cost of $25, any IFC costing less than $24.99 does not get separately billed. The patient receiving an IFC that meets the cost threshold does not see a separate charge on their hospital account. However, another patient receiving an indwelling catheter costing more than $25 will be charged for the same type of supply that has been marked up using the hospital’s mark-up policy. Thus, one patient gets charged separately for use of an IFC and the other does not.

Using the unit cost threshold methodology therefore does not ensure all patients will be charged the same because, as the above example shows, one patient is charged only the room-and-board rate while the other patient is charged room and board plus the charge for the IFC. Meanwhile, the hospital’s reimbursement team must determine the best practice for reasonably setting rates for room and board, procedures and services that include the costs of routine items and supplies purchased and packaged in bulk.

Limited guidance on billable supplies from CMS and others

CMS and other nationally recognized organizations do not provide specific guidance on determining what is a billable supply, nor do they provide any list of billable supplies. Individual payers have published their own coverage policies using the language found in the CMS Provider Reimbursement Manual (PRM).b Some payers have gone as far as hiring external auditors to help recoup payments made to hospitals, citing the PRM and claiming the payments for items or services are routine and that the hospitals were overpaid based on the payer’s interpretation of the manual language.

Meanwhile, CMS has been consistent in its directive that hospitals should report their charges under the revenue code that will ensure the charges are assigned to the same cost center to which the service costs are assigned in the cost report. (See the sidebar at the end of this article for details on CMS’s directive regarding billable supplies.)

How to develop a billable supply policy

Key steps and considerations for hospitals in developing such a policy include the following.

1 Assemble a team of individuals who are knowledgeable about the organization’s charge capture practices. The team should include, at minimum, staff from materials management, nursing, operating/surgical and reimbursement. The team also should include a revenue integrity expert who preferably has coding and billing expertise and/or clinical background.

The team should begin its work by reviewing all existing and current CMS guidance and gather and review payer policies and contracts where the payer has defined what is and is not separately billable.

2 Create supply categories with a specific definition based on the CMS and/or payer policy language. The dedicated team will need to participate in defining the categories and creating the definitions, because these individuals will later support others across the organization in determining which medical supply will be separately billed.

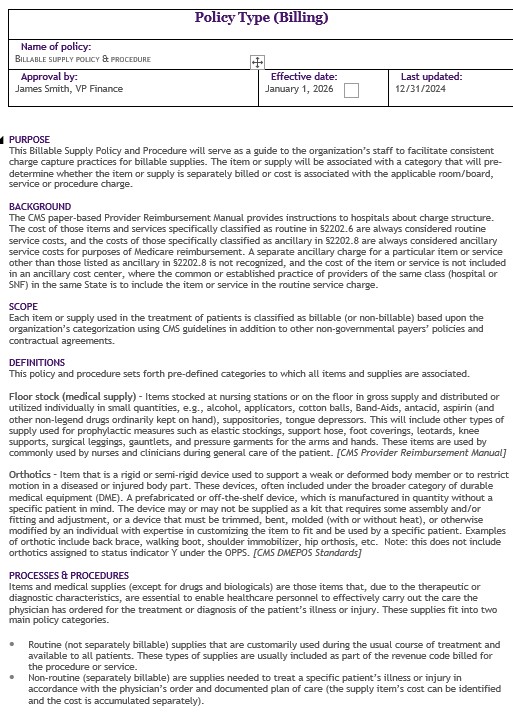

The number of categories should encapsulate all medical supplies, devices, implants and even minor equipment and associated supplies used by the organization. Examples of defined categories created with hospitals, for example, include floor stock, incontinence care, personal care, surgical device, implant, orthotics, personal protective equipment, kits and wound care supply.

3 Create a decision tree in which each of these categories is listed as not separately billable and separately billable. Under these categories, items or supplies that are not separately billable are identified as being routine, while those that are separately billable are designated as non-routine. See the exhibit below for a sample list.

Examples of supply items typically listed as not separately billable and separately billable

| Not separately billable (routine) | Separately billable (non-routine) |

|---|---|

| Floor stock (medical supply) IV supplies Incontinence care Personal care Personnel protective equipment Surgical supply/instrumentation | Implant Surgical device (disposable) Orthotics Wound care supply Reprocessed device |

4 Give special attention to items such as operating room (OR) packs, kits and trays. These types of items require a second-level analysis because they include multiple products specific to the setup and performance of a procedure or service. A key consideration in this analysis for OR packs, kits or trays is determining whether they contain any items that ordinarily fall into the separately billable category. And if they do, the cost of such items should be considered for price setting, despite the inclusion in a kit that contains items that are not separately billable.

5 Outline the billable supply policy in a written document. The written policy should not only clearly outline the previous points and any others deemed important to consider, but also include measures that ensure the hospital’s charge capture practices follow CMS regulatory guidance and third-party payer policy specifics. (See the end of this article for a sample formalized billable supply policy.)

Regarding CMS guidance, the billable supply policy should include the use of revenue code assignments based on finalized billable categories, as well as the application of HCPCS codes where necessary. Having pre-defined revenue codes and eligible HCPCS code(s) for the categories ensures consistency of the hospital’s efforts for billing items and supplies that are separately billable.c

The policy also should account for coding guidance from the Medicare Claims Processing Manual, Chapter 4, Section 60.4.3, to enable the hospital’s reimbursement and finance leadership to more easily account for the separately billable items in third-party contract negotiations.

6 Integrate specific payer requirements regarding medical supplies into the supply policy. Third-party and nongovernmental payers continue to expand on policies for medical supply coding and billing. In addition to relying on their own interpretation for what is considered routine, payers are beginning to require hospitals to submit HCPCS codes for supplies individually billed with revenue codes 270, 271 and 272 (medical/surgical supplies and devices).

Based on such payer trends, it is important that the policy consider the more restrictive payer coding and billing policies so that charge capture practices will be consistent across the entire organization, with few charge capture exceptions for payer-specific payment purposes.

Going forward, the hospital’s billable supply policy may require slight modifications to account for payer denials where the payer contract language or policy may not have sufficiently defined the status of certain items. Any material coding and billing changes may also need to be implemented later in the payer contract to minimize the impact on the hospital’s expected payments.

7 Educate all stakeholders within the hospital on the billable supply policy. Once the newly created billable supply policy has been reviewed and approved by the hospital’s reimbursement and financial leadership, staff in all applicable areas of the hospital will need to be educated on the policy. Specifically, patient financial services staff (and revenue integrity staff, if applicable) should also be informed of the need to escalate payer denials for supplies so that reimbursement and finance leaders can adjust payer contracts and pricing for room and board or procedures, where applicable.

8 Evaluate charge capture practices after the policy has been implemented. After the policy has been fully implemented, the hospital should perform a comprehensive evaluation using the supply categories to calculate the annual revenue currently being charged for the non-billable items. The hospital’s reimbursement and finance leaders should evaluate this revenue to determine where the costs and expenses need to be allocated (e.g., room and board, specific procedures, OR time charges). This effort may require adjusting prices for these items and services to account for potential revenue loss and determine how any pricing impacts payer reimbursements. Following is a sample routine supply analysis.

Sample analysis of routine supplies under revenue code 272 that are not separately billable to patients

| Item description | Revenue code | Item/unit cost | Price | Total annualized quantity | Total annualized costs | Total annualized charges |

|---|---|---|---|---|---|---|

| Arthroscopy tubing | 272 | $116.69 | $368.00 | 89 | $10,385.58 | $31,569.00 |

| Drape, custom eye drape | 272 | $184.33 | $581.00 | 128 | $23,594.67 | $71,512.00 |

| Neptune manifold | 272 | $20.67 | $66.00 | 837 | $17,298.00 | $52,750.00 |

| Surgilav irrigation system | 272 | $58.37 | $184.00 | 63 | $3,677.05 | $11,227.00 |

| Surgiwand irrigation system | 272 | $113.33 | $357.00 | 60 | $6,800.00 | $20,587.00 |

| Tourniquet | 272 | $43.33 | $137.00 | 102 | $4,420.00 | $13,463.00 |

| Tubing, CO2 with filter | 272 | $60.00 | $180.00 | 78 | $4,680.00 | $13,455.00 |

| Totals | 1,357 | $70,855.30 | $214,563.00 |

3 benefits of a supply policy

A billable supply policy offers the following primary benefits:

- Better informed healthcare teams and less confusion about what the hospital organization considers billable

- Consistent charge capture practices for separately billable items and ease of charge reconciliation

- More useful data for the reimbursement and financial leadership teams in preparing for contract negotiations, including costs of routine items in setting charges for room and board, ancillary services and procedures

A billable supply policy as a living document

Hospitals should review their billable supply policies annually and update them, as necessary, to account for changes in payer coverage policy and/or CMS guidance. The reimbursement and financial leadership team should be kept informed of material changes and asked to provide input on the changes because of their possible impact on the hospital’s reimbursement based on current (or existing) payer contracts.

It also is important to provide continuing education to staff responsible for billable supply charge capture and to consistently provide comprehensive education on the policy to newly onboarded staff.

Footnotes

a. Notably, in 2015, under the OPPS, CMS implemented a subset of its ambulatory payment classifications (APCs) called comprehensive APCs (C-APCs) “to consolidate payment for the highest cost device dependent procedures into a single, global prospective payment rather than paying separate single APC payments for each component of the procedure.” See CMS, Medicare Fee-For Service Provider Utilization & Payment Data Outpatient Hospital Public Use File: A Methodological Overview, November 2020.

b. CMS.gov, The Provider Reimbursement Manual – Part 1, publication No. 15-1.

c. The team should keep in mind that, under the OPPS, CMS has prepared for the C-HCPCS codes an explanation of certain device pass-through category codes.

What CMS has to say about billable supplies

CMS provided clear guidance applicable to billable supplies in its The Provider Reimbursement Manual – Part 1, publication No. 15-1 (PRM).

Chapter 22, Section 2202, of the PRM addresses the establishment of charges. The charge refers to regular rates established by the provider and should be related consistently to the cost of services and uniformly applied to all patients whether inpatient or outpatient.

Chapter 22, Section 2202.6, addresses routine services. Routine inpatient services in a hospital are the s ervices included in the daily charge referred to as the room and board. The routine services included in the regular room are dietary and nursing services, minor medical and surgical supplies and the use of equipment and facilities for which a separate charge is not customarily made.

Chapter 22, Section 2203.1 – Routine Services (SNF) and Section 2203.2 – Ancillary Service (SNF), which refer to services provided in skilled nursing facilities but also apply to hospitals, can assist hospitals in determining if an item is ancillary and can be recognized as a charge.

According to the language in these two sections, the use of the supply or item must meet all three of the following conditions:

- Reflect direct identifiable services to individual patients

- Not be generally furnished to most patients

- Not be reusable

Section 2202.6 of the PRM is reinforced by language found in the current CMS internet-only Medicare Claims Processing Manual, Chapter 4, Section 240 – Inpatient Part B Hospital Services. CMS says nursing services provided by the floor nurse may or may not have a separate charge established depending upon the classification of an item or service as routine or ancillary among providers of the same class in the same state. So, if the provider does not follow the directives in the PRM and the Medicare Claims Processing Manual, the provider cannot bill for these routine services.

The Medicare Claims Processing Manual, Chapter 4, Section 0.4 – Packaging, also provides insight into what is considered routine and included in the outpatient prospective payment system (OPPS) ambulatory payment classification (APC) payments. CMS does not pay separately for items and services designated as packaged (based on the revenue code assignment) because the cost is included in the APC payments. Examples of CMS packaged services under the OPPS are routine supplies, anesthesia, recovery room supplies and most drugs integral to a surgical procedure

Sample billable supply policy