Innovation and Disruption

10 Vital Responses to Healthcare Disruption

A report from HFMA's 2023 Spring Thought Leadership Retreat

July 11, 2023

2:07 pm

Disruption is reverberating throughout the healthcare industry, and it’s incumbent on legacy organizations to develop strategic responses for the benefit of their consumers, their communities and themselves.

With that overarching challenge becoming ever more pressing, HFMA’s 2023 Spring Thought Leadership Retreat brought together leaders from across the industry May 4-5 in Atlanta to consider approaches that can help hospitals and health systems fortify their positions.

Disruption is “a topic that’s both timely and critical to the future of healthcare,” past HFMA President and CEO Joseph J. Fifer (retired June 6) said as he kicked off the gathering.

The pressures stem both from industrywide forces such as the labor crunch and from the ingenuity and dexterity of disruptive entities. Perhaps most notably, such companies tend to be more intentional than traditional providers about creating optimal experiences for consumers.

“We are not as focused on the consumer experience as we need to be,” Fifer told attendees at the end of the retreat. “I would just encourage you to go back to your organizations and have that conversation. There are big, massively capitalized entities that are focused on the consumer experience. And if we’re not [similarly focused] as an industry, I think we’re making a big mistake.”

Reflecting on the question of whether disruptors can turn a profit in the healthcare space, Fifer said, “I believe that they will, and I believe they’re going to come right after that consumer experience.”

The concept of culture affects an organization’s ability to make the necessary adjustments, he added.

“What is culture in an organization? It’s a collective reflection of attitude,” Fifer said. “If the attitude that we take back to our organizations is that we really do care about keeping people healthy, we really do care about the consumer experience, we really do care about that electronic front door and making it as simple, as easy and accessible as using our phones, it will start to change the perception.

“And ultimately the trust in our organization, trust in our healthcare system, will begin to reverse this trend that we’ve been on.”

Sponsored by Guidehouse, Strata Decision Technology and Vizient, the retreat highlighted the key challenges and opportunities for stakeholders trying to navigate an industry being swept by change.

10 Vital Responses

1. Recognize the changing landscape

2. Address wasteful costs

3. Improve the cost effectiveness of health

4. Update your contracting strategies

5. Seek value-based payment opportunities

6. Accelerate consumerism strategies

7. Evaluate your care delivery model

8. Incorporate digital care

9. Maximize your reach

10. Be agile (and calm)

1. Recognize the changing landscape

Many hospitals and health systems face substantial risk in the current environment, according to insights shared during the retreat.

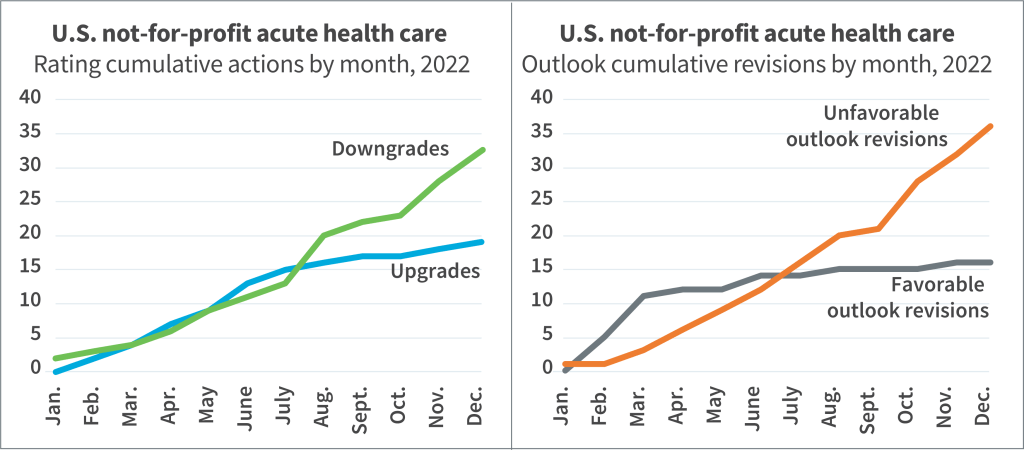

S&P Global Ratings has issued a negative outlook for the acute healthcare sector because of several factors, said Anne Cosgrove, director with the company’s U.S. Public Finance Healthcare Group. These include continued cash flow compression, waning unrestricted reserves and a negative bias in ratings and outlooks for individual organizations (see the exhibit below).

Financial results for 2022 came in “with very large losses,” she said. “And these losses run the gamut from small credits to large healthcare systems.”

S&P Global Ratings 2022 Rating Actions

Hospital margins sagged, spending much of 2022 in negative territory before inching up to 0.2% in December, according to a presentation by Vizient’s Jon Barlow, vice president for consumer innovation, and Tawnya Bosko, PhD, DHA, senior principal for value transformation. Meanwhile, major payers had operating margins of well over 5%.

Looking forward, “Things are stabilizing, but that doesn’t mean things are getting better,” said Aaron Wesolowski, vice president for policy research, analytics and strategy with the American Hospital Association (AHA). “We’re not seeing double- or triple-digit increases in expenses at this point, but we’re not seeing expenses come down. [And] the volume trends are kind of the new reality.”

The ongoing shift from inpatient to ambulatory settings also can have an adverse impact on margins, he added. The loss of regulatory waivers and flexibilities that were available during the pandemic compounds the difficulty, as does the disenrollment of potentially millions of Medicaid beneficiaries into next year.

Add it all up, and the threat seems existential.

At an industry level, “We’re watching hospitals close,” said Carol Friesen, CEO of OSF HealthCare’s Eastern Region. “If we don’t [adapt], it’s the mission we’re committed to that is in jeopardy.”

Sidebar: Why workforce-related disruptions are top of mind

2. Address wasteful costs

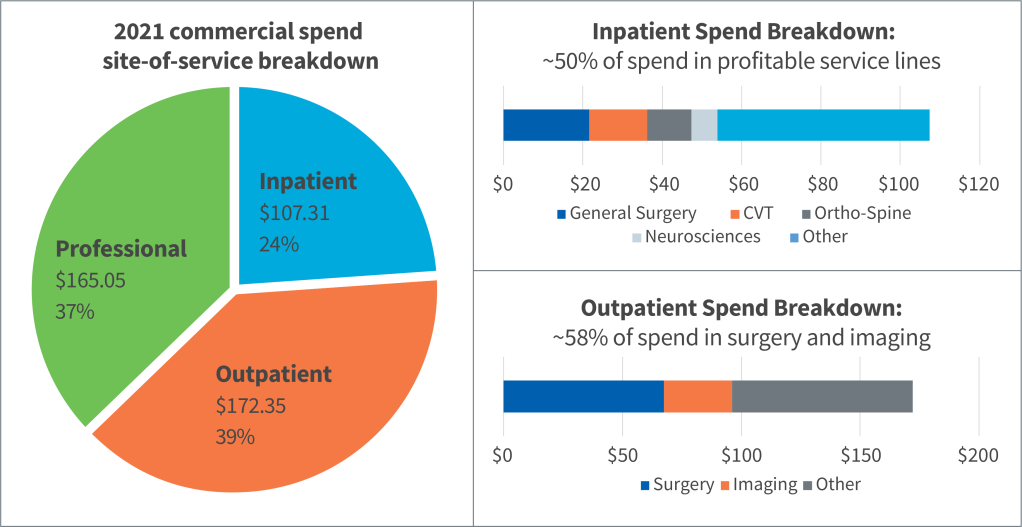

One of the most basic forms of healthcare disruption is the ability of new entrants to offer high-value services at lower costs. As they seek to match those competencies, including by addressing the fragmentation of care (see the exhibit below), providers should start by properly framing the issue.

“Purchasers want providers to reduce the total cost of care while maintaining or improving quality,” Fifer said. “And that doesn’t line up very well with this fragmented system that we have. Disruptors, especially [those] that don’t have the stand-ready obligations and the extensive infrastructure that hospitals do, can operate at a lower cost structure and thus potentially deliver more cost-effective care for the sliver that they’re addressing.”

Total Cost of Care Varies Based on the Degree of Fragmentation

Providers should tackle costs in a deliberate and thorough manner.

“We’ve started to see more organizations being really rigorous and thoughtful about their fixed and overhead expenses, their administrative areas,” said Alina Henderson, vice president for solutions and marketing with Strata, “and really saying, ‘Do we have ROI in this?’”

For example, OSF HealthCare made a push to examine “our overall structures, our organizational structures, doing some reorganizing, looking at our corporate offices,” said Kirsten Largent, senior vice president for financial operations. “We haven’t done a great job in the past at really leveraging our scalability and focusing on getting those costs down.”

With such approaches, there’s no getting around the fact that tough decisions have to be made about resources — including human resources.

“We have a cost structure issue within healthcare,” said Bryce Gartland, MD, hospital group president and co-chief of clinical operations with Emory Healthcare. “There are ways of [addressing] it with attrition and [staff] repositioning and the like, but I do think we need to not kid ourselves in terms of the administrative cost structure issues that we’ve got to address from an industry standpoint, and frankly productivity even down to the frontline level.”

3. Improve the cost effectiveness of health

Matching the value proposition of disruptors means innovations should be geared toward keeping patients out of the hospital, even if that approach affects the finances of traditional hospital operations.

“It’s not only the cost effectiveness of healthcare that’s important. It’s also the cost effectiveness of health,” Fifer said, referring to the strategic focus HFMA is championing for the industry.

“As a society, we spend the vast majority of healthcare-related dollars on healthcare, not on the social determinants of health and the behavioral factors that largely determine an individual’s health status,” Fifer added. “The resource allocation is not sustainable in this way at a societal level. It’s not going to yield the improvements and outcomes that care purchasers expect and deserve.”

Even implementing initiatives geared to the social determinants of health (SDoH) won’t be adequate to counter disruptive entities that are finding ways to lower the total cost of care on a per member per month basis, Fifer said. In centering efforts primarily on SDoH, “You may wind up channeling resources to initiatives that, though well-intended, do not move the needle on achieving cost effectiveness of health and do not reduce healthcare stakeholders’ vulnerability to disruption.”

Hospitals recognize the shift in incentives, said Lindsey Dunn Burgstahler, vice president for programming and intelligence with the AHA’s Center for Health Innovation.

“The profit in healthcare is going to go [toward] keeping people healthy or, if they have chronic conditions, keeping those managed,” she said. “We’re really not set up for that. We are working toward being set up for that.”

For example, Burgstahler said, “We have seen hospitals really amp up what we label their anchor strategies,” looking to enhance such strategies through both community investments and systematic handoffs to community partners.

One challenge is establishing the data collection processes and caliber of analytics that can guide resource allocation in such initiatives, she added.

4. Update your contracting strategies

A disruptive environment necessitates a new emphasis on achieving optimal terms with payers.

“There’s been an acceleration of volume that’s moving from acute care out, and we have to figure out where we want to put our pricing strategies,” said Richard Bajner, partner and payer/provider leader with Guidehouse.

Providers also should be cognizant that health plans in the current environment are focusing on Medicare Advantage (MA) as a driver of revenue (for more on MA, see the sidebar below). Thus, health systems should emphasize their value proposition in areas such as total cost of care and their impact on the health plan’s MA star rating, said Vivek Gursahaney, director with Guidehouse.

Likewise, for a growing number of payers in the commercial space, “Their focus is entirely on value-based care,” Vizient’s Bosko said. “No more fee-for-service rate increases unless you can show the quality and outcomes, and hopefully that you’re not the highest-cost-of-care provider in the market when health systems frequently don’t even know if they’re a higher- or lower-cost care provider in their market.”

Given all the challenges, Ascension has made a point of shoring up its contracting approaches, said Michael McMillan, senior vice president for payer contracting and payer relations.

“If you are a health plan, you know when you’re across from HCA because they have a way of behaving that lets folks know what they want and what they need,” he said. “I don’t know if that’s true on the not-for-profit side. Certainly, at Ascension, we haven’t taken the perspective [that] we’re here to get, respectfully, everything that we need.”

More recently, the organization’s approach in negotiations has been to make clear “what we want, backing it up with data and facts and making sure that we can achieve it.”

5. Seek value-based payment opportunities

Bringing the right mindset to value-based payment (VBP) initiatives is important because the finances don’t always line up at first glance.

“Value-based care is known for reducing utilization,” Bosko said. “Most health systems are going to say, ‘How are we going to offset the changes in utilization — because that financial impact is more than any shared savings I’m going to get.’ You have to think about it as growth in managing populations, growth in lives.

“It’s a different lens to think about growth, but it still is growth all the same.”

In terms of opportunities for shared savings, risk-based contracts with commercial insurers are less advantageous compared with such contracts in Medicare fee-for-service and Medicare Advantage.

“The [commercial] payer’s definition of value-based care is site-of-service utilization with steerage,” Gursahaney said. “It’s aggressive utilization management and denials, and it’s basically low unit-rate increases.

“If they can push you to risk, they’ll do it, but the model for them has very little to do with [providers] engaging in shared savings contracts.”

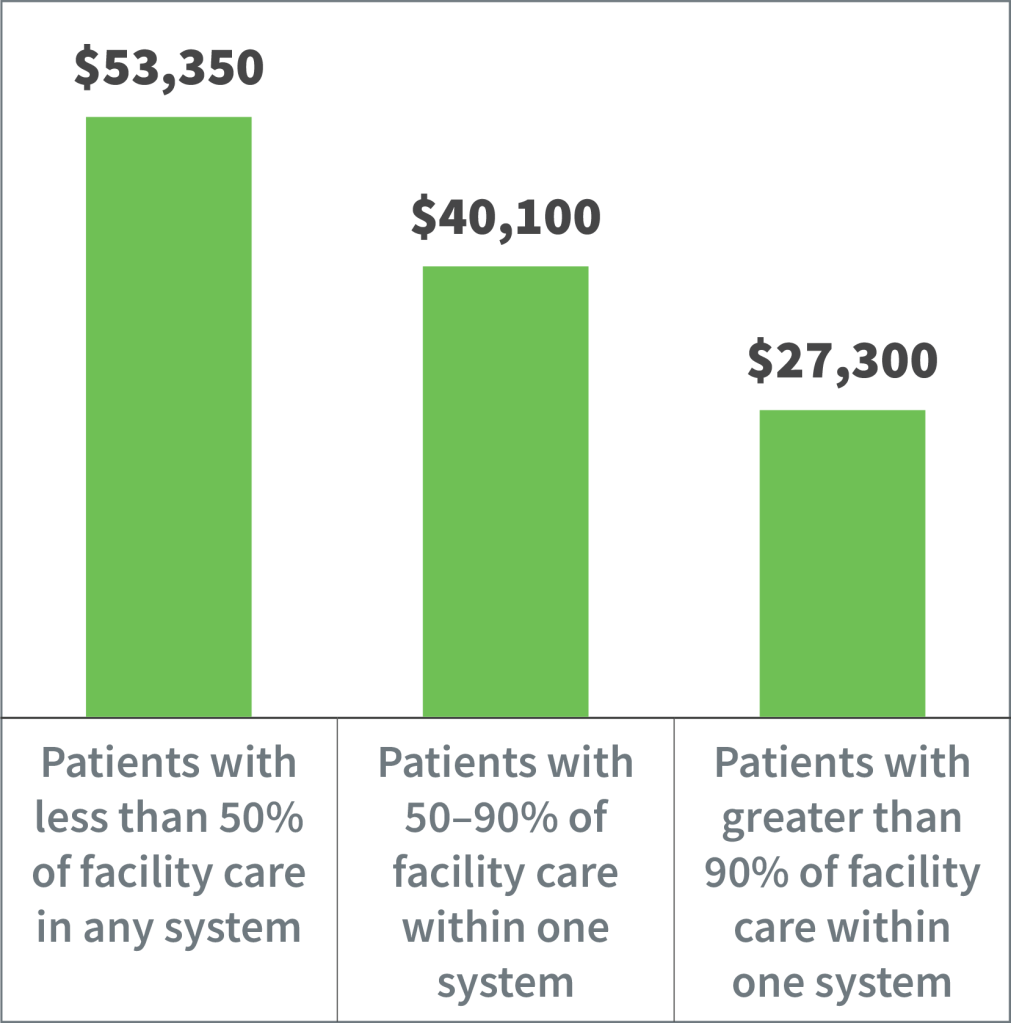

Commercial VBP contracts also can be less lucrative because commercially insured patients are more likely to engage with profitable service lines (see the exhibit below).

Said Gursahaney, “How do you make sure that you’re aligning your shared savings rate with your contribution margin from that payer?”

Systems Challenged to Meaningfully Reduce Commercial Costs Without Cannibalizing Most Profitable Services

Fifer said hospitals and health systems are approaching “a fork in the road” regarding the approach to risk.

“Either do a deep dive and have a significant amount of your revenue that’s at risk, whether that’s through having a health plan within the organization or a very significant upside and downside risk environment — you’re going to have to go deep where you can justify the investments in that,” he said. “Or go the other direction. And that is to pull back and be an incredibly efficient provider of care within that insurance process.”

6. Accelerate consumerism strategies

“Loyalty to healthcare brands is fragmenting,” according to the presentation by Vizient’s Barlow and Bosko. In response, “health systems must move beyond traditional marketing and brand building to deep market analyses and retail-inspired relationship building.”

The stakes are substantial, Guidehouse’s Bajner said, given that the difference between patient retention rates of 65% and 85% can equate to “tens of millions of dollars.”

With disruptors competing in part on their ability to manage the customer experience and customer relationships, an organization’s clinical reputation is “no longer sufficient” to gain market share, according to the Vizient presentation.

“Everybody expects you to deliver amazing, high-quality care,” Barlow said. “There’s a time and a purpose for brand marketing, but the days of putting up your quality scores or your U.S. News and World Report [ranking] on a billboard saying, ‘We have the greatest services,’ those are over because that’s not enough anymore.”

Gursahaney described the challenge as growing customer loyalty rather than the organization’s patient population: “If it’s in the ED, if it’s in the primary care office, if it’s for an ancillary test, those are all patients that we should eventually be trying to be sticky with and creating relationships with. That’s just a mindset change and a tracking and measurement change.”

Through that prism, the financial focus shifts to average revenue per customer rather than patient volume, he added.

In efforts to become more consumer-centric, organizations can start with the basics — including the patient financial experience.

“There is a ton of friction around understanding what something might cost you, the bill when you receive it, and then payment of that,” said Burgstahler of the AHA.

UCI Health in Irvine, California, is seeking to improve something as fundamental as the registration process for patients, said Tatyana Popkova, chief strategy officer.

“The language and vocabulary of what 80% of consumers look for when they want to transact or discover healthcare services, it’s not what we [traditionally had] put out there,” she said. “So, our digital front door creates that match.”

7. Evaluate your care delivery model

The pandemic highlighted the “considerable vulnerabilities” of a healthcare delivery system anchored by acute care hubs, Barlow and Bosko said. The system is evolving into new vertical integrations that are “purpose-built” to reverse patient flow across the system, reducing acute care utilization and spend.

In a market such as Las Vegas, Bajner said, only 1% of commercial outpatient surgery volume takes place in hospital outpatient departments. The rest has migrated to physician offices on the strength of disruptor models such as UnitedHealthcare/Optum.

Ascension’s McMillan added, “This is such an underrealized part of strategy. It goes back to, ‘We will never give up our HOPD.’ [Then] you will miss the market.”

Emory Healthcare is considering ways to right-size its services, Gartland said. “Do you really need to be doing everything at all locations?”

Such conversations “traditionally have been a third rail in healthcare,” he noted.

Massachusetts General Hospital launched an enterprise-wide asset management tool to glean insights that could lead the organization to shift volume among sites, said James L. Heffernan, consultant and CFO emeritus with Massachusetts General Physicians Organization. “What it really gets down to is: Are we using the facilities we have?”

Popkova said UCI Health generates 46% of its revenue from services that take place outside the hospital. “We’re trying to balance our portfolio that way to make sure we diversify risk, but also following the market trend,” she said.

Strategic changes to the care delivery model should be the product of sustained collaborative ventures between finance, clinical and operations teams, Strata’s Henderson said. “You have to bring those three groups together.”

Some organizations try to get clinical leaders to own financial accountability, she added, but a better approach is for such leaders to keep their focus on costs within specific DRGs or service lines.

“The key here is not having everyone looking at everything all of the time,” she said. “Oftentimes, that’s where we’ve seen organizations really slow down.”

8. Incorporate digital care

A key part of an updated care model is a digital care platform that can make high-quality healthcare more seamless and convenient. As with other aspects of the response to disruption, traditional providers must shift their thinking.

Ann Mond Johnson, CEO of the American Telemedicine Association (ATA), referred to the healthcare industry’s “edifice complex.” In other words, “We’re very tied to our bricks and mortar.”

In implementing changes, she added, “Culture trumps everything. It’s really the values and the beliefs of the organization, this idea that, ‘I’m doing this not because of the reimbursement. I’m doing this because we have fundamental problems in the healthcare system that we cannot address unless we deploy technology differently than we have in the past.’”

Given ongoing and future labor dynamics and increasing demand by an aging population, among other issues, “We’re going to be asked to do more with less, and we’re going to be asked to do it better than we used to,” said Adam Hornung, executive director of operations with Intermountain Healthcare.

“That isn’t a hypothetical. We’ve already seen moves in that direction.”

Considering the population of Intermountain’s markets, for example, “I should be hiring 15 neurologists for our system,” he said. “If I try to post and hire for 15 neurologists, it’s just not going to happen.”

By crunching the data, Intermountain leaders identified migraine headaches and low back pain as the main reasons for neurology referrals. Such cases can crowd out more urgent issues such as stroke and dementia.

But in a pilot program using e-consults in the primary care setting and video visits with advanced practice providers, only nine of 200 patients ended up having to see a neurologist.

9. Maximize your reach

Incorporation of digital health is, in part, a manifestation of the effort to improve patient acquisition and retention.

As part of its strategic focus coming out of the pandemic, Emory is “focusing very heavily on access,” Gartland said. “How do we make sure that we’re able to never say no?”

“There’s always latent capacity that is never uncovered because we don’t take the time to really pull back the covers and look at processes, whether it’s processes for referrals or scheduling,” Vizient’s Barlow said. “Those types of things are very low-risk but high-reward benefits. This is a new set of levers.”

“All of us get trapped into a usual way of doing business on stuff,” Gartland said. “Think about: How would Chick-fil-A come in and work on clinic throughput? They’re phenomenal at how they get drive-throughs going. We [in healthcare] stink at patient throughput.”

Traditional providers can enhance access through partnerships with disruptors, most of which seem hesitant to enter the acute care space. For example, UCI Health seeks to partner with companies that specialize in telehealth or home-based care.

“We don’t have the strength in our balance sheet to do everything alone,” Popkova said.

Critically, access improvement strategies factor into industrywide efforts to improve health equity, said Johnson of the ATA. But such progress will require significant investments to ensure high-speed Internet is widely accessible.

“The challenge is how we make sure that everybody bears the investment in a way that makes the most sense for the payoff that they’re going to get,” she said, referring to healthcare and government stakeholders. “Those are the issues that we’re going to have to address if we really want to get to this idea of ensuring that everyone gets care where and when they need it.”

10. Be agile (and calm)

As daunting as the task of responding to disruption may seem, hospitals and health systems can be methodical at first.

“The organizations that we see driving sustainable and successful change start small and humble initially but quickly pivot into a very aggressive change rollout within their organization,” said Frank Stevens, chief growth officer with Strata.

Said his colleague Henderson, “Break everything down into the smallest possible piece, and you will find it easier to make progress. With all of the challenges that your teams have been going through over the last few years, wins are great, and wins are exciting.”

The pandemic and ensuing struggles have brought a sense of urgency that hospitals and health systems should channel.

“Change management has never been easier than what it is now — because there is an overwhelming need to change,” OSF HealthCare’s Friesen said. “Some of this work has needed to be done for a very long time.”

A final note from experts: Don’t panic. Many disruptors are proving not to have all the answers just yet, at least when it comes to achieving financial returns. And few if any seem eager to take on acute care.

“Don’t be scared of this disruption,” Barlow said. “Utilize some of the tactics they’re doing, some of the approaches, the acquisitions that they’re making, and learn from it and try and adapt it to your situation in your organization.”

Why workforce-related disruptions are top of mind

Asked about the foremost challenges facing hospitals and health systems, Carol Friesen, CEO of OSF HealthCare’s Eastern Region, had a succinct response.

“Labor, labor, labor,” she said during a panel discussion at HFMA’s Spring Thought Leadership Retreat.

“Really everything related to [labor] — the retention, the recruitment, the stabilization,” Friesen added. “Unlike so many other times when we’ve had labor challenges, [the pandemic was] the first one where it was across the board,” affecting frontline workers, nurses and physicians at different points.

According to data shared in a presentation by the American Hospital Association’s Aaron Wesolowski, hospital labor expenses between 2019 and 2022 rose by 20.8% overall and 24.7% per patient (even when accounting for increases in patient acuity).

One source of relief for many organizations in recent months has been a reduction in contract nursing labor as more RNs return to full-time employment. James L. Heffernan, consultant and CFO emeritus with Massachusetts General Physicians Organization, mentioned seeing decreases of about 20% in traveler costs.

Conversely, though, an increasingly competitive market for full-time staff could alter cost structures.

An issue “that’s a little bit worrisome is avoiding fixing some of the costs at the level they are,” Heffernan said.

Academic medical centers may be able to help by evaluating how they train the next generation of clinicians, especially given telehealth’s potential to increase the efficiency of clinical operations.

“We want to make sure that we provide an environment where the new generation of practitioners train also in telehealth,” said Tatyana Popkova, chief strategy officer with UCI Health. “We don’t want to train them in the environment where they have to relearn and readapt because they’re coming from this traditional academic medical system that really is no longer traditional.”

Medicare Advantage: A leading vehicle for disruption

As the program technically known as Medicare Part C steadily overtakes the traditional Medicare program in beneficiary volume, healthcare providers should take stock of the consequences.

In January, Medicare Advantage (MA) edged past the 50% mark in its share of total Medicare enrollment, with 30.19 million out of 59.82 million beneficiaries. That’s up from 29% a decade ago.

“Most of you are dealing with Medicare Advantage as the primary Medicare segment in your markets today,” Tawnya Bosko, PhD, DHA, senior principal for value transformation with Vizient, said during HFMA’s Spring Thought Leadership Retreat.

MA is a platform for big payviders to control the longitudinal journeys of frequent utilizers of healthcare, said Bosko and colleague Jon Barlow. They shared data showing enrollment increases of more than 9% for UnitedHealthcare and Humana between 2018 and 2022, while fast-risers CVS Health (16.8%) and Elevance (18.4%) solidified their positions.

The rapid growth of the MA program poses a challenge to hospital revenue, Bosko said.

“How many of you think Medicare Advantage is negotiable for your systems? In general, it’s going to reimburse on a fee-for-service basis, and then you’re going to [adjust for] administrative burden, and the net impact is less than Medicare fee-for-service reimbursement,” she said.

In other words, “You’re losing every time a patient switches from fee-for-service to MA,” said Richard Bajner, partner and payer/provider leader with Guidehouse.

He added, “Your unit reimbursement is probably 7, 8, 10% less on Medicare Advantage because of denials, bad debt, etc.”

Such issues highlight why providers would do well to set their MA unit prices above 100% of Medicare fee-for-service rates, Bajner said. Many health systems set their prices at the 100% mark, “and then all that downgrade just contributes to degradation.”