Fast Finance

Not dead: Provider-sponsored plans reassessing

Partnership models may be the best option going forward, says an adviser.

Published

June 8, 2026

12:03 pm

Provider-sponsored health plans (PSHPs) proliferated in recent years and now face a historically challenging market. Some are reassessing, while others are in wait-and-see mode, says an adviser.

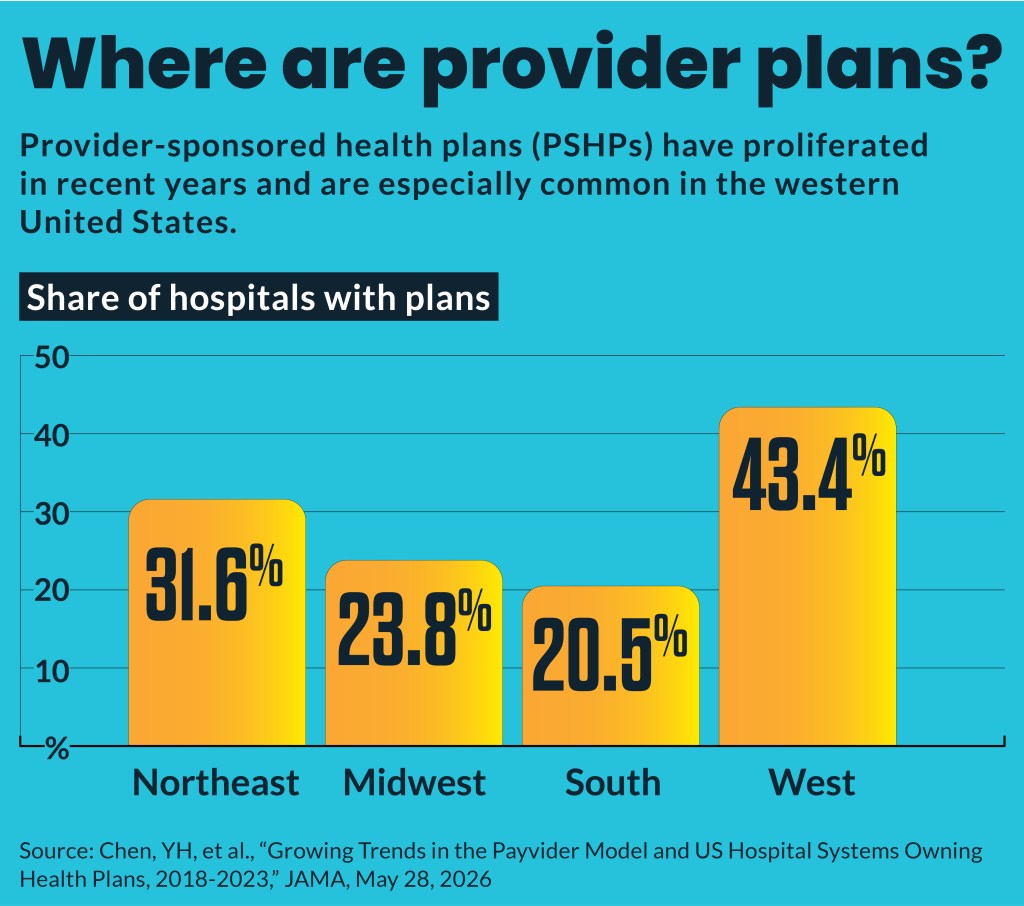

From 2018 through 2023 the number of hospitals owning PSHPs increased from 692 (18.3% of hospitals) to 834 (27.2%), according to a new study published in JAMA by researchers from Massachusetts General Hospital and Harvard Medical School in Boston.

“The most surprising finding for us is that there is a huge increase in the number of healthcare organizations that are also owning health plans,” said David Chang PhD., a co-author and an associate professor of surgery at Mass General, Harvard Medical School. “We notice it with our own institution. Mass General Brigham has a Mass General Brigham Health Plan and we’re surprised to see that this is part of a national trend.”

The growth in PSHPs in those years was concentrated among academic medical centers (AMCs), of which more than 35% have launched health plans, Chang said in an interview.

The share of non-AMC hospitals with health plans “is still going up, but they’re essentially flat,” said Chang. “So, this is a trend that’s happening mostly among medical school-affiliated hospitals.”

Chang said the research did not examine why PSHPs increasingly appeal to AMCs but noted that successful PSHPs can improve the finances of hospitals by eliminating revenue delays under the dominant fee-for-service reimbursement model.

“What this does financially is sort of change out [the revenue process] a little bit so that you can actually have revenue, a little, some revenue before you actually do the work,” Chang said.

Recent struggles

Over the last year, a growing number of PSHPs announced that they were closing or pulling back from various health insurance segments

Those recently announced retreats included:

- Presbyterian Healthcare Services in New Mexico exiting the Medicare Advantage (MA) market

- Providence ending most of its health plans by 2027 and selling its MA plan

- PacificSource, partly owned by Legacy Health in Portland, Oregon, dropping ACA marketplace plans and all plans in Montana

Some of the pullback likely reflects challenges faced by smaller PSHPs, Chang said. “Maybe they are not as viable as some of the larger players.”

It’s possible the PSHPs are retrenching at a new plateau and will refocus on such specific populations as local elderly patients going forward, said Chang.

“The market’s still kind of testing out … how viable this kind of idea is,” Chang said.

Some market observers have said they see signs of hope for PSHPs, even amid the recent retreats. For instance, some highlighted that Presbyterian Healthcare Services will retain its MA Special Needs Plans (SNPs) for dual-eligible Medicare enrollees, even as it exits the broader MA market.

MA enrollment this year increased by about 1 million people, mainly due to higher enrollment in SNPs, according to a KFF report.

Wait or reassess

The current environment is forcing a much harder look at these plans, Craig Savage, managing director for Alvarez & Marsal, said in emailed comments. He noted the PSHP market is not dead, but it is bifurcating.

Only a handful of health systems’ PSHPs have “turned their plans into strategic assets that reinforce their provider enterprises,” noted a December report by Alvarez & Marsal, that Savage authored.

“At the other end of the spectrum is the majority of systems whose PSHPs are subscale, undercapitalized and operationally deficient,” stated the report.

The current plan environment has forced many regional PSHPs to decide whether they have the scale, capital, technology, and regulatory capabilities to remain in the payer business — or whether the plan has become an anchor.

“I think there is still some ‘wait and see’ behavior, but it is becoming much harder to defend,” Savage said.

Fitch Ratings noted in an April report on St. Luke’s health system in Idaho that providers with sizable health plans or shared-risk plans generally have below-average operating EBITDA margins compared with health systems without such coverage.

Ways forward

Wait and see is not neutral — it is active value destruction, said the Alvarez & Marsal report.

“The only real choice is whether to invest, partner, or exit, and the time horizon is measured in months, not decades,” said the report.

The report identified five options based on “capital requirements, reserves freed or frozen, and the impact on days of cash on hand.” Those alternatives are:

- Doubling down with investments in staff

- Joint venturing or outsourcing

- Consolidating with other plans for scale

- Exiting

- Refocusing narrowly on the Employee Retirement Income Security Act’s self-insured plans

The most viable paths for PSHPs today are generally partnership models rather than go-it-alone models, said Savage.

“That could mean a joint venture with an established payer, delegated administration or TPA support, an MSO/shared-services model, a narrow commercial or direct-to-employer product, a centers-of-excellence strategy, or using the employee health plan as a controlled platform to build capabilities,” he said. “Consolidation can also make sense where it helps a plan cross real scale threshold.:

For some systems, however, exit or significant retrenchment is the financially responsible answer, he said.