Realigning Care And Coverage

While the movement toward value-based care appears to be stalling out, a growing contingent of insurers and health systems are integrating coverage and care in different ways, working with each other or on their own.

By LOLA BUTCHER, HFMA CONTRIBUTING WRITER

Highmark Inc. has achieved nearly $2.5 billion in cost savings since 2017 through better health management resulting from a value-based reimbursement program for top-performing primary care physicians.

Those avoided costs at the Blue Cross and Blue Shield-affiliate division of Highmark Health came from inpatient admissions and emergency department visits that did not happen — in other words, revenue that hospitals did not receive — for Highmark members managed by physicians in the value-based care program.

Saurabh Tripathi, Executive vice president and CFO of Highmark Health

Pittsburgh-based Highmark Health, though, is unusual because it treats some of its health plan members in owned facilities. Of Highmark Health’s $22 billion in 2021 operating revenue, $4 billion came from provider operations. That mix, called a “blended health organization,” has served Highmark Health well, said Saurabh Tripathi, executive vice president and CFO.

“Having a payer side and provider side in our organization gives us the benefit of driving our vision and mission across the country,” he said.

Despite Highmark’s eye-popping results, the journey to value-based care has been slow as much of the hospital industry moved tepidly into value-based care arrangements. But there are signs that such activity is picking up.

Leading health systems and insurance companies are using a range of strategies — vertical integration, payer/provider partnerships and direct contracts with employers — to position themselves to accept financial risk for the quality and efficiency of care they deliver.

And CMS is doubling down. In its “refresh” strategy announced last fall, the agency said it expects all fee-for-service (FFS) Medicare beneficiaries and most Medicaid patients to be treated by providers in a value-based care model by 2030.

That could mean trouble for go-it-alone health systems that are clinging to FFS payment, in the view of Tripathi.

“Some of those health systems will struggle to survive because value-based care is the future,” Tripathi said. “My recommendation would be to get on this as quickly as possible, find a strategic partner, learn from someone who has done it and embrace value-based reimbursement.”

Cooperation Is A Necessary Ingredient

Payers and providers working in tandem instead of in opposition is essential to improving population health, according to David B. Nash, MD, founding dean emeritus of the Thomas Jefferson University College of Population Health and Dr. Raymond C. & Doris N. Grandon Professor of Health Policy at the university.

“My long-held belief, supported by the research evidence, is that we have to find a better way to realign economic incentives,” Nash said. “A very powerful way to do that is providers and payers working together.”

Highmark Health offers a compelling example of how to marry providers and payers. Formed in 2013 as the parent organization of health plans and hospitals, Highmark Health has developed multiple approaches to supporting the provision of and payment for care. (See sidebar, next page)

Highmark Health’s vision is to reengineer healthcare delivery to reduce costs and improve healthcare while enhancing individual wellness and customer satisfaction.

“We have designed Allegheny Health Network’s capabilities around that, and we have done the same thing on the insurance side,” Tripathi said.

He cites the example of the Together Blue low-cost narrow-network plan that includes only Allegheny Health Network providers and facilities.

“We have gone in a different direction than being an unrelated payer and provider,” he said. “We have worked together to draw a circle around our patients and members and customize our products for them.”

The Highmark Health strategy of owning payers and providers is unusual, and it does have a downside. While U.S. insurers have enjoyed record profits in recent years, health systems have been struggling with the financial challenges associated with the COVID-19 pandemic and, more recently, staffing shortages and wage increases. In Tripathi’s view, the financial burden of owning hospital systems in the short run is outweighed by the opportunity to advance value-based reimbursement.

“Our clinical team on the payer side works with the clinical team on the provider side, and we come up with the programs to reduce unnecessary utilization,” he said. “Within Highmark Health in the last couple of years, we have seen hundreds of millions of dollars reduction in the cost of claims by driving value-based reimbursement.”

Highmark Health owns and partners with a variety of organizations

Ownership:

- Blues health plans serving Pennsylvania, Delaware, West Virginia and parts of New York

- Allegheny Health Network, a 14-hospital system serving western Pennsylvania

- Lumevity, a consultancy focused on activating operational, digital and cultural change

- United Concordia Dental

- Technology companies HM Health Solutions, enGen and Helion

Partnerships:

- Holds a 20% stake in the Penn State Health system in central Pennsylvania

- Holds a 40% stake in a joint venture with Geisinger Health, serving four counties in north central Pennsylvania

- Entered a strategic partnership and value-based contract with ChristianaCare in Delaware

Another benefit of Highmark Health’s ownership of a health system is the opportunity to pilot new ideas for achieving the Triple Aim. One example: After the successful pilot of a technology-enabled Type 2 diabetes management program at Allegheny Health Network, Highmark Health earlier this year made the program available at no cost to most of its adult members diagnosed with Type 2 diabetes.

“We can use our own healthcare system to launch products and learn from the early successes — or failures, for that matter — and then go to our other provider partners with what we learned and accelerate the advance of those products across our footprint,” Tripathi said.

Banner-Aetna Joint Venture Working

With more than five years’ experience under its belt, Banner|Aetna — a joint venture between Phoenix-based Banner Health and Hartford, Connecticut-based Aetna Inc. that serves the Arizona market — has demonstrated some key advantages over traditional payer- provider contracts .

As equal partners, Aetna owns and Banner Health each owns 50%, both reap the financial rewards of reducing unnecessary utilization while also bearing the financial risk of not doing so.

“By having a joint venture, you can leverage where each entity has the underlying expertise,” said Banner|Aetna CEO Thomas J. Grote.

In the arrangement, Aetna handles the underwriting, pays the claims and supports sales and service while Banner Health manages the joint venture’s “performance network,” a subset of providers with a demonstrated record of high-value care, and handles utilization management.

“With 100% aligned incentives, we can turn over utilization management responsibilities to Banner to get the care decisions closer to the care delivery,” Grote said. Providers get fewer upfront denials citing “lack of information” because Banner has access to the medical records that provide clinical details needed to justify a request.

Another benefit is the ability to quickly implement innovations. For example, Banner|Aetna recently introduced Virta Health, a virtual program that helps people reverse Type 2 diabetes.

“We piloted it last year, saw immediate results from the pilot and stood it up within nine months,” Grote said. “The joint venture presents that opportunity because we are smaller and nimble — we have more than 375,000 members in one market rather than Aetna’s more than +20 million members across the entire country.”

The joint venture is delivering on both cost and quality. About half of Banner|Aetna members choose its performance network, composed of about 60% of the providers in the market.

“We’ve seen that network is consistently generating better results,” Grote said, referring to a higher percentage of patients using beta blockers properly and a higher percentage of Type 2 diabetes patients getting their hemoglobin A1C levels below 8%.

Meanwhile, the performance network generates up to 14% savings compared to the joint venture’s broad network, which encompasses almost all providers in the market. Those savings reflect fewer avoidable readmissions, less high-tech imaging being performed, shorter inpatient stays and reduced ED use.

Despite that track record, Grote says the joint-venture model is not the universal answer to America’s low-value care crisis. Aetna has five joint ventures across the country, and Grote does not expect that number to grow significantly.

That’s because the key ingredients necessary for a joint venture are hard to find. Both partners need a significant presence in the market. Both must have the capital to invest in a long-term venture, be willing to trust the other partner — and be truly committed to value-based care and population health.

“It can’t be just window-dressing,” he said. “You really have to believe in it. And it can’t just be the value-based care leader believes in it, but the CFO has to believe in it, and the system has to believe in it.”

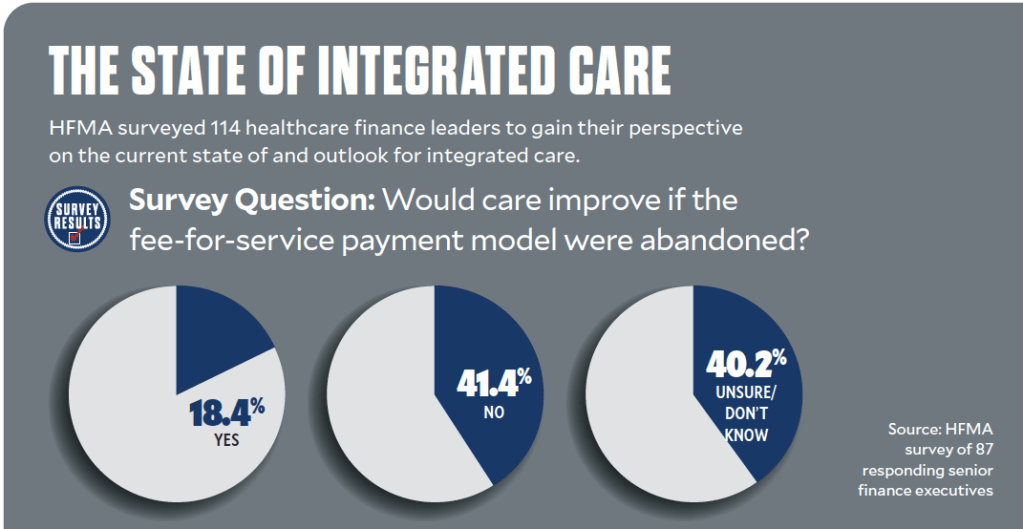

Years into the effort, insurance coverage considered to be value-based was achieved by just 11% of commercial coverage at the low end and in 29% of Medicare Advantage coverage on the high end, according to 2021 data from the Health Care Payment Learning & Action Network. Part of the reason adoption of value-based care is slow may be a lack of faith in the concept. Forty-one percent of finance executives surveyed by HFMA don’t believe that care would improve if FFS payment were abandoned, while 18% believe it would. The balance, 40%, are unsure or don’t know.

Early challenges come with creating consistent incentives throughout each partner organization.

Internally, “there are going to be people who run a service line or have responsibility for driving revenue through certain avenues, and the things we do in value-based care are not going to necessarily align with their goals,” Grote said.

Later challenges come with navigating the realities of the market, including competing health systems that are likely also working with other insurers and do not want to support the joint venture.

“Things get complicated, for sure,” said Grote, who predicted the value-based care movement will advance more through contracts between payers and providers than through joint ventures.

Cone Health System Invests in Health Plan

Leaders at Cone Health, a five-hospital system based in Greensboro, North Carolina, believe vertical integration is key to value-based care delivery — but the health system must be in charge.

“I’m not ready to cede health systems over to non-health systems, whether they be insurance companies or venture capital firms,” said Mary Jo Cagle, MD, Cone Health’s CEO. “My perspective is that health systems today are in a position that we can either be commodities or we can be aggregators and set our own path forward.”

Cone Health CEO Mary Jo Cagle, MD, (right), shown greeting nurse educator

Chanin Maynard, MSN, at an emergency department opening.

Cone Health chooses to be an aggregator. Earlier this year, it signed a letter of intent with a larger competitor — Novant Health, based in Winston-Salem, North Carolina — to take a minority ownership position in HealthTeam Advantage (HTA), a Medicare Advantage (MA) plan that Cone Health started in 2016.

With about 16,000 members, HTA is one of two MA plans in the state to receive Medicare’s five-star rating. Working in a competitive market in which nearly 70% of seniors are in an MA plan, HTA differentiates itself by its local roots.

“One of the reasons we’ve been successful is people associate our product with our physicians,” Cagle said. “We emphasize local physicians and a local product, and that has really reverberated.”

Novant’s investment will allow HTA to continue on a growth trajectory. The plan currently serves only a portion of the Triad Region, 12-counties in central North Carolina, but leaders see a much bigger future.

“We started in three counties; now we’re in seven counties,” she said. “A decade from now, I’d love to see it certainly all across the state of North Carolina, and perhaps even across the Mid-Atlantic or the Southeast.”

That confidence comes from Cone Health’s experience in risk-based contracts, starting with a Medicare accountable care organization a decade ago. Today, Cone Health cares for nearly 250,000 patients under various risk contracts with both private and public payers.

As Cagle and her colleagues gained experience with those contracts, they realized that the typical MA benefit design does not work for the benefit of patients, physicians or health systems.

“We saw that the key is designing [a] benefit plan that could lead to success, first of all for the patient and then with what the providers need to do to keep patients well or, if they have chronic disease, keep them in the doctor’s office and out of the hospital,” she said.

For example, Cone Health’s newest medical center includes Sagewell Health & Fitness, a medically supervised fitness center that HTA members can access through their Silver Sneakers benefit. The facility also serves rehab patients.

Northwell Sidesteps Payer

Nick Stefanizzi, CEO at Northwell Direct

Meanwhile, Northwell Health, based in New Hyde Park, New York, is moving the payer entirely out of the picture. It sees a need to get closer to the true purchasers of healthcare via Northwell Direct, a for-profit subsidiary that contracts directly with employers.

“That fundamental belief is why we believe we have an opportunity to offer an alternative to the traditional insurance carriers,” said Nick Stefanizzi, Northwell Direct’s CEO.

Northwell Direct launched in early 2020 just before the COVID-19 pandemic emerged. Its early clients were interested in it for its “at work” offerings, ranging from COVID-19 testing, vaccination and consulting services for the JetBlue workforce to primary care services, including health coaching, for Whole Foods’ employees.

Its other service line is “network solutions,” which provides the full range of health benefits to self-funded employers.

Northwell Direct partners with third-party administrators, pharmacy benefit managers and stop-loss carriers to handle functions typically under an insurance carrier’s purview. Its provider network extends beyond Northwell Health’s physicians to include other organizations — for example, Montefiore Health System in the Bronx and RWJBarnabas Health in New Jersey — for broader geographic coverage.

“We wrap that network with care management services that are proactive and fully integrated across that network,” Stefanizzi said.

“If we have an inpatient admission from one of our employers, I can send a nurse to the bedside before that individual is discharged to make sure that their follow-up care is not only fully understood but organized before they leave the hospital,” he said.

The direct-contracting model can save employers up to 20% on their health-benefits tab, Stefanizzi said. He thinks the approach will gather steam as employers seek ways to control their healthcare spend, but growth will be slow.

“This is a long-term build because the challenge we’re solving for comes with entrenched forces — traditional insurance models — in our way,” he said.

“The leadership [at Northwell] is taking a very long view of this as an investment in the future of the health system and a long-term growth strategy.”

Kaiser Permanente and UnitedHealth Group: Healthcare giants that offer care and coverage their own way

Kaiser Permanente, based in Oakland, California, is a long-time provider of integrated healthcare and does it on a scale other organizations can’t replicate. Meanwhile, UnitedHealth Group, Minnetonka, Minnesota, is not strictly an integrated care provider, but is seeing fast growth in its clinical care division, part of a sister company to its well-known health insurance operation.

Arthur Southam, MD, executive vice president, health plan operations and chief growth officer at Kaiser, described how the unusually tight level of integration between the three entities reflects the perspective of founders Henry J. Kaiser and Sydney R. Garfield, MD, who said access and coverage must go hand-in-hand.

Kaiser Permanente

With $100.6 billion in total revenue and income in 2021, this three-pronged organization consists of:

- Kaiser Foundation Hospitals, with 39 hospitals

- Kaiser Foundation Health Plan, with 12.6 million members

- Permanente Medical Groups, with nearly 24,000 physicians working for eight groups

What makes Kaiser Permanente structurally unique?

The health plan and the hospitals [divisions] are both not-for-profit, operating under the control of the same board of directors, and they have a very tight — in some cases, 75-year-long — relationship with these eight large multispecialty medical group practices. Of our $93 billion in [2021 operating] revenue, 98% of it came from our health plan selling health benefits to employer groups, individuals and Medicare and Medicaid beneficiaries. And those 12 million people who are enrolled in our health plans get 80% or more of their total care from our own delivery system.

What are the primary advantages of that arrangement?

In our world, the health plan is an integral part of the organization; it’s not a third party that we negotiate with. Therein lies a key difference with respect to other systems because the relationship of a healthcare delivery system to payers is often quite contentious. And most systems have multiple payers, but our healthcare delivery system — all 39 hospitals, 730-plus medical office buildings and more than 307,000 employees and physicians — works with only one health plan.

The three of us work together on strategy and determining where we invest our capital and develop facilities. And all of us — our health plan, our outpatient practice, our inpatient practice, our pharmacy services — operate on the same integrated technology platform, which is an advantage for efficiency and delivering well-coordinated care.

The KP model has obviously proven to be successful. Why has it not been widely adopted?

It’s hard for others to replicate this because most delivery organizations have and want relationships with multiple payers. And most health systems want and need relationships with many different physician practices in their community. The fact that there are so many relationships, in many ways, gets in the way of high levels of strategic and financial integration and a mutual commitment to the success of one another.

UnitedHealth Group

Parent to:

- UnitedHealthcare, a global provider of health insurance for individuals, Medicare Advantage and Medicaid managed care and businesses.

- Optum, which has divisions offering value-based care and consulting, pharmacy care services and data and technology

Although the organization doesn’t consider itself a payvider, health plan giant UnitedHealth Group has adopted a multi-pronge approach that allows the organization to act as a growing provider of clinical care and as a more traditional health plan.

UnitedHealth Group’s value-based clinical care-focused unit, Optum Health, just signed a deal to assist Walmart clinics in implementing value-based care, an Optum Health line of business that is growing swiftly. Optum Health overall saw revenue grow 36% to $54.1 billion in 202 relative to 2020, according to financial filings.

Although most of Optum Health’s revenue dollars came from affiliated companies, more 2021 revenue growth came from unaffiliated companies. Indeed, Optum Health’s 2021 revenue from unaffiliated companies soared 43% to $23.8 billion, and its unaffiliated business also grew sharply, rising 30% to $29.2 billion, the fi ling’s stated. A company spokesman said Optum Health works with more than 100 payers.

Meanwhile, UnitedHealth Group’s insurance operation, UnitedHealthcare, continues to add revenue and on a much larger scale, growing 11% to $223 billion in 2021. Thirty percent of UnitedHealthcare’s membership are covered with risk-base contracts.