Patient Financial Communications

Patient-Centric Aid in a Consumer-Driven Marketplace

November 28, 2018

11:25 am

A tailored financial plan based on a patient’s individual economic circumstances may increase the patient’s willingness to pay.

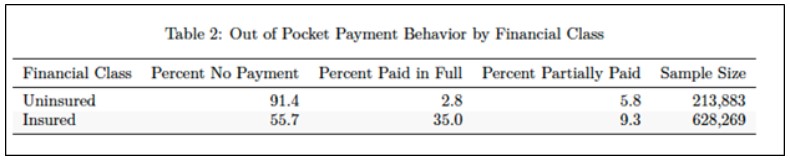

The accelerated trend toward high-deductible health plans and cost-shifting to patients has brought with it the need for healthcare provider organizations to implement a more versatile financial assistance policy. As it is, data show more than 91 percent of uninsured and 56 percent of insured out-of-pocket expenses go unpaid. a Furthermore, patients experienced an average increase of 29.4 percent in deductible and out-of-pocket maximum costs since 2015, and the majority of hospitals are now reporting that traditional collection solutions are not helping to improve their margins. b If these patients, who are in greater need of financial aid than ever, can be converted from nonpaying to paying, they will represent a vital revenue source for health systems.

Consequently, just as other consumer-centric markets have evolved to deliver fiscally responsive personalized financial experiences, healthcare providers find themselves in similar circumstances. Healthcare organizations may be able to capture some of that lost revenue by adopting some form of adaptive financial assistance (AFA). Anchored in the larger patient-provider financial wellness movement, AFA involves the use of enhanced analytic methods and qualifiers that adjust more dynamically to provider fiscal needs and patient economic diversity.

The key premise for AFA is that patients do not pay when financial assistance is insufficient, either because they can’t or because they elect not to. However, if the amount of financial assistance is targeted precisely to patients’ circumstances, they are most likely to pay in full, given their behavioral and affordability characteristics, and their payment levels will help providers achieve the highest possible revenue.

The Case for AFA

The current market presents obstacles for conventional financial assistance. Almost half of adults are challenged to cover a small-scale financial disruption of $400 let alone absorb unexpected out-of-pocket medical expenses that average many times this amount. c Paying high medical bills comes at great cost to one’s financial well-being or even economic survival.

Behaviorally, consumers are fiercely loss averse. From an informational standpoint, patients lack expertise to verify care quality and quantity, which could make them less inclined to pay. An added complexity involves the distressed consumption that pervades health care. The need for urgent care impedes patients’ competitive choice and rationing, which are thought processes that come more naturally when the patients are not distraught.

Further, providers tend only to encourage medical payment rather than legally compel it. Healthcare organizations recognize the heavy burden high bills put on patients and tend to be reluctant to pursue heavy-handed collection activities—especially taking into account factors such as negative public relations, mission discontinuity, and brand disutility that accompanies it.

AFA in Principle and Practice

Backed by a “no patient left financially behind” philosophy, AFA runs on behavioral economic principles. It concerns itself with how patients form payment attitudes, how they process price information, and what triggers a favorable response relative to capacity and perceived value for money. On the provider side, it considers a plethora of decisional dynamics that involve financial assistance-to-revenue sensitivities, operational consistency realities, balancing discretionary aid and fairness interests, and a give-get calculus.

In particular, AFA is mathematically tuned to amplify all facets of each individual financial assistance transaction, including provider revenue. As illustrated later, this process involves the use of big data techniques to locate financial assistance scenarios that generate the greatest payment compliance and highest revenue opportunity. From this process, a provider can identify revenue maximizing discounts (RMDs) targeted to each patient’s circumstances. Traditional income, family size, and conventional asset metrics are supercharged by the enriched RMDs and then used to recalibrate financial aid scales.

Operationally, using an AFA approach, financial counselors swap their existing aid calculation for the mathematically enhanced one. The resulting determinations are operationalized over the existing infrastructure and applied consistently just as they are now during intake or other points in the process. All qualification data are likewise stored and available to auditors. To ensure 501(r) compliance, providers communicate and explain to patients how to apply for financial assistance, what data are used in the AFA calculation, what is needed to be considered, and how they qualify for aid under each RMD tier.

Dataset, Design Controls, and Computation

Data used to design AFA contained approximately 785,000 insured and uninsured patient accounts between 2010 through 2017. Accounts were sampled from approximately 200 individual facilities. Each record contained historical payment transactional detail with roughly 75 patient affordability, payment behavioral, and account characteristics inputted from externally regulated sources.

In instances where accounts had multiple income, credit, and demographic identifiers, only the most recent information was used. As additional controls, the data and method were reviewed by economists, with comments from revenue cycle and healthcare finance executives to provide an industry perspective..

AFA Price Optimality

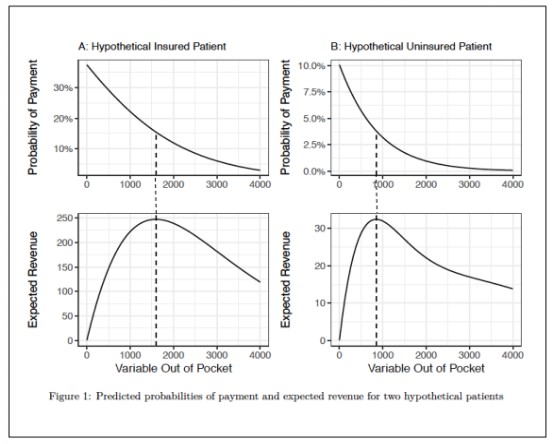

Methodologically, backwards induction is used to model how hospitals and patients respond sequentially to variable financial assistance scenarios. The computation begins with a review of historical baselines relative to payment on past balances, as shown in the exhibit below. A wide range of variables then are investigated to calculate optimal aid relative to payment likelihood and expected provider revenue. Financial assistance-to-revenue calculations are generated and the resulting coefficients are used to slot patients into best-response aid tiers.

As illustrated in the exhibit below, AFA optimality occurs where the apex of the expected revenue arch in the lower panel intersects with the downward sloping patient payment probability line in the upper panel. Expected revenue increases as AFA aid moves toward its optimality and then dissipates thereafter. It is here where payment probability and conditions align at their best-response potential. Offering financial assistance for amounts on either side of the dotted line results in lesser payment compliance and revenue opportunity.

AFA Results

Applying the model to real patient data, calculations show that AFA will result in improved revenue for healthcare organizations. Noteworthy findings include the following:

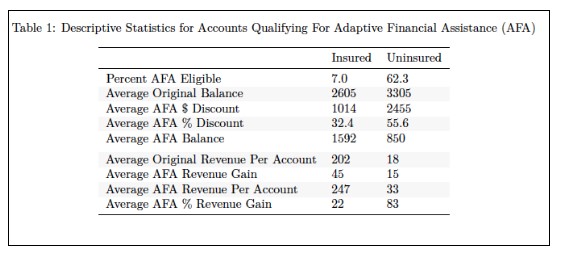

- Analysis reveals about 62 percent of uninsured patient accounts and 7 percent of insured accounts in the dataset possess characteristics where an AFA-generated aid adjustment results in a more optimal payment scenario than under the original bill amount (see exhibit below). d

- The average AFA RMDs are about 32 percent and 56 percent for insured and uninsured accounts, and the resulting average optimal balances are $1,592 and $850 respectively.

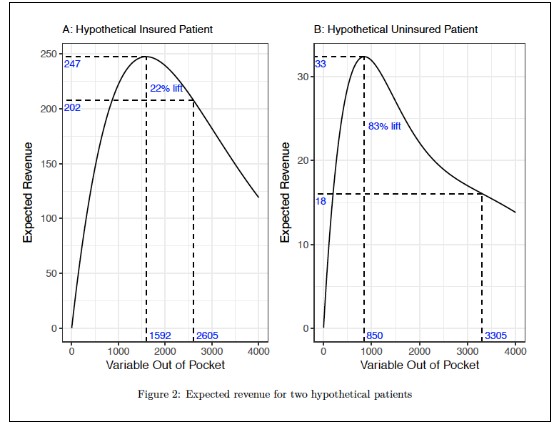

- AFA generates an 83 percent per-account revenue increase for uninsured patients and 22 percent for the insured (see exhibit below), with the mean probability of payment in full roughly doubling and quadrupling for the insured and uninsured respectively.

A clearer picture emerges when the AFA algorithm is applied to a prominent academic medical center. Modeling shows:

- Approximately 2,130 patients per month would benefit from the AFA approach.

- The calculated optimal discount is 32 percent for the insured and 71 percent for the uninsured.

- The annual forecasted revenue lift is approximately $1.1 million when billing at these discount percentages.

In other words, AFA suggested that by not billing a monthly average of $8 million for the 2,130 patients under the existing practice and, instead, billing only $3.2 million, the result would be a $1.1 million increase in collected revenue.

AFA Key Considerations

Considering AFA involves a comprehensive and data-guided assessment of the current system relative to advancing an enhanced alternative to it. The algorithms and method described earlier could help define the benefits and best-response options once adjusted for market-specific data, provider financial aid baselines, and performance objectives.

In parallel, examination should extend to whether (or how) managed care contracts allow for AFA aid-based discounting. Here, investigation could look for any unequable cost-shifting in rate construction, with a focus on whether a $1 cost-shift to beneficiaries equals $1 in provider revenue. Should financial inequities present themselves, analysis would reveal cause for higher payments and/or allow for AFA flexibility.

Related consideration involves evaluating the impact of excessive premiums, with emphasis on the impact on out-of-pocket payment. If paying both the premiums and the out-of-pocket amounts presents patients with a difficult economic choice, and they opt to cover the premium over the out-of-pocket expense, their decision boomerangs back to providers in the form of uncompensated costs.

Finally, when planning for AFA, providers should consider updating their community messaging. For example, because AFA is based on individually tailored, fiscally responsive, personalized experiences rather than on a more generalized group aid approach, providers my find it helpful to script consistent messaging patients around AFA’s precision and the fact that it is additive, mission-driven, patient-centric, and being applied equitably, among other things.

AFA Benefits

AFA benefits accrue through the formation of cooperative payment dynamics and establishing more idealized, just right conditions early in the financial aid counseling process as illustrated above. Once instituted, these conditions:

- Increase provider revenue expectations while reducing patient payment dilemma

- Lessen the effects of systemic nonpayment, particularly for uninsured patients with low-to-moderate affordability and payment behavioral characteristics

- Reduce costly downstream billing, dunning-cycle, and collection activities that result in patient disengagement, dissatisfaction, and no-payment scenarios

- Diminish the ineffective practice of assigning unattainable out-of-pocket expenses absent financial assistance pricing precision

- Establish healthier patient-caregiver financial relations, which offer increased payment conversion and more sustainable bottom-line margin potential

A Precursor of More Consumer-Centric Health Care

As an industry first-mover, AFA shows promise to enhance financial aid policy in three distinctive ways. First, it identifies optimal assistance and revenue scenarios. Second, it aligns more exactly with patient economic diversity, including with the economic circumstances of those who have the least capacity to pay in full. Third, it delivers fiscally responsive personalized financial experiences that boost satisfaction while preserving as much provider revenue as possible.

More broadly, AFA introduces behavioral finance and established economic principles into the patient financial affairs conversation and calculus. Doing so allows for methodological inclusivity that stimulates larger conversations between practitioners and academicians to prompt and inspire advanced solutions, given the need for change in the patient-provider financial wellness relationship. The narrow application demonstrated here reveals just one opportunity.

Building on research that led to the development of AFA, future efforts should be focused on designing individually customized comprehensive financial plans for patients at preregistration, developing advanced and tailored financing products with personalized payment installment options, creating more frictionless payment configurations such as digital wallets, using crypto-currency, and advancing all categories of consumer-directed medical expense financial wellness strategies. Until these innovations have been achieved, the principles and methods described here offer only a preliminary glimpse into the advantages of more intelligently designed, patient-centric financial assistance approaches for today’s consumer-driven marketplace.

Footnotes

a. ARxChange study.

b. Dyrda, L., “ 12 Trends in Patient Responsibility Payments, Up 29.4% Since 2015,” Becker’s ASC Review, Oct. 24, 2017.

c. Board of Governors of the Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2016.

d. The disparity among the two financial classes is mainly the result of much larger average out-of-pocket expenses for uninsured patients.

e. Of note, the AFA average aid discount is not mathematically the same as the discount calculated (or implied) from the average change in balances. The former weights each account the same, whereas the calculated/implied discount from the average balances weights the large balances more than the small ones. Also, individual gains, AFA designs, aid, and pricing equilibria would differ by market and for each specific population.

The authors acknowledge contributions to this article by Steven Kurz, MBA; Jerry Bruno; Lisa K. Neff-Wheeler; and Bruce Hallowell.