Strategic Planning

Why health systems need a hybrid strategy and ambidextrous leadership to ensure financial sustainability

February 26, 2020

6:20 pm

When the Affordable Care Act first began to roll out its programs aimed at encouraging provider organizations to take medical risk from payers and deliver value-based care, many hospitals faced a daunting challenge knowing where to start.

The ACA offered providers opportunities to participate in shared savings programs, bundled payment models and other risk-based programs, and it created a medical loss ratio floor to give health insurers an incentive to shift care management activities to providers. The underlying assumption was that shifting risk from payers to providers would give health systems an incentive to “manage population health” and make care more affordable.[a]

Many health systems’ initial response was to “launch 1,000 ships” by developing accountable care organizations (ACOs), clinically integrated networks (CINs) and other vehicles, hoping that some of them would find safe passage to the new value-based world. Because no amount of business planning could predict which ships would arrive safely, this was a reasonable initial response.

Examples of the “1,000 ships” provider responses to cost and quality pressures from ACA-driven health reform

Types of Initiatives

- Private and public exchanges

- Direct contracting with employers

- Network affiliations

- Narrow and tiered networks

- High-deductible health plans

- Medicare reference pricing

- Centers of exclellence

- Value-based risk contracts

Segments

- Medicaid Temporary Assistance to Needy Families

- Medicare-Medicaid dual eligible

- Medicare fee-for-service

- Medicare Advantage

- Commercial administrative services only

- Commercial, fully insured

- Commercial health insurance exchange and private

Services

- Inpatient

- Outpatient surgery, routine

- Outpatient surgery, specialized

- Outpatient diagnostics, ancillary

- Cancer care

- Clinical rehabilitation

- Emergency department treatment and release

- Transplant

Unique Mission

- Academic research

- Not-for-profit enter

- Private enterprise

- Complexity of cases

- Subsidization of Medicare and Medicaid

- Payer-broker-employer-consumer dynamics

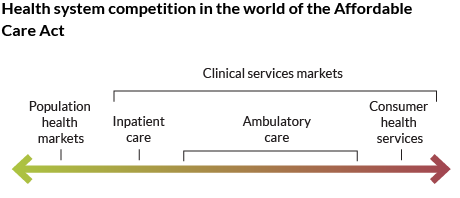

At the same time the ACA was pushing health systems to pursue population health management, many clinical services markets (e.g., ambulatory care) were being disrupted by new competitors and rapid technological change. The effect of these combined trends was to force provider systems to compete in a much more complex set of inter-related markets, as shown in the exhibit below.

Health systems have little choice but to compete across the board; ignoring any one market would create vulnerabilities in the others. As a result, health systems now compete with each other for inpatient admissions and ambulatory care, with each other and with insurers for members, and with each other and a wide range of companies for other clinical services (including insurers, many of which now employ physicians).

Given this complexity, and facing tighter margins, health systems can no longer afford to launch more ships. They need coherent and effective hybrid “strategies for the middle” that can generate reasonable ROIs, and leadership flexible and skilled enough to play in a variety of different markets.[b] What makes this challenging is that the different markets shown in the previous exhibit require fundamentally different approaches to strategy development and implementation.

Competing in inpatient markets

Inpatient markets are traditional markets that health systems understand well. Inpatient care is subject to substantial economies of scale, and barriers to entry are high. As secondary care moves to the outpatient setting, inpatient care has become focused on the most acute conditions, and volumes (numbers of discharges, patient days) have declined dramatically. Under these conditions, health systems must concentrate on building sustainable competitive advantage, and consolidation is a proven strategy for accomplishing this purpose, as discussed in the sidebar, “Inpatient market consolidation has led to stable inpatient markets in metro areas.”[c]

Competing in population health markets

Like inpatient markets, markets for population health are governed by traditional competitive rules. The principal players in these markets are health insurers, which are paid 10% to 20% of total healthcare costs to manage the quality and cost of healthcare services. Competing for members is their main way of growing revenue. Relationships between members and insurers involve substantial switching costs, making health plan purchasing decisions sticky, and creating long-term value for customer relationships. Market share matters because large insurers can negotiate lower rates with providers and gain a cost advantage over smaller insurers. As a result, like inpatient markets, barriers to entry are high.

Building sustainable competitive advantage in population health markets requires a variety of competencies, including plan design, pricing, provider network contracting, claims processing, member services and cost management. Scale is also critical, and since the 1980s, the market for managing population health has been consolidating rapidly. Based on Fortune’s most recent “Fortune 500″ list, two health insurers (United HealthGroup and CVS Health) are now among the 10 largest public U.S. corporations, each with more than $200 billion in annual revenue.[d]

Health insurers have a significant advantage over health systems in markets for population health, because they contract at scale with multiple providers to deliver a wide range of services across broad geographies. Health systems that own insurance products and employ physicians who can manage the quality and cost of care, like Kaiser Permanente and Geisinger, can compete successfully, but these skills take a long time to develop. Health systems that don’t market insurance products directly to employers or individuals must have contractual relationships with insurers, raising questions about whose “member” a given person or family is — the insurer’s or the provider’s.

As a result, despite all the ACA programs, relatively few health systems are competing vigorously in population health markets to date. Most health systems remain heavily dependent on fee-for-service revenue, taking little financial risk. In a recent profile of the not-for-profit and public health sectors, Moody’s Investor Service found that only 3.7% of the revenue of 284 freestanding hospitals and provider systems in 2018 was truly risk-based, up from 3.0% in 2014.[e]

Competing in emerging clinical services markets

In contrast to inpatient and population health markets, most other clinical services markets are local, fragmented and chaotic. Barriers to entry are low, and as a result, new cross-sector competitors are emerging all the time. Building sustainable competitive advantage is challenging in chaotic markets. Professor Rita Gunther McGrath of Columbia Business School describes an approach to strategy development that may suit these markets better, which she calls building “transient advantage.”[f]

Building transient advantage requires scaling new business initiatives rapidly, managing short product life cycles to maximize near-term benefits and unsentimentally disinvesting when life cycles start trending down. Success requires a portfolio manager’s mindset of making good short-term bets, maximizing benefits from investments, getting in and out at the right time and moving on. Building transient advantage does not replace traditional concepts of business strategy, but it does have different rules of engagement. Some of the most important are the following.

1. Pick the right areas for investment. The most fertile areas are those that meet immediate needs of healthcare consumers and/or purchasers (“customer experiences and solutions”). [g] Go-to-market initiatives – new retail care delivery vehicles, new risk contracts with employers, etc. – are less risky and more productive than projects requiring large, expensive infrastructure.

2. Choose champions wisely. Introducing new products is an entrepreneurial activity, and provider systems need internal leaders with an entrepreneurial mindset to champion key initiatives. Independent physicians with business acumen often make good champions, because they interact in the marketplace every day. Clinical investigators also can make good champions because they compete in fast-moving, highly competitive markets for ideas.

3. Give champions the tools and support they need for success. Entrepreneurial project leaders need clear accountability, relevant metrics and appropriate incentives, both carrots and sticks, to guide their efforts. Incremental revenue is a useful metric for champions and the executives managing them.

4. Create internal sponsorship. Champions need sponsors. In external capital markets, venture capitalists with direct financial stakes in the success of entrepreneurs play this role. In health systems, this role can be played by chief innovation or transformation officers or leaders of internal venture funds. Providing release time and seed funding, candid advice and counsel and protection from traditional organizational processes (e.g., budgets) is essential to cultivating successful “intrapreneurs.”[h]

5. Promote small initial investments and condition future investments on success. Innovative companies adopt an incrementalist philosophy of business development, captured by 3M’s motto, “Make a little. Sell a little. Make a little more.”[i] Because the risk is great, initial investments should be limited until initiatives prove they have legs.

6. Encourage partnering. Because emerging markets are dynamic, solo plays are relatively high risk. Partnering with other companies with similar goals but different skills and networks — e.g., supplier companies or co-investors — is a much less risky strategy.

7. Exploit business interdependencies. In many cases, ambulatory and consumer initiatives may not move the revenue or profitability needle much on their own. But they may enhance other businesses. Remote patient monitoring, for example, while unlikely to generate much revenue, may enable health systems to react quickly to changing patient conditions and provide other services that improve outcomes and generate incremental revenue.

8. Build innovative cultures. Innovative cultures are characterized by a certain set of values, starting with an emphasis on sales and growth. Innovative companies value experimentation and adopt an ethos that celebrates blockbuster successes but doesn’t penalize good tries that fail.

The need for ambidextrous leadership

Straddling traditional and emerging markets is challenging, requiring substantial investments in people, facilities and systems. One organizing strategy that some health systems have implemented is creating separate operating divisions to address these different markets — e.g., an ambulatory division separate from an inpatient division. Most provider systems that own large health plans — like Intermountain Healthcare in Utah, Henry Ford Health System in Michigan and Sentara Healthcare in Virginia — manage their health plans separately from their delivery systems. Of course, creating separate divisions focused on different markets raises the question of how common activities like care management should be integrated across divisions.

At the corporate level, implementing different strategies requires ambidextrous leaders who can balance the needs of diverse businesses and cultivate diverse leadership teams. Finally, scale and resources are essential to success, and vertical and horizontal consolidation is creating the large, capable health systems required to compete in this complex, chaotic world.

Footnotes

[a] The Affordable Care Act set maximum medical loss ratios that health insurers can earn on their insurance products, limiting their administrative costs and profits.

[b] Eggbeer, B., Wesslund R., Weylandt, S., “It’s not so simple: Why provider organizations need a ‘strategy for the middle,'” hfm, December 2016.

[c] Porter, M.E., Competitive Advantage: Creating and Sustaining Superior Performance, New York, The Free Press, 1985.

[d] “2019 Fortune 500,” Fortune, 2019.

[e] Moody’s Investor Services, “Not-for-profit and public healthcare US medians: Revenue growth inches ahead of expenses as margins hold steady,” Sept. 3, 2019, Appendix I.

[f] McGrath, R.G., “Transient Advantage,” Harvard Business Review, June 2013

[g] Zenger, T., “What Is the Theory of Your Firm?” Harvard Business Review, June 2013.

[h] Pinchot III, G., Intrapreneuring: Why you don’t have to leave the corporation to become an entrepreneur, 2013.

[i] Peters, T.J., and Waterman, R.H., In Search of Excellence: Lessons from America’s Best-Run Companies, 1982, reprinted in 2016.