Costing and Managerial Accounting

Activity-Based Costing: When to Walk and When to Run

Published

May 30, 2019

3:39 pm

|

Updated

November 7, 2022

8:47 am

Sponsored by Kaufman Hall

In a method popularized by long-distance runner and Olympian Jeff Galloway, runners learn to intersperse walk and run segments during their race. Among the advantages of the method is a reduction of stress and fatigue, both during and after the run, as runners build in time for recovery throughout their race. The logic behind Galloway’s method applies beyond the running path. Organizations may perform best when they blend higher and lower intensity efforts and choose to run full speed when the effort is likely to generate the most value.

In cost accounting for healthcare, higher effort models including activity-based costing and time-driven activity-based costing have attracted growing interest. While these models can provide meaningful analytics, for many organizations the level of detail required will prove to be a heavy lift. A modified approach to activity-based costing matches intensity of effort with potential impact on organizational performance and helps finance leaders identify when to walk and when to run.

A Modified Approach to Activity-Based Costing

A modified approach to activity-based costing can balance an organization’s desire for operational excellence with its need for repeatable, low-maintenance solutions. Key to this approach is identifying areas in which the effort involved in activity-based costing will be rewarded with a significant impact on financial or clinical performance, operational efficiency, or organizational decision making.

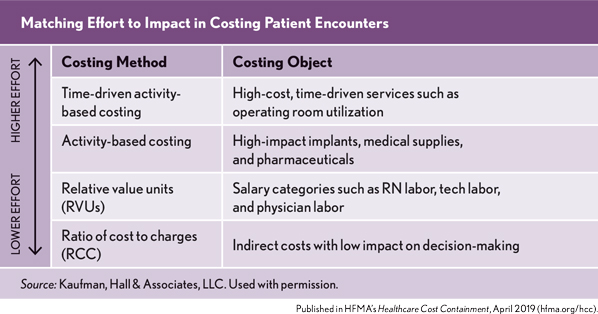

For example, as hospitals and health systems face downward pressure on payment rates and a push toward greater price transparency, finance leaders likely will need a more detailed understanding of the costs associated with individual patient encounters. A tiered approach to costing focuses the most intense efforts on high-impact items (see the exhibit).

In this case, time-driven activity-based costing is used for high-cost, time-driven activities such as operating room utilization, while activity-based costing is used for high-cost implants, medical supplies, and pharmaceuticals. The assignment of actual vendor cost to the chargeable item, or even directly to the individual patient encounter, can provide valuable insight into the impact of physician preferences on the cost of an episode of care. Paired with data on clinical outcomes, these insights can help identify which items produce the best outcomes at the lowest cost.

At the next level of intensity, relative value units (RVUs) can be used for staff salary expenses such as nursing labor, tech labor, and physician labor.

At the lowest intensity level, a traditional ratio of cost to charges (RCC) approach can be used to allocate expenses in areas such as non-chargeable supplies or miscellaneous costs that have a very low impact on decision making.

A higher intensity approach may also generate value in areas that are not immediately apparent. For example, a more detailed approach to costing for certain areas of indirect or semi-direct costs can also provide valuable insights into the true cost of patient encounters, while mitigating the distortion of results that can occur when these costs are allocated solely on the basis of statistics such as revenues, expenses, or FTEs. Expenses from areas such as surgery scheduling, cancer registry, patient financial services, and case management can be assigned based on the related clinical activity to individual patient encounters as direct, controllable costs for analytics. In a similar manner, clinical semi-direct costs, such as expense in clinical administration departments, can be redirected to specific direct departments to facilitate full cost assignment.

As finance leaders adopt more detailed costing methods, they should also consider the calculation frequency and the costing time period. A move from year-to-date to monthly or quarterly periodic costing will improve opportunities for trending. It will also ensure that early months are not reprocessed with each costing cycle, thus making the process more efficient. For many organizations, a quarterly processing cycle will strike the right balance between a timely refresh of costing data and demands on staff time.

Benefits of a Modified Activity-Based Costing Approach

By focusing higher-intensity costing methods on high-impact areas, a modified activity-based costing approach creates efficiency and helps ensure stakeholders that their time is being spent on efforts of value to the organization. Improved transparency on true costs makes end-users more confident in the costing data.

As the benefits of a modified activity-based costing approach become evident, finance leaders may decide to dedicate more resources to higher effort “runs” and less to lower effort “walks.” Throughout this process, organizations will need a cost accounting solution that has the capability and flexibility to:

- Cost all components with the most appropriate methodology

- Enhance costing methodology for different components over time

- Pull these components together to present a full and accurate picture of the organization’s costs

By finding the proper balance between costing “runs” and “walks,” finance leaders can help put their organization on the path to improved financial and clinical performance.