Cost Reduction

Understanding physician costs is the first step in clinical cost transformation

Published

October 14, 2019

8:30 pm

|

Updated

November 7, 2022

8:37 am

From our Sponsor, Kaufman Hall

Before you can address costs, you must know what those costs are. While this statement seems obvious, it defines a problem for many healthcare finance professionals. In a recent survey of healthcare finance executives, more than 70% of respondents said they did not have a high degree of confidence in the accuracy of results from their existing cost accounting solution. Almost 50% said they had no or very limited use of cost and profitability reports to support strategic decision-making and influence financial and tactical planning (2018 State of Cost Transformation in U.S. Hospitals and Health Systems: Time for Big Steps, Kaufman, Hall & Associates, LLC).

A lack of actionable cost data is a particularly acute problem with respect to physician costs. Costs associated with the physician enterprise are a significant driver of patient care costs and service- line profitability, and health systems’ need for accurate and trusted physician cost data has only intensified. Physicians continue to migrate from independent to system-owned practices. New payment models push health systems to identify and remove unwarranted variations in the cost of care to realize savings against historical cost benchmarks or keep costs below a bundled price paid for episodes of care. Yet many health systems maintain a hospital-centric cost accounting structure that fails to provide actionable insights into physician costs across the care continuum.

Overcoming challenges to effective cost accounting

To gain insights into physician costs, finance leaders must be willing to move beyond traditional cost accounting methods to a cost accounting solution that addresses the following limitations:

Use of overly simplistic methods. Reliance on ratio of cost to charges (RCC) will never provide the granularity needed to accurately capture physician labor costs. A solution that can incorporate relative value units (RVUs) and micro-costing (e.g., to determine time spent at different sites of care) is essential.

Time- and resource-intensive processes. Time and resources will always be limited. A cost accounting solution must be efficient, with repeatable processes.

Lack of timely results. Reliance on data that is six months old — or older — restricts an organization’s ability to respond in a timely manner.

A hospital-centric focus. As more care moves beyond an acute setting, finance leaders must have the ability to accurately identify costs across the continuum of care.

Lack of buy-in from executive leaders and physicians. Combined, the limitations described in the preceding bullet points generate data that lack the specificity needed to build trust in the data’s ability to inform decision-making. Stakeholders need a transparent process that identifies data sources and assumptions made in analysis of costing data.

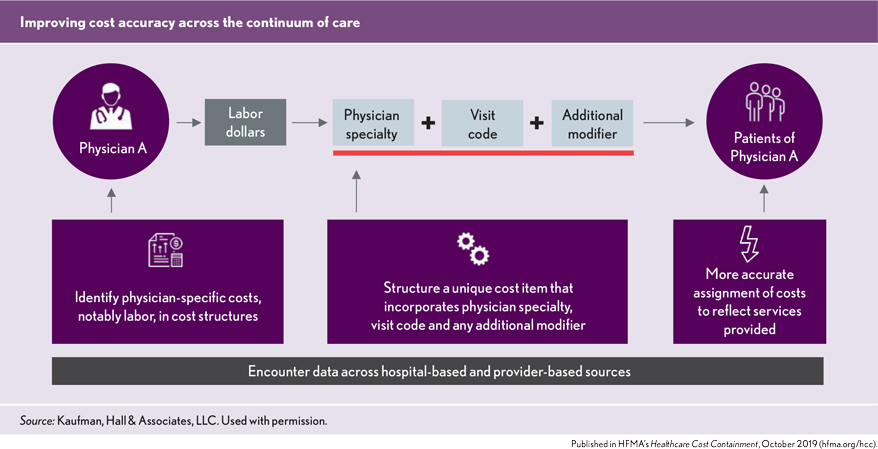

The goal of physician costing is to complement existing hospital-based accounting processes by identifying physician-specific costs, notably labor, in cost structures and more accurately assigning these costs to patient-specific encounters.

As the accuracy of physician cost data grows, so too will confidence in the data and its ability to serve as a tool to identify opportunities for improving physician performance, growing service lines or negotiating payments that better reflect the full costs of delivering care.

Getting started

The addition of physician costing to existing hospital-based costing processes should be approached as a work in progress: Physician cost data can be refined gradually to improve the data’s specificity and value as a decision-making tool. It is nonetheless important to start with a plan, which includes the following steps:

Set the vision. Work with executive and physician leadership to define what the organization hopes to learn from physician cost data and what are its “need-to-know” priorities.

Map the approach. Sketch out an initial process for physician costing, including any assumptions regarding physicians’ roles in the process.

Build the costing structure. Start with the information available now. For example, the process might begin with RCC data on the understanding that a transition to RVUs will be required to achieve the desired granularity of information.

Get feedback and refine. Share the data with key executive and physician leaders and educate them on what insights it provides and how it differs from cost data they have seen before. Use their feedback to refine the costing structure.

Tolerate imperfection. Data need not be perfect before it is shared with stakeholders; more important is transparency about how the data was collected and what it can show and what it cannot.

Once the costing structure is in place, the addition of more refined costing units (e.g., RVUs instead of RCC) and costing techniques (e.g., assignment of physician costs to sites of care depending on average time spent at different sites) will add both specificity and value to the information provided by cost reports. Again, transparency about how the data is collected and what insights it provides will continue to build trust in the data.

The value of physician cost data extends across multiple dimensions. It can contribute to:

- Service line analysis, by supporting cost and margin analysis across care settings (hospital, medical group, home health, etc.)

- Financial planning, by supporting full business case development across many strategic initiatives

- Physician analysis, by providing comparative physician data on costs and utilization and identifying areas for executive and managerial focus on unwarranted variations in care and cost reduction opportunities

- Pricing and contracting, by informing negotiations that secure payments sufficient to ensure full cost coverage.

Physician costs should be an integral part of any health system’s performance improvement and cost transformation efforts. Taking time to plan for the expansion to physician costing and to educate key stakeholders on the process and intended results will help ensure a successful costing initiative. The right cost accounting solution will then provide a powerful tool to define, understand and address physician costs.