Financial Sustainability

3 steps for executing an effective consumer-driven physician strategy

November 24, 2020

3:33 pm

Healthcare providers face unprecedented pressure to meet consumers’ needs and expectations. This strong imperative has been driven in large part by the uncertainties COVID-19 has created, which have added to consumers’ anxiety and prompted them to look to providers for help and guidance.

Yet many providers, including hospitals, health systems and physician practices, have been slow to develop a strong consumer-focused strategy. Traditionally, providers have tended to be slower-moving organizations focused on making operations work well for their physicians, nurses and other staff. As a result, by and large, healthcare still tends to be less focused on consumer experience or convenience than many other industries.

Providers should take a lesson from banking. At one time, banks required customers to get in a car, drive to the bank and stand in line for a teller to complete a transaction. Now, even ATMs are passé; we use our phones to make deposits, pay bills and complete most banking transactions.

Now that patients can interact with providers virtually, consumers want continued access to healthcare, as fast as they can get it, at low cost, with as little bureaucracy as possible. Although some pent-up demand for elective procedures will re-emerge once the pandemic is under greater control, about 74% of consumers responding to a recent survey reported they plan to make fewer hospital visits for care after the COVID-19 pandemic.a More than 90% of consumers surveyed expressed fear of visiting a hospital for elective procedures, and 50% expressed concern about their ability to manage their healthcare post-COVID-19.

Physicians and health systems (including hospitals) that collaborate continuously on improving the consumer experience and bringing decisions as close to the consumer as possible will win in the emerging post-COVID-19 world.

Health systems, therefore, should form a consumer-experience planning team composed of physician leaders and representatives from finance, strategy, marketing, technology and transformation/innovation to pursue the three broad steps described below, which are aimed at a creating consumer-driven physician strategy. (For a further discussion of today’s industry-shaping factors, see the sidebar to this article, “COVID-19’s impact on healthcare drives the need for a consumer focus”).

1. Work with clinical leaders to design care delivery focused on the consumer

Assessing the shifts in consumer preference about virtual and ambulatory care will provide a basis for designing a consumer-facing market strategy. The strategy also may require further integration of primary and specialty care, including:

- Greater use of team-based care approaches to support communication among primary care physicians, specialists and APCs, with the use of integrated care plans for chronic disease treatment and management

- Risk-stratified care management and care coordination for complex cases bridging primary care and specialty visits

- Greater use of APCs in procedural specialties to efficiently utilize operating room time

- Balanced compensation models incorporating the Triple-Aim of improved outcomes, improved patient experience and reduced costs, among other incentives

Greater use and integration of consumer-facing applications, such as patient portal web applications and mobile apps, can be considered to enable a broad range of service and other improvements, including:

- Centralized scheduling

- Improved patient-physician communication

- Virtual care and telemonitoring

- Efficient delivery of test results

- Timely presentation of reminders and alerts for needed services

- Capture of outcomes and patient experience data

- Patient self-management, particularly among patients with chronic diseases

- The requisite realignment of services includes new design elements to offer innovations beneficial to consumers, such as:

- Digital triage for urgent care

- Digital-first providers

- Seamless “plug-and-play solutions” for staffing and scheduling

The health system’s technology and analytics may need to be reinforced to achieve the full potential of digital health.

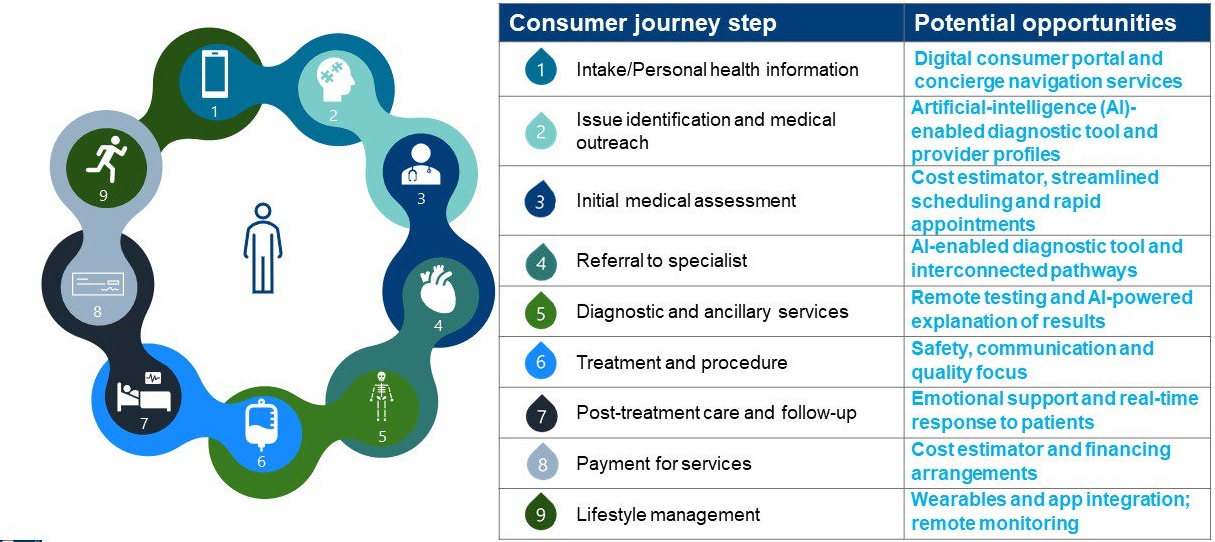

Considering that every healthcare consumer encounter differs, the exhibit below presents the consumer’s generic healthcare journey, as steps in a continuum, and potential opportunities for physicians and health systems to make the consumer experience more efficient and personalized.

The healthcare consumer’s journey

Source: BDC Advisors, 2020

Key questions for health systems to consider during this step are:

- When was our last consumer survey?

- What services need to be enhanced to connect to the consumer across the continuum?

- How are we making in-person activity safe?

The immediate focus for physicians during this step should be to:

- Develop new consumer approaches

- Update digital tools and analytics

- Promote new care processes

2. Partner with physicians to refresh network strategies and offerings

Health systems and physicians should treat recent developments as an opportunity to conduct a disciplined analysis of the current ambulatory portfolio to identify which assets and sites are most critical to their future mission and contribute to future financial sustainability. They should comprehensively review utilization of physical facilities to identify underperforming assets with an eye to either fixing or closing them. This review should be coupled with planning for flexible workforce management that ensures staffing and demand are aligned to meet consumer expectations.

Once the planning team understands and agrees on the future service mix changes, their next step will be to assess the implications regarding necessary changes to core infrastructure (including facilities, the supply chain and IT support) and the financial resources needed to bring the infrastructure in line with the projected future market and services.

This review should include attention to new modalities, including possible expansion of home-based and non-hospital-based ambulatory care to provide care for the growing population with chronic conditions. Between now and 2025, the over-65 population will grow four times faster than the general population. This rising older population also will be prime targets for integrated telehealth services and home care services.

Key questions for health systems to consider are:

- Is our current physician network at risk for being disrupted?

- How can we make our network more agile and better connected to the consumer?

- Are there opportunities to develop additional products and services to relieve consumer anxiety, provide safety and meet new expectations with alternative modalities?

The immediate focus for physicians should be to:

- Recalibrate physician operations, teaming and compensation

- Update physician affiliation/partnership models and strategy

3. Evaluate consumer-friendly technologies and consider partnering with enablers

During recent COVID-19 lockdowns, consumers found different ways to access needed care through new technology-enabled services, including telehealth and subscriptions to virtual care with primary care and behavioral health providers. Although traditional healthcare organizations have scrambled impressively during 2020 to offer such innovations, the disruptive trend was already strong prior to the onset of the pandemic.

Because of the substantial capital investment and technology expertise required, these trends have been led by a menagerie of nontraditional provider organizations, formed by health plans, private equity investors, venture capitalists, pharmaceutical and biotechnology manufacturers and even large employers. Some of these new entrants are pure-play healthcare providers, hiring licensed professionals to deliver care. Others work by partnering with traditional healthcare organizations. As a result, physicians enjoy a growing set of options for where and how to work, and for whom.

In any case, this new competition demands a thoughtful response from health systems and incumbent participating providers. If a disruptor can provide best-in-class performance and experiences for one component of the overall system, they can present a threat or an opportunity to achieve competitive differentiation. The pandemic shock has substantially shortened the strategic planning horizon.

Health system and physician leaders therefore should keep apprised of the growing number of start-up entrepreneurial ventures offering clinical services, interacting directly with patients and deploying their own enabling technology to achieve better health and economic outcomes compared with traditional medical group practices and health systems. (See the sidebar, “Tech-enabled market disruptors and opportunities,” below.) Such ventures have been described by Nirav Shah, MD, senior scholar at the Clinical Excellence Research Center, Stanford University, as “tech-enabled, full-stack clinical services” firms because they deliver both technology and services, not just one or the other.

Several disease-focused providers manage many of the aspects of care, including symptom monitoring, disease management and clinical follow-up. Their care models achieve lower costs and are better at improving outcomes than their traditional healthcare delivery counterparts.

Taking a page from concierge private practices, some disruptors are changing the fee-for-service economic relationship between physicians and consumers. They charge annual membership fees, partnership management fees or some other service premiums that, in some cases, add up to close to 50% of the primary care providers’ annual net revenue.

Partnerships between traditional provider organizations and such disruptors are generally aimed at specific clinical segments such as primary care, diagnostic radiology, oncology or others. The IT platform they utilize provides access to relevant data and supports care management for specific consumer segments.

Health systems also can form or expand their own strategic venture funds, increasing the degree to which they focus on ventures they plan to incorporate into their own integrated care processes.

Healthcare organizations unaccustomed to new venture partnerships, rapid care model shifts and challenging technology and data integration should work quickly to implement a process for developing their strategies, ideally piggy-backing on the decisive leadership structures currently assembled to address the COVID-19 challenges.

Key questions for health systems to consider are:

- How are we organized to evaluate, develop and invest in new partnerships?

- What capabilities do we have in place to earn a consumer’s trust?

- How will we differentiate our services from those of competitors going forward?

The immediate focus for physicians should be to scale with virtual aggregators to compete for consumers and delight them along the healthcare consumer journey.

No time to wait

Physicians and health systems have never had a more urgent need to pursue more consumer-driven approaches. The time is now for them to build loyalty and trust with consumers and physicians in their communities, following the advice widely credited to Winston Churchill: “Never let a good crisis go to waste.”

Footnote

a Betts, D., Korenda, L., and Giuliani, S., Are consumers already living the future of health? Deloitte Insights, Aug. 13, 2020.

Tech-enabled market disruptors and opportunities

Following are examples of disrupters that are entering the market within key services areas, and the service offerings some of them are introducing.

Primary care. Several primary practices have entered the market on a national level:

- One Medical is focused on consumerism and concierge services enabling technology to allow more time with patients, medical assessments using artificial intelligence (AI) and 24/7 virtual care.

- Oak Street Health is focused on value-based and full risk contracts, primarily for underserved Medicare patients using a highly standardized and scalable care model.

- ChenMed is focused on value-based and full risk contracts for Medicare and those with complex chronic diseases with “high-touch” physician-led primary care model.

Other organizations disrupting the primary care market include:

- 98point6

- Parsley Health

- Iora

Multispecialty. Leading entrants into the multispecialty space include the following.:

- OptumCare, now the largest employer of physicians in the nation, focuses on value-based care and eventually full capitation with a pluralistic approach to growth using medical group acquisitions, IPA acquisitions, IPA start-ups, IPA wraps and tuck-in acquisitions.

- Privia allows multi-specialty physicians to remain independent, supplementing their efforts with data-driven population health, wellness and patient engagement platforms.

Other leading multispecialty market disrupters include Mednax and VitalMD.

Urgent care. Prominent market entrants include Go Health and OptumCare.

Radiology. Teleradiology Solutions is a leader in this area, offering lower-cost radiology settings with the scale necessary to provide AI tools. RadNet and VRad are other leaders in this area.

Oncology. Two prominent disrupters are Twentieth Century Oncology, which owns cancer centers, and California-based Flatiron which offers a clinical-genomic database enabling oncologists to comply with NIH guidelines and use genetically guided treatments.

Diabetes. Disrupters in the diabetes service area include:

- Omada Health, which also focuses on hypertension management.

- Virta, which provides continuous care platform for type 2 diabetes that improves objective and patient-reported outcomes.

- Hygenia, which is a rapid microbiology testing and solutions company that specializes in managing insulin therapy.

Behavioral health. Lyra is focused on improving access to behavioral healthcare in acute scenarios such as suicide ideation, and tracks outcomes, even in patients not seeking care.

Hospice. Aspire, whose care protocols achieve a 65% increase in hospice transition rates, has reduced per-patient costs for care in the last year of life by $10,000.