Fast Finance

ACA plan financial struggles could hit providers

Health systems should expect greater scrutiny of utilization by ACA plans.

Published

June 23, 2026

11:17 am

ACA marketplace plans lost $5.5 billion in 2025 — despite record enrollment and before extra subsidies expired, according to new data. Their course-correction strategies could hit hospitals and health systems.

The individual segment plans suffered a $5.5 billion underwriting loss in 2025, according to an analysis of insurance filings by Mark Farrah Associates. That compared with only a $508 million underwriting loss for plans in the small group market. The five leading ACA plan companies also saw marked deterioration in their medical-loss ratios.

The Mark Farrah findings “show that the individual market was already under real underwriting pressure before the full impact of the enhanced subsidy expiration flowed through,” Craig Savage, managing director and health plans market leader for Alvarez & Marsal, said in emailed comments. “The $5.5 billion underwriting loss is not just a subsidy story. It is a medical-cost, utilization, acuity, risk-pool and pricing story.”

The 2025 losses predated the end of COVID-era extra subsidies provided to ACA marketplace enrollees, which plans partially blamed for financial challenges this year.

Fueling the 2025 losses was an influx of membership from Medicaid redeterminations the previous year, Karan Rustagi, a director for Wakely Consulting Group, said in emailed comments.

“This created a disconnect between what was assumed in pricing for 2025 and what actually happened that year,” said Rustagi. “The losses were driven by misses on assumptions in pricing about claims-cost levels and risk-adjustment transfers leading to a disconnect between premiums and claims/risk-adjustment expenses.”

Those losses — and concerns about more losses in 2026 — resulted in a range of ACA marketplace pullbacks:

- Aetna dropped all ACA marketplace plans at the end of 2025

- Mountain Health Co-Op left Wyoming

- Molina left local markets across multiple states

- BCBS of Arizona terminated its PPO offering

Provider effects

The increased pressure on ACA marketplace plans, said Savage, will show up for providers in three ways: pricing, pruning and policing. Specific actions include:

- Pricing through higher-rate requests where they can

- Pruning through market exits, county-level footprint reductions, narrower networks, more selective contracting and tougher unit-cost negotiations

- Policing their spending through more prior authorization, concurrent review, site-of-care management, specialty pharmacy controls, post-acute management and payment integrity

“Providers should expect more scrutiny of inpatient admissions, high-cost imaging, elective procedures, specialty drugs, length of stay, readmissions, coding documentation, DRG validation, medical necessity and overpayment recovery,” Savage said. “A payer-margin problem quickly will become a provider-administrative and cash-flow problem.”

Wakely Consulting is seeing significant interest from plans for evaluations of their provider contracts and networks to look for opportunities to reduce costs, said Rustagi. Also, plans are looking to add step therapies on expensive drugs and gold carding providers who don’t need prior authorizations on many services.

Savage highlighted the potential of a gold card plus risk-share compact.

“Providers that meet agreed standards on evidence-based pathways, documentation, access, total cost, readmissions and outcomes should receive reduced prior authorization burden,” Savage said. “In exchange, they should accept more accountability through episode budgets, shared savings, downside risk or performance guarantees. That would turn utilization management from an adversarial claims-control process into a targeted performance-management model.”

Continuing pressure

Financial pressure on insurers offering ACA plans continued this year.

The largest ACA plan company, Centene, saw its marketplace enrollment drop by nearly 2 million to reach 3.6 million in Q1. In June, the insurer offered buyouts to most of its 60,000 or so employees.

In April, Baylor Scott & White notified regulators of its intent to discontinue individual marketplace plans, which cover about 100,000 lives, by the end of 2026.

Savage said plans cannot “prior authorize” their way out of a bad risk pool.

“The more constructive path is precision medical management, not blunt denial management,” Savage said. “The best plans will use data, AI-enabled workflows and provider collaboration to focus interventions on high-variation, high-cost and clinically sensitive areas. The worst plans will simply add friction everywhere.”

Utilization hits

When Fitch Ratings issued a “deteriorating” outlook for the U.S. health insurance sector, it highlighted the impact of rising utilization.

“Fitch expects medical cost trends to drive the sector’s weaker operating performance, as utilization has risen due to more costly and frequent provider visits,” Fitch stated. “We expect high behavioral health utilization and rapid growth in specialty pharmacy spending to persist.”

That elevated ACA enrollee utilization has benefited hospitals and health systems. ACA enrollee visits to emergency departments (EDs) and inpatient care had surged past pre-pandemic levels by the end of 2021, according to one study.

Although providers rarely detail site of service for ACA enrollees, Community Health Systems stated that ACA marketplace enrollees mainly use the system’s EDs and often don’t pay their deductibles or co-insurance.

“Utilization is clearly part of the story, but I would not reduce [payer financial pressure] to utilization alone,” said Savage. “Higher acuity, pharmacy trend, provider unit-cost pressure, metal-tier migration, risk-adjustment dynamics and member churn all matter.”

Those utilization patterns mean that any significant shift from ACA marketplace enrollment to uninsured status could provide a double hit to health systems of decreased high-margin utilization and increased bad debt or charity care costs.

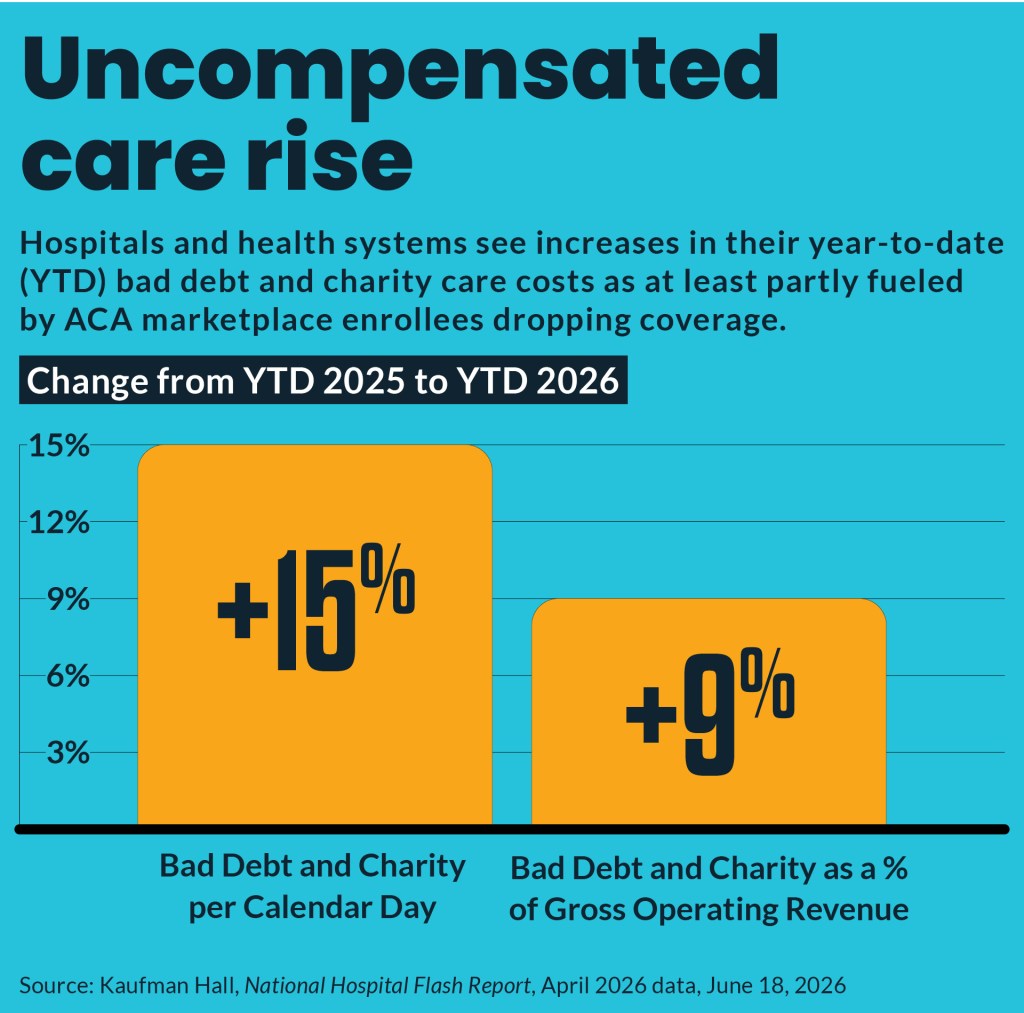

One organization reported to the Washington Post that they have seen a 25% increase in uninsured and self-pay patients. By April, hospitals reported a 15% increase in bad debt and charity care compared with the same year-to-date period in 2025, according to the latest Kaufman Hall National Hospital Flash Report, which uses Strata Decision Technology data for 1,300 hospitals.

“The individual market also matters beyond the ACA exchanges themselves,” Savage said. “It affects providers, because enrollment losses can increase uncompensated care and bad debt.”