Financial Sustainability

Why the physician’s office, not the ED, is a health system’s true front door

Published

June 25, 2021

9:49 pm

|

Updated

November 7, 2022

8:42 am

Sponsored by Kaufman Hall

The long-held notion that the emergency department (ED) is the front door to the hospital remains pervasive. However, the underpinnings of this conventional wisdom have shifted in some very significant ways.

Three factors have shifted the focus away from the ED as the hospital’s front door.

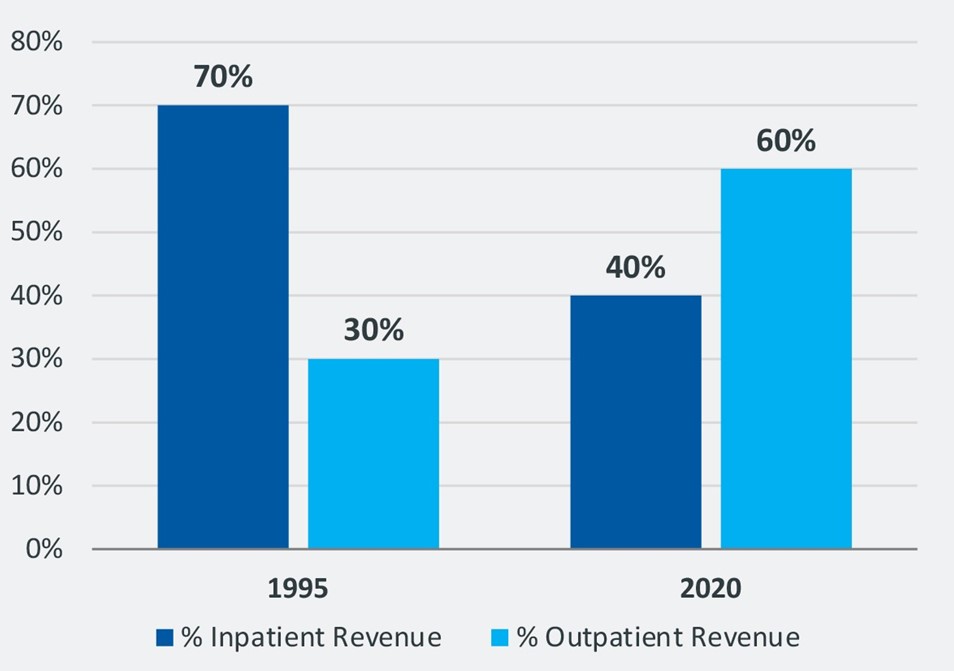

1 Inpatient revenue no longer makes up the lion’s share of a hospital’s total revenue. Back in 1995, inpatient revenue made up 70% of hospital revenue, according to the American Hospital Association. Over the past 25 years, however, we have witnessed a powerful macro-trend in the shift from inpatient to outpatient utilization for a broad range of procedures and conditions. And with that shift in utilization has come a shift in the percentage of total revenue. In 2019, prior to the COVID-19 pandemic, outpatient revenue made up 60% of total health system operating revenue, according to a recent Kaufman Hall analysis.

Percentage inpatient versus outpatient revenue

So while the ED may be one path to inpatient admissions, inpatient admissions no longer predominate health system revenue.

2 In a world of value-based payment, the ED is a bad front door. Most everyone under risk-bearing payment arrangements who seeks care in the ED poses a liability, not a help, to a health system. . From the point of view of value-based care, most people who visit an ED end up there because the system has failed to manage their health in a manner that avoids a medical emergency.

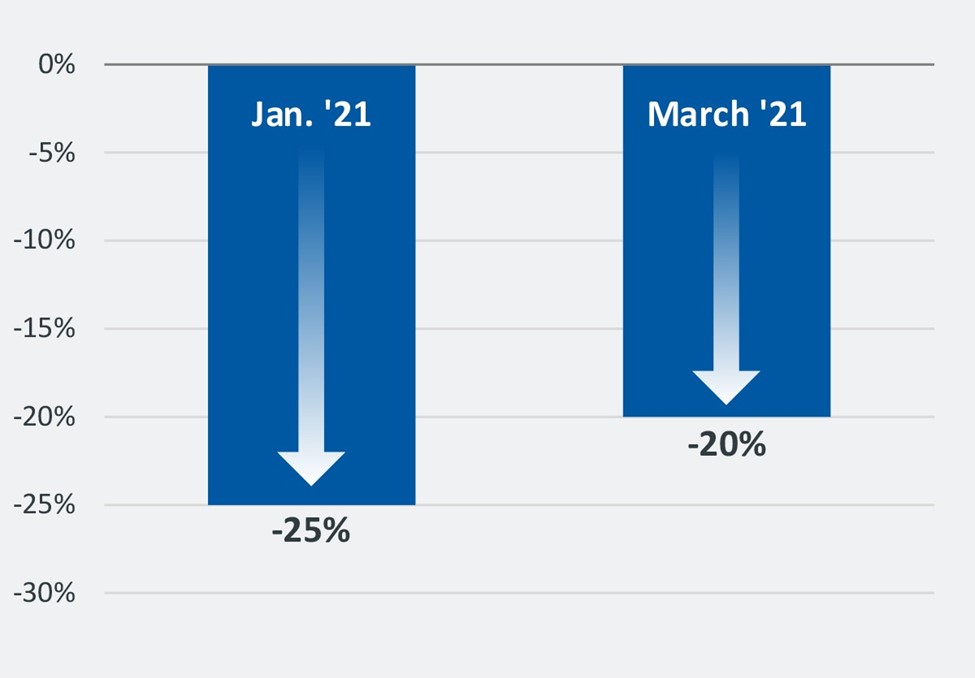

3 One of the strongest and, so far, most lasting effects of the COVID-19 pandemic has been a precipitous drop in ED visits. At the height of the pandemic’s first wave, in April 2020, ED visits were down 43% year-over-year. At the height of the pandemic’s third wave, in January 2021, ED visits were down 25% year-over-year. And as of March 2021, ED visits were still down 20% from pre-pandemic levels.

Percentage decline in emergency department visits in January and March 2021 relative to pre-pandemic levels

G. Mark O’Bryant, president and CEO of Tallahassee Memorial HealthCare, echoed the thoughts of many CEOs when he told us recently “I’m not sure ED volumes will ever go back to where they were, at least on a case mix or a percent-of-population level.” In other words, the industry is likely to see a permanent decline in patients entering health systems through the ED as a front door.

All of which begs the question, if the ED isn’t the health system’s front door, what is?

A new front door

From our point of view, the answer is the physician’s office.

The health economics of today demand that successful organizations do two very basic things incredibly well. Both put the physician center stage.

1 Success depends on increased consumer volume and loyalty. In the economy as a whole, Amazon is the poster child for this approach. Its unprecedented traffic and loyalty give Amazon the opportunity to aggregate a huge variety of products and services, to cross-sell endlessly, to sell subscriptions and to even sell services to other companies based on the infrastructure Amazon has built.

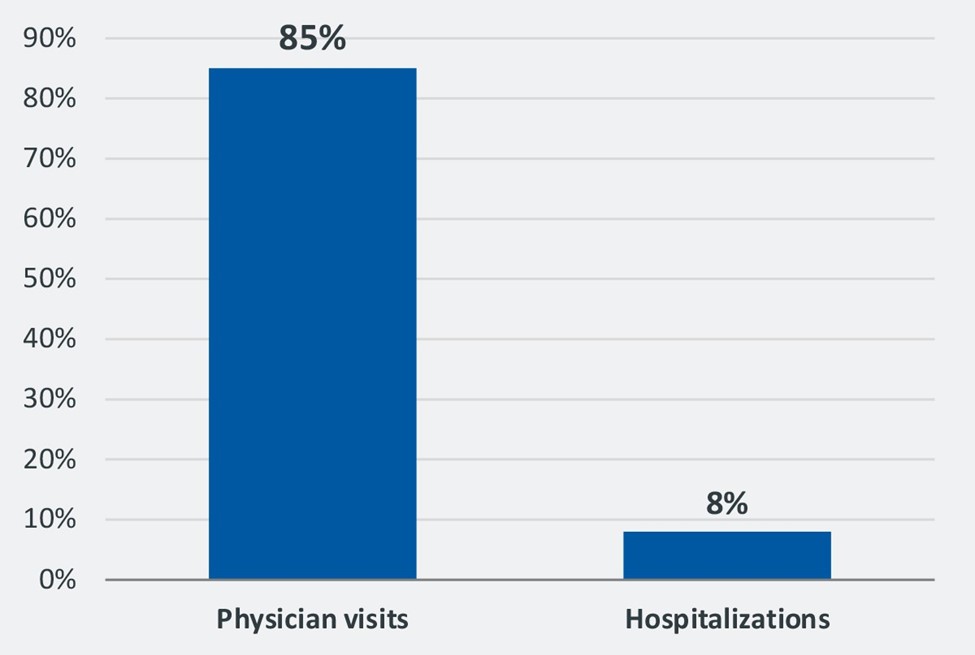

In healthcare, physicians are the key to both volume and loyalty. Almost 85% of the U.S. population visits a physician in the course of a year, compared with only 8% who are hospitalized overnight. The nation sees 883 million physician office visits each year, compared with only 36 million hospitalizations.

Percentage of population having physician visits versus hospitalizations

2 Success in today’s health economy requires managing the total cost of care. With perpetually downward pressure on payment and a financially unsustainable system as a whole, controlling total costs is really the only path forward. When it comes to the cost of care, the physician has more influence than any other individual. Physicians — especially primary care physicians — focus on keeping people healthy and therefore out of expensive treatment settings. And given the power of their s keystrokes in determining medication, supplies and treatment regimens, physicians control resource utilization to a great extent.

Optum certainly has health economics figured this way. As we have seen over the past few years, Optum has quietly invested in pretty much everything except hospitals, with an emphasis on physician practices. Having so far accumulated more than 50,000 physicians and targeting 75 major markets in the future, Optum sees physicians as the means to amass consumer volume, maintain loyalty and control costs through, among other techniques, narrow hospital and ancillary service referrals.

Kaiser Permanente also has structured itself around this concept of the health economy. The health system’s emphasis is not on hospitals and inpatient care, but on managing care in the least expensive setting, including a years-long push toward virtual care. Already in 2016, more than half of Kaiser’s physician visits were done virtually.

In the long run, the systems that will emerge as the most effective and successful will be those that take to heart the concept of physicians as the front door by focusing on access and retention.

These systems will track and perform at high levels for a new set of metrics that are far more sophisticated than simply tracking volume or revenue. Examples of such metrics include:

- Access: Percentage of patients requesting a same/next day appointment who are accommodated. With the large number of healthcare access options available today, if a health system doesn’t see its patients, someone else will.

- Access: Percentage of patients requesting visits who are seen within two weeks. In today’s climate of convenience, consumers will not tolerate waiting longer than two weeks for an appointment unless they have a strong existing bond with the physician, and health systems should expect that their competitors will know this.

- Access and retention: Percentage of patients calling for appointments versus patients actually seen. Too often, patients contact a physician office or health system to schedule appointments but either give up because of scheduling challenges or do not show up for the appointments because someone else saw them sooner

- Retention: Percentage of new patients that return for a second visit/service. It’s not enough simply to see new patients. Patient loyalty is measured by how many new patients show up for follow-on visits and services.

- Retention: % of patients who are seen by system physicians, referred for additional diagnosis/treatment and receive the additional service. Patients referred by physicians for additional services within the system but for one reason or another do not show up for those services are a huge lost opportunity for maintaining patient health and loyalty, which translates into lost health system revenue.

In areas such as these, best practices should be understood and implemented, and high-performing service lines and physicians should be studied and celebrated.

A welcoming front door

As the true front door for healthcare, physician practices are much more complex and diverse than the ED. Ensuring that physicians serve as an effective front door requires vision, dedication and sophistication in design, strategy and operation. Moreover, physicians will prove to be a strongly effective front door if the health system is solidly committed to being a more meaningful part of community health and a more financially successful enterprise in the future.