Value Based Payment

Risk contracting: Outlook and success factors for hospitals and health systems

Published

March 30, 2021

5:31 pm

|

Updated

November 16, 2022

11:48 am

Sponsored by GHX

To begin to realize the full benefits of value-based payment contracts, hospitals and health systems need to understand what’s in it for them and their patients and physicians. Those leading the way have already enjoyed enough success to realize clear benefits.

Almost 95% of hospital and health system respondents to an HFMA study said that coordination and collaboration with partners in alternative payment models (APMs) will improve or remain unchanged over the next five years.a This finding may reflect an auspicious outlook for the future of value-based payment and its ability to positively transform the nation’s healthcare system. Value-based payment holds the key to achieving the Triple (or “Quadruple”) Aim of reducing cost of care while improving care quality and the patient and provider experience.

The findings of the December 2020 study, sponsored by GHX, corroborate results of an HFMA-GHX study conducted in August 2020, which found similar levels of optimism among hospitals and health systems regarding the prospects for their performance under APMs.

The earlier study sought to assess the relative resolve of U.S. hospitals and health systems to participate more deeply in the transition to value from a predominantly fee-for-service model. The study asked whether COVID-19 had either a positive or negative impact on organizations’ views regarding their ability to improve the collaboration and cooperation among APM partners so essential for financial success under risk contracts. The answer was clear: COVID-19 has had little effect in dissuading organizations from moving ahead with plans for taking on more risk. If anything, many pointed to the benefits of a steady revenue stream derived from being paid for managing the health of a population, rather than being reliant on fee-for-service for the types of procedures that had to be deferred during the pandemic, which resulted in big revenue losses.

The December study took these questions one step further with a focus on understanding key specific success factors and obstacles that organizations must address to thrive financially under an APM. The research sought to elicit key insights about these factors, with attention to lessons learned from the organizations that have enjoyed some success in achieving the benefits of a value-focused approach.

This research is a continuation of HFMA’s long-standing support for the underlying principles of value-based payment, and its ability to improve care quality while reducing costs.

“HFMA formalized their work on the transition away from fee-for-service healthcare with a series of reports under the name of HFMA’s Value Project over a decade ago,” said Todd Nelson, FHFMA, MBA, director, partner relationships and chief partnership executive at HFMA. “This work looked at defining the value equation and the current state of value, and it outlined the key capabilities needed and provided insights and information for a path to value. These principles still hold true today as we continue down the journey to value.”

A long and winding road

The message from the research was mixed. Although it found that, overall, the outlook for the future of value-based care was positive, it also found many obstacles lie ahead for the nation if it is to complete the transition to value. Among the almost 95% of survey respondents who believed stakeholder collaboration and cooperation in support of APMs would either improve or remain unaffected by COVID-19, 61.8% were optimistic, expecting to see improvement. That leaves 32.8% who did not see a change in the status quo. And a significant 5.3% were openly pessimistic about the future of value.

Perhaps the greatest differentiator between the first and last groups was that organizations committed to moving forward had a clear vision of what was needed and the expected benefits, whereas those that were pessimistic were leery of taking on risk by entering into what for them was a realm of uncertainty.

How much more practical might it seem to choose the certainty of revenue from FFS over the uncertainty of assuming risk? Based on the survey responses, the answer lies in grasping the true potential of value-based payment.

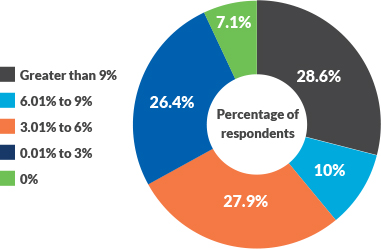

Where the nation stands today on the road to value is perhaps best evidenced by the relative amount of revenue that respondents to the survey say they will have at risk in value-based contracts in five years. About 34% of responding organizations project having less than 3% of their revenue at risk in APM arrangements, whereas only 28.6% anticipate having more than 9% of revenue at risk in such arrangements. Clearly, it will be some time before the nation sees a complete shift to value.

Survey question: In five years, what percentage of your net patient service revenue do you anticipate will be at risk in an alternative payment model?

One other suggestive point is that the survey uncovered no statistical significance in any of the findings, suggesting the similarity of responses might be determined by factors organizations had in common, such as size, location, number of physicians or number of beds. In other words, a large health system was just as likely as a small rural hospital to be either optimistic or pessimistic about the outlook for value-based payment.

That said, let’s look at key perspectives from the three groups.

1. The optimists. When asked why they were optimistic about seeing improved collaboration and cooperation in the next five years among AMP partners (i.e., other hospitals or health systems, employed and community physicians, post-acute care providers, and internal and external supply chain partners), the most common response among these respondents was that they and their partners recognized the mutual benefit of shared growth and coordination.

Other common responses included:

- The sense that APM partnerships resulted in better-informed medical decision-making and innovation

- An overall good prior experience with such contracts

Among the factors these organizations cited as driving success, the very partnerships themselves were the most commonly cited benefits. APMs appear to foster a spirit of collaboration that promotes success. Other factors included:

- Increased competencies and abilities in evaluating resources

- Cross-departmental collaboration

- Leadership direction

- Ability to understand data

The most cited areas requiring additional work were improvement in flexibility and coordination with partners. Other areas mentioned as requiring more attention included:

- Care coordination

- Data access and analysis

- Coordination between clinic care and revenue cycle teams

- Provider and payer partner engagement

Most respondents also cited these efforts as ongoing, with time horizons for addressing specifics ranging from one to five years.

Two findings were perhaps most telling:

- About two-thirds of respondents attributed their success to careful planning and preparation, as opposed to capitalizing on existing capabilities to move forward.

- Almost 56% suggested efforts to improve collaboration and cooperation needed to be focused primarily on physicians, compared with 25% who saw post-acute care providers as primary areas of focus.

Nearly 80% of optimists also saw a role for supply chain partners in their efforts to promote value, with almost half of those respondents seeing the role as important or very important.

2. The moderates. This group, comprising 32.8% of respondents, appears to represent various perspectives on the future for value-based payment, unified by the expectation that they will not see any significant change in collaboration and cooperation with their APM partners in the next five years.

Although comments of some respondents in this group suggested they recognized the need for change (i.e., “all facilities need to change and collaborate”), the most common reason cited for no change was that the environment today is balanced and static.

Factors contributing to this static environment included:

- The challenging payer structure

- Shortage of willing APM partners due to lack of interest

- Small patient volume in value-based arrangements because of the small amount of revenue at risk

A lack of risk tolerance was the most-cited obstacle to success with risk-based contracting. Indeed, the very term risk could be viewed as a disincentive to pursue risk-based contracts in the face of the “certainty” of fee for service.

This obstacle goes hand-in-hand with the next two most cited obstacles: Resistance to change and conflicting agendas and goals.

Nonetheless, these organizations also appear focused on making strides. Top responses regarding priorities to lay the groundwork for success were to:

- Build and upgrade networks

- Improve analytics

- Improve communication

And 50% of respondents were either working on those priorities now or hoped to meet them within six months to a year.

For this group, again, about two-thirds attributed their current stance toward value-based care to a matter of choice. The other third said they were challenged by issues of feasibility.

Perhaps one of the most notable similarities between the optimists and the moderates was that, for both groups, efforts to promote collaboration and cooperation were focused primarily on physicians. Among moderates, 66.7% of respondents cited this priority.

Moreover, an even greater percentage of respondents in this group believed supply chain partners bring value to value-based payment arrangements, with 83% holding this view, and 33% believing the role is an important one.

3. The pessimists. Only about 5% of respondents were pessimistic about seeing improved collaboration and cooperation among APM partners in the next five years. Their responses suggested a strong disinclination to pursue such contracts. Reasons offered included:

- The whole undertaking is too complex.

- There is too much uncertainty, including COVID-19.

- It’s too time-consuming and a drain on resources.

- Metrics are inconsistent, and data access with partners is poor.

Perhaps most telling were two comments from respondents about the obstacles to success with value-based contracts:

- “Leadership does not understand the tactical concepts of risk-based contracting.”

- “The program must provide value. Otherwise, the work involved (and there is a lot) is not worth it.”

When asked if, despite the obstacles, their organization might still increase participation in risk contracts, one respondent said only if downside exposure were minimized. Moreover, in three of four cases, these organizations’ stances toward value were a matter of choice.

Success comes from understanding the benefits of delivering value

Although the outlook for the nation’s transition to value-based care remains positive, there clearly is much work that remains to be done.

Risk aversion is perhaps the biggest obstacle: But COVID-19 has challenged such assumptions, showing population health payment models can provide a steady revenue stream at a time when fee-for-service revenue might face sudden declines due to a crisis. Hospitals and health systems have learned that lesson in no uncertain terms as they experience a profound decline in elective surgeries as a direct result of the COVID-19 pandemic.

If the nation is to reap the full benefits of a value-focused approach to healthcare, organizations need to clearly perceive and understand the long-term benefits of value-based payment, not only to society but also to their own organizations. Simply put, those benefits include:

- Reduced cost of care and improved coordination of care

- Improved population health

- Improved patient experience

But understanding the benefits is only part of what’s needed. Organizations taking on risk need to understand the nature of the risk they are taking. And the HFMA-GHX research found that, overall, organizations moving ahead most forcefully in APMs look to data analytics to gain that understanding, and they look to physician engagement and leadership to take the steps necessary to realize the benefits.

See Part 2 of this article for a discussion of implications of the HFMA-GHX study findings, with comments from study participants.

Footnote

a. Reese, E.C., “Hospitals and health systems remain optimistic, overall, about APMs,” hfm, December 2020; APMs include accountable care organizations (ACOs), bundled payment and other population health models, both governmental and commercial, where providers can receive incentive payments tied to the quality and value of care they deliver to patient populations.