Costing Managerial Accounting

Hospitals and physician practices generally achieve ‘moderately effective’ use of cost data, according to a survey, which also identified more effective approaches

April 1, 2020

12:14 am

A recent HFMA-sponsored survey found less than half of healthcare organizations consider themselves “moderately effective” at getting clinicians to use data to help lower the cost of care, while just 7% claim to be “highly effective.” The survey also identified steps that boosted physician engagement on the priority.

The survey of 254 hospital and physician practice executives by HFMA and Strata Decision Technology found a plurality (43.9%) rated their own effectiveness at using cost data as “moderately effective.”

The middling response actually raised more concern for one analyst, due to the increasingly serious cost pressures facing those organizations.

“Given the current environment we’re in, I’m not sure ‘moderately effective’ is going to cut it amid the increasing cost pressures,” said Chad Mulvany, director of healthcare finance policy, strategy and development for HFMA.

For instance, the recently released compendium of hospital data by the American Hospital Association found that the spread between net revenues and total expenses among 5,198 community hospitals narrowed from 9% in 2014 to 8% in 2018.

Most organizations aren’t seeing widespread adoption of cost data because of its complexity, agreed Alina Henderson, senior director of professional services for Strata Decision Technology. Effective use of cost data is a “heavy lift” because it requires both acceptance across an organization and use of that data to drive different outcomes.

“For most of our clients, using cost data ‘effectively’ means that the insights gathered from this data can be applied in key business decisions and functions,” Henderson said. “Organizations that use cost data effectively apply it to processes like financial planning and forecasting, clinical variation analysis, cost reduction and service line performance management.”

Other responses on cost data effectiveness included:

- 7% “highly effective”

- 23.7% “slightly effective”

- 3.5% “not effective at all”

- 21.9% “other” responses

Meadville Medical Center, a 249-bed community hospital in Meadville, Pennsylvania, mainly uses cost accounting to determine whether various service lines and procedure types are maintaining a positive revenue margin, said Cory Jackson, the organization’s controller.

“We feel our cost accounting data is very effective for that purpose,” Jackson said.

Cost accounting roles include helping the organization decide whether to add new types of procedures by comparing the actual costs and revenues of pilot procedures against their projected revenue.

Opportunities to engage physicians on cost

The surveyed healthcare organizations, which include hospitals and health systems ranging from those with less than 100 beds to those with more than 1,500 beds, also reported a range of engagement with physicians on cost data. Among key lessons organizations have learned to improve their cost accounting efforts are:

- 26.3% said engaging and including physicians very early in the process

- 21.1% said providing strong physician training about how and why use of cost data is important

- 15.8% said starting simple

- 10.5% said providing value to physicians

- 10.5% said maintaining focus on quality

- 5.3% said validating their results

- 5.3% said providing data visualizations

- 5.3% said having physician habit start in residency

“This showed the importance of making sure physicians have good resources to understand the cost data shared with them and the vehicle to use it effectively,” Mulvany said.

However, the role of cost data varied widely among organizations.

“Cost data is interesting to clinicians, but in my experience, the cost accounting data doesn’t drive the discussion, it just starts or ends the discussion and the real progress occurs from a dialogue on what could be different (which the data typically doesn’t tell us),” said Craig Ganger, vice president of finance for Premier Physician Network in Ohio.

Henderson said that in her work with hospitals, she has found physicians frequently are an underutilized resource by finance staff trying to apply cost data to drive improved care efficiency. Among the many reasons is that few organizations effectively engage clinicians earlier in the process, such as during cost model design, hypothesis-testing ad hoc analysis or data acceptance.

“The barriers causing this range from culture and communication to logistics and [data] accessibility but can be overcome with a focused approach,” Henderson said.

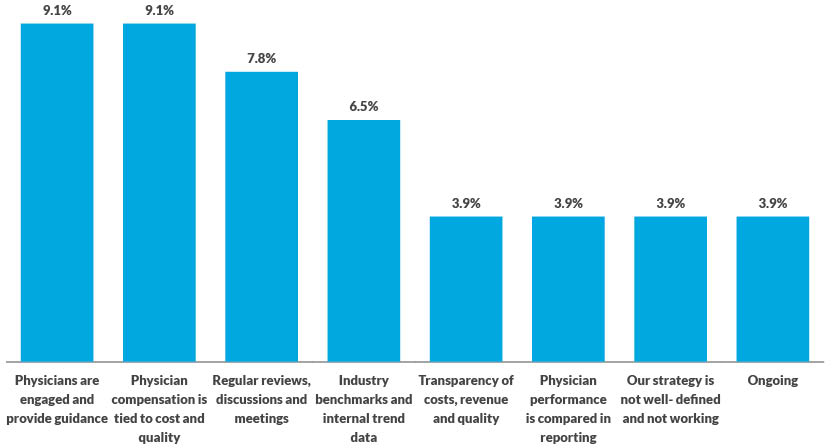

Cost data strategies used to reduce total cost of care

The data in the exhibit below reflect the response to the following open-ended question: Please describe the strategies your organization has used to encourage clinicians and/or physicians to use cost data to reduce the total cost of care.

Source: HFMA and Strata November 2019 survey

How to engage physicians more effectively

To assess the ways that organizations are engaging physicians in the cost accounting effort, the survey asked about the extent to which any of four strategies were used to help physicians understand and use cost data, and it found:

- 40.5% provide a dedicated live contact to answer questions

- 24.8% provide one-time or occasional training

- 12.4% provide regular training on data use and interpretation

- 11.1% provide user guides

- 11.1% provide no resources

Meadville’s Jackson said his hospital provides physicians with cost data down to the procedure level and compares those to the contribution margin, or the extent to which the procedure contributes to the organization’s overhead. Through the use of the reports and follow-up discussions, he has found physicians (about two-thirds of whom are employed) “are very receptive” to finding ways their treatments can be tweaked to allow them to contribute positively to the organization’s margin.

Such conversations vary based on the clinical area of focus and are complicated by the organization’s financial situation. For example, the hospital’s cost accounting initiative found that the organization only obtained a positive margin when both a higher-paying trial back surgery and a lower-paying follow-up full procedure were performed at the same hospital.

Those results were shown to surgeons, who then agreed to perform both procedures — when needed — at their hospital to help its margin, instead of their practice of splitting them between two hospitals.

HFMA’s Value Project research similarly had found increased physician engagement when in-person resources were provided in addition to static guides, Mulvany said.

Henderson’s experience also reflected the importance of providing live feedback resources on using cost data for effective clinician engagement.

“Anyone who is seeing cost data for the first time will have questions that need to be answered to help him or her better understand that data,” Henderson said. “Whether it applies to allocations, source systems, cost components or metric calculations, this discussion is most effective in an engaging forum versus a written FAQ document.”

That said, Henderson noted that the wide variety of personal learning styles means that such information is most effective when presented in both written and verbal formats.