Benchmarking and Forecasting

Why Healthcare Forecasting is a Combination of Art and Science

Published

May 19, 2019

11:27 pm

|

Updated

November 27, 2024

10:18 am

Even though healthcare organizations have more refined data today than ever before, many organizations’ key healthcare financial forecasts — particularly where new ventures or integrated activities are involved — have often been far off base. Consider the following scenarios:

- A highly respected, innovative health system finished 2018 with an unexpectedly large loss. New value-based contracts were part of the problem.

- A physician network is having trouble “moving the needle” in expanding its patient base to levels projected to be achievable. New incentive structures from a health system parent were part of the problem.

- A state is having more difficulty than expected introducing a new healthcare payment model for its employees. Differences in payer/provider expectations, cultural differences, and data limitations are taking longer than expected to address.

Forecasters must judge when and how to introduce new change factors into their forecasts.

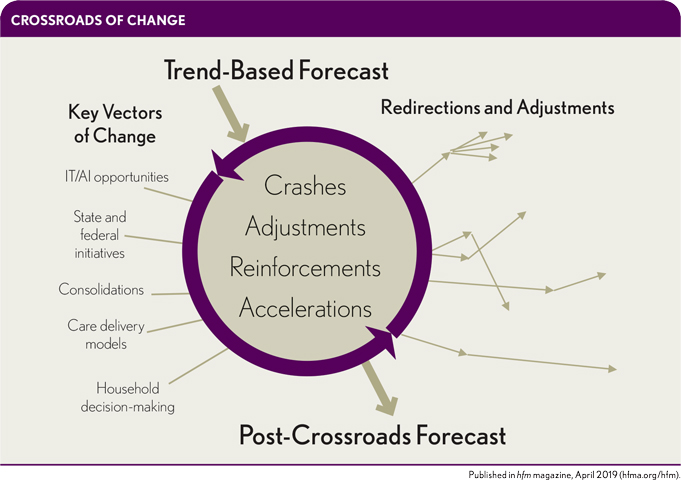

Vectors of Change

Healthcare leaders need to respect the complexity and nuances of some of today’s key decisions. Clearly, a forecast is based on an analysis of related costs and trends, but the forecaster also has to consider the likelihood of predictions encountering a crossroads where several vectors of change intersect. See the exhibit below.

Consider the following vectors of change.

IT and artificial intelligence (AI). Large new investors (e.g., Apple, Amazon, Google, Berkshire Hathaway), well-established innovators (e.g., IBM, Kaiser Permanente, Partners Healthcare, Intermountain Healthcare, Providence Healthcare, Optum, Humana), a new generation of start-ups, and many combinations of these players are investing record amounts in new approaches to health care.a Thus far, these new investments have not had a major impact, but that’s not likely to continue to be true. Many expect an explosion of new AI initiatives, affecting areas ranging from the revenue cycle to care delivery models.b

State and federal initiatives. As expected, many states are experimenting with new approaches to Medicaid (including, for example, integration of physical and behavioral health services). Others are looking at reference-based pricing of services and/or pharma. Meanwhile, the Centers for Medicare & Medicaid Services (CMS) and states are interested in new value-based payment models. CMS and several states are pursuing parallel actions to address social determinants of health, such as housing.

Consolidations. Mergers, joint ventures, clinically integrated networks, and other forms of consolidation already have had a major impact. These opportunities are not slowing. In fact, new opportunities for consolidation are being explored, including joint initiatives in AI.

Models of care. Health systems are beginning to reassess how they combine physicians with other resources in delivering managed care. Home care for the highest-risk patients is reemerging.

Household decision-making. Families are learning to adjust the role of health care in household budgets. For some population segments, households have some years of spending more than their high deductible, and other years of spending close to zero.

What Happens at the Crossroads

Where these vectors of change meet at the crossroads, the effect is likely to be dynamic.

There will be accelerations. For example, AI may play an increasing role in some diagnoses, and it also may play an important role in directing care for some segments of the population. For example, “Alexa, here are my symptoms. Should I see a specialist or a general internist?”

There also will be collisions. For example, there likely will be a winnowing out of competing organizations providing AI solutions in health care. And some consolidations that have proven to be duds have been quietly closed, while others have been folded into other initiatives. It’s understood that a fraction of new start-ups will be successful, but somehow, we are surprised when the same is true for consolidations.

There will be transformations. AI may become its own form of consolidation, or it may link to existing trends in consolidation. AI may lead to new partnerships between tech companies and providers and/or payers. Meanwhile, models of care are undergoing wholesale changes, to where many physician decisions are now being made by health systems. And patient-physician-payer interactions have changed significantly from five years ago.

The opioid crisis and high-deductible health plans also are major drivers of change, with the result that both treatment options and costs of care are showing signs of diverging for different socioeconomic segments of the population. And the use of voice devices, such as Alexa, in place of written communication has the potential to further differentiate the ways some population segments make healthcare decisions.c

Obstacles to Accurate Forecasts

All these factors point to some common impediments to healthcare organizations’ ability to provide usable forecasts. The forecaster’s art lies in deciding when and how to introduce the right vectors of change.

Ignoring the vectors of change. The longer the forecasting period and the more strategic the forecast for the whole enterprise, the less defensible it is to ignore these changes.

Overestimating how quickly changes will occur. Perhaps the most common problem is that the forecaster recognizes the importance of the new vectors but over-corrects for them. Although the change factors are likely to radically alter healthcare finance trends over time, the change will occur slowly at first. Organizations have learned, sometimes the hard way, that just because a new approach can lower costs or improve care, change will happen quickly. The change requires realigning incentives and making supportive organizational changes, and it must be pushed by determined leaders.

Failing to understand the relationships among the vectors of change. Dealing with this obstacle may be an important new frontier—not only for forecasters but also for financial and organizational leaders and strategists.

The bottom line in healthcare innovation is that as health care changes, forecasting approaches have to change.

Market forecasts, total-cost-of-care forecasts, financial cost models, and population health models all have to be adjusted to the trends in health care. Those of us in the forecasting business need new models for effectively dealing with each of these major forces of change, and for understanding how they interact with each other.

Steps to an Effective Forecasting Approach

A productive forecasting process should include the following four steps:

- Set a reasonable bar for precision. Allow for an error term, while forecasting approaches catch-up to behavior.

- Monitor the accuracy of forecasts predictions over time. Separate out and track the causes of errors.

- Involve more than one perspective during the forecasting process (e.g., data analyst, market analyst, technology/AI observer, caregiver, organizational analyst, sociologist).

- Estimate and understand the effect of each major force (vector) on a forecast, and then attempt to estimate the combined effect of all vectors.

The good news is accuracy in forecasting need not be a competitive sport. We can learn from each other how to effectively deal with obstacles. Everyone can benefit from more accurate forecasts.

Footnotes

a. See for example: HIMMS, 2019 Healthcare Trends Forecast: The Beginning of a Consumer-Driven Reformation, 2019.

b. Cohen, A.B., and Safavi, K., “The Oversell and Undersell of Digital Health,” Health Affairs, Feb. 27, 2019.

c. Vlanos, J., “Amazon Alexa and the Search for One Perfect Answer,” Wired, Feb. 18, 2019.