Given that the M&A market is strong at all levels in the healthcare market, finance leaders should focus on where they can make moves to increase their ability to compete in a changing market.

It seems as if every week brings the announcement of a new healthcare megamerger that supposedly will transform the industry. From Walmart-Humana to CVS-Aetna, the continuous message is that disruption has arrived.

It is true that many of the announced cross-market megamergers are bringing new levels of transactional value, volume, creativity, and potential industry impact. But in reality, merger-and-acquisition (M&A) activity in the lower and middle markets is just as strong, accounting for more than 90 percent of recent deal volume, according to FactSet’s August 2018 Flashwire US Monthly . These deals affect healthcare organizations more directly and immediately than do the top-market newsmakers. And for healthcare finance leaders who must return to their day jobs after reading the headlines, it’s on those markets where their focus should be—and where they can make moves to increase their ability to compete in a changing market.

A recent report, Reshaping Healthcare M&A: How Competition and Technology are Changing the Game, addresses trends that influence buy-and-sell decisions in the hyperactive healthcare marketplace. The report is based on a Q1 2018 phone survey of 100 healthcare senior executives with experience as M&A dealmakers in the middle market. One-third of respondents are corporate executives and two-thirds are private equity executives. The insights and direction gleaned from the survey can provide direction for financial executives who are looking to place the right bets.

Economic Drivers

In 2017, there were 579 deals for U.S. healthcare targets, the second-highest total on record. And the first quarter of 2018 (the most recent quarter for which data are available) saw a nearly 35 percent year-over-year increase in completed healthcare M&A transactions, according to the survey report. Economic conditions have ripened the market for this level of activity in several ways:

- Unemployment has reached historically low levels.

- Borrowing has been cheap for a while.

- Companies have paid down debt and stockpiled cash (with a chance to glean even more from the 2017 tax law).

- The nation has ushered in a new presidential administration that favors deregulation.

All signs point to M&A activity continuing at heightened levels.

More companies and investors than usual have money (or at least capital) to spend. More money means more buyers, and an increase in buyers leads to a shortage of attractive targets. That’s the top challenge in healthcare M&A right now, according to 25 percent of respondents to the survey. Additional characteristics of a seller’s market are almost equally as challenging: High valuations, excessive competition, and condensed timelines for due diligence each were named by 20 percent of respondents as the most significant barrier.

“Valuations are a big concern in the current market,” one private equity operator observed. “Businesses that have matured over time have accumulated assets that have increased in value. With affordable valuations being a criterion of attractive targets, the number has fallen considerably.”

Such valuations typically are expressed in terms of enterprise value divided by earnings before interest, tax, depreciation, and amortization (EV/EBITDA). In 2017, the median EV/EBITDA multiple for U.S. healthcare transactions was 13.8, which is down slightly from the median figure of 14.5 in 2016 but a substantial increase over 2015, when the number was 10.9.

Yet market players are adapting, altering their bets to the conditions of the market.

Joint Ventures as an Option

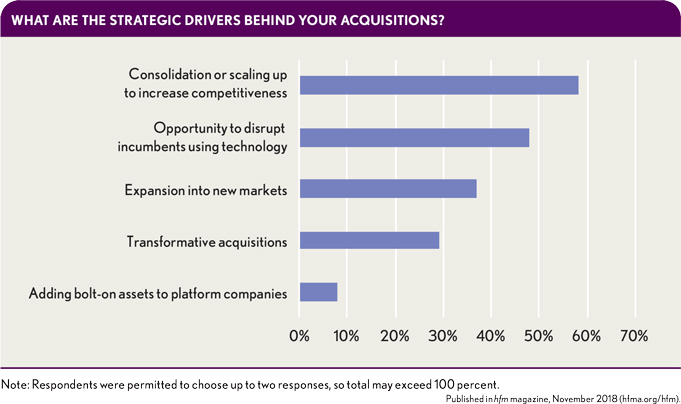

Healthcare companies and private equity firms alike have developed methods to help them overcome the challenges they face. One of the main strategies both groups are using is to consolidate or scale up to increase competitiveness—reported by 58 percent of the survey respondents—in contrast to the much-hyped vertical integration seen among some large-cap players. That approach is the primary driver for only 8 percent in the middle market.

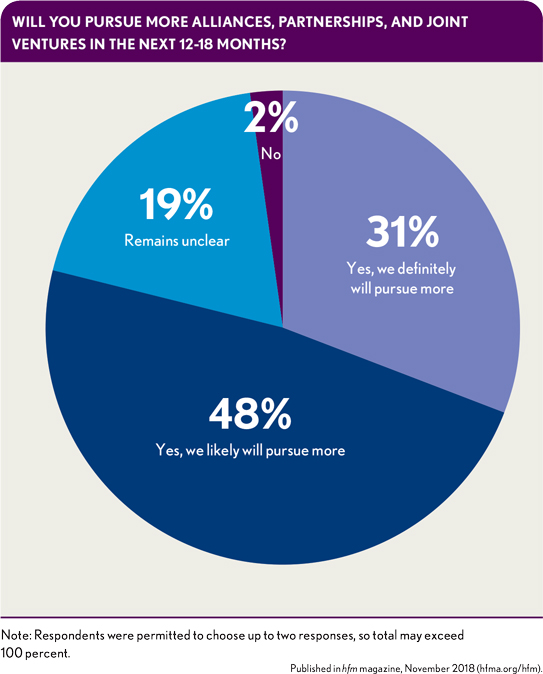

Organizations also are turning to joint ventures and alliances to expand into new markets and grow top-line revenue more quickly and with less hassle. An overwhelming majority (79 percent) responded that they expect to pursue alliances, partnerships, and joint ventures in the next 12 to 18 months. Health system finance leaders know all too well that joint ventures and partnerships can be an effective approach when at least one party wants to remain independent but both sides could make gains through close cooperation. Although alliances come with their own set of challenges, they allow organizations to realize value sooner by avoiding some of the incredibly challenging and time-consuming aspects of M&A deals, such as fully integrating infrastructures, cultures, and technology.

Joint ventures also can be a means by which to access new technology. The most prominent benefit of partnerships and joint ventures is the opportunity to access outside technology or expertise, according to 57 percent of respondents. In a world that increasingly favors a digital-first approach, quicker access to new technology could be game-changing for some organizations.

In addition to alliances, more than half of the survey respondents said they believed asset sales by large-cap healthcare companies would increase significantly (32 percent) or moderately (31 percent) in the year ahead. If that prediction comes true, new assets on the market may become highly lucrative opportunities for middle-market buyers who are looking for fresh inventory.

“There is significant pressure on large-cap healthcare companies either on the growth front or because of regulatory changes,” a corporate development director noted. “I think as pressure continues to mount, companies will find it challenging to maintain top-line growth. Some will react by sharpening their focus and selling non-core assets.”

Indeed, divestitures are piquing the interest of strategic buyers looking for ways to get into the M&A game. Companies hoping to raise money for higher-priced acquisitions could find themselves selling some of their own assets to fund the deal. Given the new tax law and high valuations, many corporations are looking inside their own house to decide what they can sell. They know they can set a high price—and at the lower tax rate, they get to keep more of the profits.

The Impact of Technology

Technology has emerged as perhaps the central force shaping acquirers’ M&A strategies in the healthcare middle market. An overwhelming majority of respondents, 93 percent, said technology and systems integration challenges are creating added complexity in the healthcare industry.

Also, more than a third of respondents (36 percent) said the fast pace of technological change would pose the greatest challenge to healthcare companies over the next one to three years. In the context of M&A, this concern raises the importance of digital due diligence in the targeting phase and makes it critical to plan how acquired companies will be able to adapt, or disrupt, using technology going forward.

Many healthcare companies, of course, still do not provide an Amazon-like customer experience. The need to manage patient-protected data is a valid concern, but there also is a real opportunity to improve.

To be sure, buyers said they are looking for acquisitions that can evolve with the rapidly shifting environment—or that can enable them to proactively transform the environment themselves. In that sense, the emergence of new digital tools is seen as a prime opportunity: 48 percent of respondents said one of their top two strategic drivers for making healthcare acquisitions was the chance to disrupt incumbents using technology. And they were more likely to invest in healthcare IT than in any other subsector of health care, including providers, staffing, and even home health.

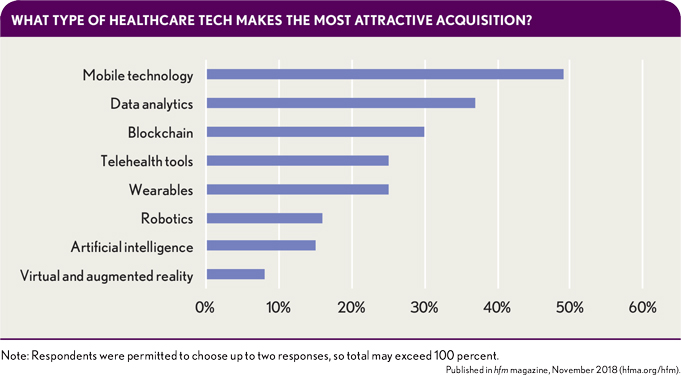

Various technologies are seen as having potential to advance the industry. Among survey respondents, the technologies deemed most attractive were mobile tools (49 percent), data analytics capabilities (37 percent), and blockchain applications (30 percent). Wearables, sensors, and trackers (25 percent) and telehealth tools (20 percent)—all of which intersect with the mobile space—also are drawing interest.

A Focus on Culture

In the current competitive environment, dealmakers are devoting substantial energy to the targeting phase in M&A, especially to technological considerations. But there also is an increasing appreciation for the importance of the post-close period, when a promising asset can realize its potential—or succumb to business pressures, if the new owner isn’t sufficiently nimble.

One issue that remains a perennial concern is cultural fit. Among respondents who reported oversights in due diligence for their most recent acquisition, 36 percent said their biggest error was not detecting a mismatch in work cultures. Regarding the integration phase, the third most-cited challenge was a culture clash with the acquired company’s personnel (21 percent).

Beyond culture integration, respondents cite additional challenges that crop up after a deal is completed. Chief among them are prioritizing investments in the newly acquired asset or company that will derive the most value (24 percent) and making effective cost cuts (22 percent). The closeness and low percentage level of these two responses suggest that buyers’ post-deal challenges are varied and fragmented.

Staying Ahead of the Curve

Healthcare M&A activity shows no sign of slowing. Prices are steep, and the competition is fierce. However, in a market where competitors are leveraging acquisitions to open new markets and gain access to human and technological resources, it is difficult to simply watch from the sidelines and not adjust business strategy accordingly—whether or not that strategy includes M&A.

Although cross-market megamergers understandably grab our attention, it is important for every organization to ensure that its business and technology strategy allows it to derive maximum value in accordance with its unique circumstances. Such a strategy is what enables successful healthcare finance leaders to place the right bets.