Innovation and Disruption

Healthcare venture investing: How to succeed in a white-hot market

Published

December 3, 2021

2:27 pm

|

Updated

November 16, 2022

5:53 pm

While the world suffered through the COVID-19 pandemic, the U.S. healthcare venture market exploded in 2020 and the first half of 2021. A growing number of healthcare corporate venture investors expanded their activities apace to realize financial opportunities, support their corporate strategies and spur innovation throughout their organizations.

As a follow-up to our previous surveys of venture investors in health systems and other healthcare companies, we conducted a third survey this year to understand the forces driving today’s rapidly expanding market for healthcare venture investments and its impact on corporate investing strategies.

Key findings of our research are described here. (For lists of survey respondents and health system and other strategic venture investors, see appendixes A, B, and C at the end of this article.)

Trend details and drivers

From 2019 to 2020, according to Silicon Valley Bank, U.S. healthcare venture capital fundraising for healthcare companies grew 57% to almost $7 billion, U.S. venture investments grew 55% to $44 billion, and global exit values, including both IPOs and private M&A transactions, grew 54% to over $140 billion. Both the number and size of funds grew substantially, fueled by the success of healthcare ventures in the public market. According to Silicon Valley Bank, post-IPO performance of new healthcare companies in 2020 was +104% for 2018 ventures, +98% for 2019 ventures and +85% for ventures launched in 2020.

At the top end, large private capital funds, hedge funds and leveraged buyout (LBO) companies are aggressively penetrating healthcare venture financing, especially in C and later financing rounds. A prime example is Tiger Global, a New York-based private-capital powerhouse, which raised $3.75B for its 12th venture fund in 2020 and $6.65B for its 13th fund in the first quarter of 2021. Tiger Global has grown into a major player in healthcare and life sciences investing. After participating in only five healthcare deals in 2019, the company participated in eight deals worth a little more than $1 billion in 2020 and was lead investor in three high-profile financings (Oscar Health, Olive and Spring Health). In the first seven months of 2021, Tiger Global participated in 22 healthcare deals worth almost $3 billion and was lead investor in 13 of them. Sixteen of these were C or later rounds, with an average financing value of $175 million.a

The emergence of large players like Tiger Global, Andreessen Horowitz, Clayton, Dubilier & Rice and Sequoia Capital in healthcare has created more exit channels for founders and early-stage investors. IPOs continue to be an important exit route across all segments, but increased availability of private capital has made private M&A deals more competitive with IPOs. Traditional strategic acquirers like pharma companies, which generally avoided competing with IPOs, are being forced to acquire biopharma ventures earlier at higher valuations in private deals in order to preempt these financial investors.

In addition to IPOs and private capital transactions, special purpose acquisition companies (SPACs) are emerging as another important exit path for healthcare ventures. Although SPACS can be risky, they accounted for almost half the digital health IPOs in the first half of 2021, and Rock Health expects them to make up most if not all the digital health IPOs for the remainder of the year.

Increased focus on digital health

These trends are increasing valuations of healthcare ventures significantly, as was especially evident in digital health in the first half of 2021. Digital health is not the largest healthcare segment — biopharma is substantially larger. But digital health quickly became the fastest-growing segment, growing 90% from 2019 to 2020 to $14.68 billion, and then adding another $14.78 billion in just the first half of 2021, according to Rock Health.

The pandemic was a major catalyst for this growth. As one survey respondent said, the pandemic advanced the telehealth market by a decade by fostering patient acceptance and convincing clinicians that virtual care can be effective. In addition to stimulating the development of new digital technologies, the pandemic:

- Accelerated the shift of care into the home, enabled by advancements in virtual care and remote monitoring

- Increased adoption of tech-enabled solutions, like the vaunted “digital front door”

- Increased collaboration between operations and investment professionals in health systems

- Prompted many health systems to expand their value-based “risk” contracting, which proved less risky than their fee-for-service business during the pandemic

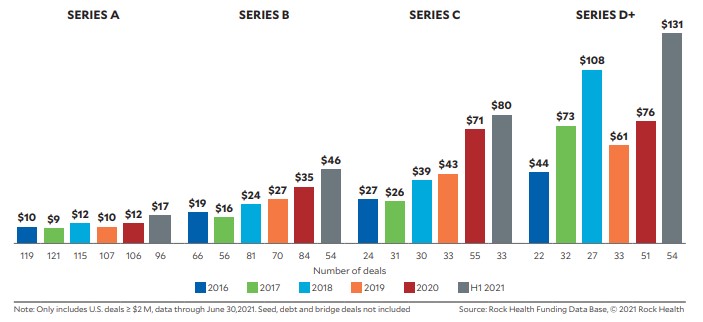

Driven by these disruptive trends, capital for digital health ventures is flooding down from later to earlier stages of investment and increasing valuations across the board. The exhibit below, from Rock Health, shows this trend clearly.

Average size of digital health funding, by year and series, 2016-1H21

Digital health investments in series D and later rounds have soared, but the average size of A, B, and C rounds has also increased, with A series financings having increased more than 40% in the first half of 2021.

These valuation trends suggest we may be approaching a situation similar to the late “dot-com” era. One experienced investor believes that high valuations are allowing ventures with subpar performance to last longer than they should, and that some portfolios are getting “long in the tooth” and unlikely to yield good returns. Another investor mentioned “zombie portfolios” full of “walking dead” companies.

Not everyone agrees, however. Two investors – one strategic and one financial – think higher prices in A and B rounds are justified because digital health companies are more mature, with more serial entrepreneurs than in the past.

And Nickolas Mark, managing director and partner of Intermountain Ventures in Salt Lake City, said, “More dollars flowing into digital health equates to more innovation, which is good for each of us individually, as well as the communities we serve.”

Need for new strategies

Increases in valuations are forcing investors to adopt new strategies, and respondents identified several changes they were making to adapt. Pete Tedesco, a managing partner at Health Enterprise Partners in New York, said his firm was doubling down on areas where they have intense convictions: “When you know you’re going to have to pay a market-clearing price, you need to stick to your strategy and add value.” Another investor said that high valuations had pushed his fund into earlier-stage investments to avoid over-paying.

Increased competition is also affecting investor strategies. More firms are establishing healthcare platforms and hiring experienced investors to build healthcare portfolios. Many firms – even early-stage angel investors – are specializing in certain healthcare segments (e.g., digital health). Other investors are merging to create larger firms that can compete with private capital and LBO players for later round financings (e.g., the merger of Cambia and Mosaic to form Echo Health Ventures). And underlying all these strategic moves is the imperative for diversification, which drives collaboration among venture investors. There is probably no industry where “coopetition” is more pervasive today than healthcare venture investing.

As prices and competition heat up, risks grow. Although in our 2018 report we heralded the opportunities of venture investing by health systems, we are now raising the yellow caution flag. In addition to the specter of the Federal Reserve tightening the money supply to stave off inflation, there is too much capital chasing too few smart deals, according to Scott Powder, president of Advocate Aurora Enterprises in northern Illinois. “Unless you have already built a strong venture infrastructure, the risk of direct investment may be too great,” Powder said.

Key survey findings: Rising numbers and shifting priorities

The number of health systems with venture investing programs grew from 69 in our 2018 survey to more than100 in this year’s survey, and we identified more than 40 other healthcare corporations with active healthcare corporate venture investing programs, as shown in Appendix A, below. About half these investors have defined investment funds; the remainder invest off their balance sheets.

In addition to the growing number of strategic players and growing size of funds, respondents noted they are making more investments, with a larger average size of deals, and have had more exits in 2020 and 2021. Reflecting this growth, one experienced investor reported their fund governing boards shifted from quarterly calls to calls every six weeks to keep pace with the increased deal flow.

Several strategic investors also noted that growth of the healthcare venture market has made ventures more central to their corporate strategies. New companies and partnerships are becoming meaningful businesses for health systems, and for this reason they are commanding more C-suite attention than in the past. As one experienced venture manager put it, “Our company is increasingly aware, asking more questions, and taking them more seriously.”

In our sample, we identified five distinct types of strategic venture investors, as detailed in the sidebar that immediaatley follows this article.

Key success factors in 2021

Given the white-hot market for healthcare ventures, key behavioral success factors have inevitably changed from three years ago. Our findings pointed to four critical success factors that should guide strategic investors today.

1. Be clear about strategic goals. The starting point for any investment strategy is deciding what you want to accomplish. Strategic goals articulated in our interviews included the following:

- Learning about new technologies to provide a window on trends. Scott Powder of Advocate Aurora Enterprises emphasized investing in strategically aligned venture capital funds rather than direct company investments because, in his view, “You don’t have to invest capital directly in early-stage companies to get this knowledge.” But as long as you keep investments small, this may be a reasonable approach.

- xperimenting with others’ solutions and scaling those that work in your organization. Roberta Schwartz, chief innovation officer of Houston Methodist, experiments with new technologies and scales them across the organization with minimal investment.

- isrupting / shaking up your existing business model? Aaron Martin, managing general partner of Providence Ventures (PV), described disruption as a major strategic goal of his company.

- Starting a new business line. Advocate Aurora Enterprises is an example of a company that has pursued this strategy.

- Promoting diversity, health equity & inclusion This strategy reflects an explicit investment goal of CommonSpirit Health.

Given the steep prices of ventures in today’s market, and the opportunity cost of investment professionals’ time, being clear about your strategic goals is a critical success factor, as Pete Tedesco of Health Enterprise Partners observed.

2. Design and implement an investing strategy to meet goals. When designing such a strategy, organizations should address the following key questions:

- What is our preferred scale for venture investing? Standing up a $100 million venture fund in a highly competitive market requires a significant investment in expensive talent and other resources to support the strategy. And planning for additional capital calls will be needed; several respondents stressed the need to stick with ventures over the long run.

- What stage of development do we want to emphasize? The range of options includes startups, early–stage companies, A rounds, B rounds and C+ rounds. In our study, we found that strategic investors were more inclined than financial investors to invest at earlier stages. (Not-for-profit health systems’ ability to participate in more expensive later rounds may be limited by access to capital.)

- How do we choose content areas to pursue? Almost all investors interviewed emphasized the importance of limiting the areas for investing, but different funds do this in different ways. KP Ventures starts every year with a set of themes that is informed by clinical operations, according to Sam Brasch, senior managing director, and every two years they conduct a more formal proactive needs assessment. PV writes a set of area-specific white papers that stack rank investment priorities. (Last year, PV produced 14 white papers. We discussed PV’s approach to prioritizing investments in our 2018 paper.)

Intermountain Ventures (IV) has a straightforward approach for setting investment priorities – a three-step inside-out process, according to Nickolas Mark, IV’s managing director and partner:

- The IV team engages across Intermountain Healthcare to better understand collective goals and pain points.

- The team pairs this analysis with research around trends and emerging technologies.

- The team synthesizes the findings into “zones of opportunity,” such as digital therapeutics or virtualizing clinical trials, which are then updated periodically.

Cedars-Sinai has developed a methodology for identifying content areas similar to PV’s approach, as discussed in our 2018 paper. According to Darren Dworkin, managing director of CS Ventures, the venture team starts the year by asking, “What problems do we need to solve?” They then analyze their own operations, and if they’re already solving the problem internally, they pass. Next, they analyze the venture world, and if someone else is solving the problem, they pass. Finally, they assess whether the venture they’re considering investing in is a game-changer, or whether it’s just bells and whistles. If it’s bells and whistles, they pass.

Given these different investment strategies and the frothy market, it is not surprising that survey respondents identified a variety of content areas where they are focusing current investments. The following exhibit highlights some of these areas.

Priority areas of focus for venture investing in healthcare

| Investment areas | Venture investing firms interested in investment area | Examples of innovation leaders |

| Digital health | Providence Ventures, McKesson Ventures, Ascension Ventures, OSF Ventures | Amwell, DexCare, Evidation Health, Hippo Health |

| Integrated physicial/virtual health | Innovation Institute, Common Spirit Health, McKesson Ventures | Wildflower Health, Tia Clinic, One Medical |

| Consumer health and wellness | Common Spirit Health, OSF Ventures | Accolade, Twistle [acquired by Health Catalyst] |

| Mental/behavioral health | Providence Ventures, McKesson Ventures, Innovation Institute, OSF Ventures | Headspace Health (merger of Headspace and Ginger), Column Health |

| Migration of care out of hospitals | Providence Ventures, Intermountain Health, Ascension Ventures | |

| Ambulatory surgery | Common Spirit Health, McKesson Ventures | Envision Healthcare [acquired by KKR] |

| Hospital at home | KP Venture, Mayo Clinic, Intermountain Health, OSF Ventures, McKesson Ventures | Medically Home, Contessa Health [acquired by Amedisys, Inc.] |

| Virtual care networks | OSF Ventures | Access Physicians, Aspen RxHealth |

| Lab at home | Common Spirit Health, Intermountain Health, McKesson Ventures | EverlyWell, 23andMe |

| Helping providers transition to risk (e.g., value-based care models) | Providence Ventures, Common Spirit Health, Ascension Ventures | VillageMD [acquired by Walgreens Boots Alliance], Oak Street, Transcarent, Iora Health [acquired by One Medical] |

| Clinical and commercial services | McKesson Ventures | |

| Cybersecurity | KP Ventures, Cedars-Sinai, Common Spirit Health | Censinet, Ordr, Netskope |

| Specialty pharmacy | Common Spirit Health, Mass General Brigham Health, OSF Ventures | Pharmapacks, Shields Health Solutions |

| Biopharma services | McKesson Ventures | OncoHealth |

| Revenue cycle | Ascension Ventures, OSF Ventures, Innovation Institute | R1 RCM |

| Monetizing best practices | Innovation Institute | Rising Nurse Leaders Program |

| Diversifying revenue and profit sources | Advocate Aurora Health, Ascension Ventures | Advocate Aurora Enterprises |

| Decentralized clinical trials | McKesson Ventures, Ascension Ventures | Lightship, Science 37 |

| Social determinants of health | Common Spirit Health, Innovation Institute, Ascension Ventures, OSF Ventures, McKesson Ventures | Unite Us, Nightingale Health |

Although many of these content areas overlap, some are distinct, and perhaps unexpected. COVID-19, for example, disrupted traditional clinical trials, creating a market for decentralized trials that several new ventures are now targeting.

Regardless of content area, investment decisions in this competitive market must be underpinned with sound due diligence. Managers should be aware of where their ventures stack up in the market. As one investor said, “If the venture isn’t going to get a bronze medal at least, we’re not interested.”

3. Syndicate and collaborate. Co-investing with other financial and strategic investors has always been popular, but syndication has become even more pervasive as the market has heated up. One financial investor said that in the past, 30% to 40% of their deals were syndicated, but in the past two years, the percentage has risen to over 50%. One rationale for syndication is simple diversification: Investing $1 million in 10 deals is less risky that investing $10 million one deal. Another rationale is to leverage complementary skill sets. Strategic investors partner with financial investors for their market understanding and financial skills. Financial investors partner with strategic investors as lead users who can validate value propositions, conduct pilots and scale ventures. Solution-finders are particularly active participants in syndications and partnerships with other investors. For a strategic investor, syndication provides assurance that they aren’t “just eating our own cooking.” (See the sidebar below for details on these different investor types.)

In the past, health systems were rarely lead investors, unless they were commercializing their own inventions. This may be changing, however. Martin of PV said the company is starting to lead more syndications, and it recently spun off Dexcare on its own, partnering with a financial lead.

4. Differentiate and integrate investing activities and operations. Venture investing and operating a healthcare enterprise are distinct businesses. Venture investing is externally focused, while managing operations is internally focused. The businesses typically operate on different timeframes. There are also potential conflicts of interest, as when operating managers pressure venture investors to invest in pet projects that are unlikely to be accretive or when venture investors pressure operating managers to implement ventures that don’t fit their needs. One financial investor observed that strategic investors can unduly constrain ventures by imposing unrealistic requirements and stretching out timelines.

Achieving symbiosis between these two businesses requires carefully designed structures and processes that differentiate them but also integrate them at just the right points. Differentiation is typically achieved by creating separate venture organizations (e.g., KP Ventures), recruiting investment professionals to staff them, defining fixed capital commitments (venture funds), setting investment goals, and developing agreed-on funding rules.

At the same time, symbiosis requires integration between investing and operations. Venture managers must develop a deep understanding of operational needs, and operating managers need to learn what venture funds are investing in and how they can help make them successful. From a timing standpoint, venture managers need to decide where they should be ahead of their systems, and where they should be in lockstep.

Effective integration is achieved through management structures and processes like the following:

- Investment committees comprised of senior operating managers

- “Boards” of funded businesses that integrate venture professionals and operating managers and provide sponsorship and “air cover” for the ventures

- Disciplined venture development processes with rapid development timelines and performance goals

- Regular reviews of venture performance, including reviewing progress in scaling ventures inside the company

KP Ventures, for example, has an oversight committee that includes KP’s executive vice president of health plan operations, its chief information and technology officer, and its national vice president for business development and innovation.

Cedars-Sinai has a similar structure called the “Selection Committee” that whittles down a list of 50 to 60 venture candidates to 10 potential investments. These are the types of structures needed to integrate investing and operating activities effectively.

Be optimistic, but be careful

Opportunities for venture investing are still significant, and healthcare companies with established venture operations and a track record of success should continue to do well. Companies considering getting into the game, however, should exercise caution. In addition to normal business risks, many ventures today are being propped up by low-cost capital that obscures problematic fundamentals. Although profitable exits have grown, they still lag invested capital. Healthcare companies whose leaders feel they want to get started in venture investing should consider lower-risk strategies than capitalizing $100 million venture funds, such as making smaller investments with syndicates of other investors.

In a crowded market, it is also important to stay focused. Most venture funds employ a handful of investment professionals (perhaps three to 10) to manage a portfolio of 10 to 25 investments. It is easy to underestimate the amount of effort required to evaluate, invest in and manage new ventures to successful exits. And experienced investment talent isn’t cheap: Corporate venture organizations must structure their compensation to compete with independent venture firms.

Finally, health systems and insurers should also take a lesson from Houston Methodist’s innovative user strategy, described in the sidebar below. Over the past few years, the market has spawned thousands of healthcare ventures, and many have the potential to create value for patients and/or providers if implemented effectively. In today’s environment, implementation is often the critical success factor. A proactive strategy that searches for and experiments with new ventures that are already in the market may pay off better with less risk than launching a dozen more.

Footnote

a. The authors conducted this analysis using www.crunchbase.com as a principal data source.

Types of strategic venture investors identified

Although all the strategic investors we interviewed are trying to develop “unicorns” with capitalizations of $1 billion and more, market growth and increasing competition are causing investment strategies to diverge. We identified five different types of strategic venture investors in our survey.

1. Traditional health system strategic investors

Traditional strategic investors, whose goals are producing excellent financial returns and delivering strategic value to the health systems that own them, have experienced excellent returns on their portfolios over the past few years and are growing in line with the white-hot market. Examples of such investors are Providence Ventures (PV), KP Ventures and Ascension Ventures (AV).

Matt Hermann, senior managing director of AV, described AV’s goals as follows:

- Deliver excellent financial returns (on par with independent venture firms)

- Be a good partner to portfolio companies and co-investors

- Create strategic value for Ascension Health

AV closed a new $285M fund in March, their fifth, bringing total assets under management to over $1 billion. According to Hermann, each fund has experienced double digit returns, and each new fund has performed better than its predecessors.

Aaron Martin, managing general partner of PV, another traditional strategic investor, said his firm more than doubled the value of its portfolio in Fund I, far exceeding returns available from alternative investments, and this fund’s value is trending higher as companies continue to exit.

2. Commercializers

Commercializers, which focus primarily on commercializing inventions developed by their own researchers and clinicians, are also having success, although their growth is slower, since it is constrained by the supply of internal innovations. Examples include the Cleveland Clinic, Mayo Clinic, Mass General Brigham and Johns Hopkins Medicine. These health systems typically maintain majority ownership of their ventures at early stages, but they often syndicate them with other investors at some point to enhance their chances of success and “avoid drinking our own Kool-Aid,” in the words of Akhil Saklecha, an emergency physician and managing director of Cleveland Clinic Ventures (CCV).

Like most other commercializers, CCV has no defined investment fund; every investment must be justified to Cleveland Clinic leadership as a worthy commitment of operating capital. One potential problem with this funding model is that ventures may have trouble getting capital for follow-on development after they have burned through initial commitments. Saklecha, however, emphasized that CCV is committed to supporting its startups from initial involvement through exit, including what he called developmental and financial “valleys of death.”

3. Financially oriented investors

Financially oriented strategic investors such as McKesson Ventures (MV) and many of the health insurer and pharmaceutical venture organizations, while strategically focused on healthcare, act more like independent venture capital firms and are experiencing similar success.

Michelle Snyder, a partner in MV, which specializes in digital health and healthcare information technology and services, described the firm’s primary goal as being focused on realizing a strong ROI. MV looks for companies that have product-market fit and material revenues and are at an inflection point where their growth is beginning to accelerate. MV is also expected to be what Snyder characterized as strategic radar for McKesson to help the company anticipate disruptions that could affect its business. MV is seven years old, has already made over 40 investments and is committed to continue growing its portfolio.

Snyder echoed Saklecha in emphasizing the importance of sustaining financial commitments over the long haul. “You need staying power to be successful in this business,” she said.

4. Solution finders

Solution finders that anchor their investments in business problems and opportunities they experience in their operations are also growing. OSF Ventures, Intermountain Ventures Fund (IV), and CommonSpirit Health are all examples of solution finders. These companies rarely invest in ventures their parent companies don’t use or expect to use in the very near future.

Stan Lynall, vice president of venture investments at OSF Healthcare, described its strategy as follows:

Our investment strategy has always prioritized strategic focus over financial focus. We only invest in technologies that can support our strategy and are endorsed by subject matter experts in our organization. While we don’t require an existing vendor relationship when we invest, we need assurance it can be employed by us in the future to either improve patient outcomes or reduce operating costs.

The main rationale for solution finders is comparative advantage: As Rich Roth, chief strategic innovation officer at CommonSpirit Health, explained, health systems are large potential customers for new technologies and can scale innovations quickly across many operating units. He believes this gives his investments a competitive advantage relative to investments made by independent venture firms.

5. Hybrid models

Many large health systems have adopted a multifaceted approach to managing ventures and innovation, including the Innovation Institute and Cedars-Sinai. Our 2018 paper highlighted the Innovation Institute, which includes an incubator (Innovation Lab), a $100M venture fund co-managed by Long River Ventures, and a portfolio of service companies that provides cash flow to fund these venture investments. Since we last profiled the Innovation Institute, its ownership has evolved, with two owners merging (Bon Secours and Mercy Health), a couple of new owners joining (MultiCare and Valley Children’s Healthcare), and Providence St. Joseph Health converting from an owner to a new subscription model developed by the Institute. The Innovation Institute’s basic multi-tiered hybrid model, however, has remained the same, and the Institute has had a couple of impactful exits in the past couple of years.

Cedars-Sinai has a simpler structure than the Innovation Institute, with a strategic fund and a tech transfer division. Like the solution finders, Cedars-Sinai only invests in ventures the health system will put to extensive use, according to Darren Dworkin, managing director of CS Ventures.a Like the commercializers, Cedars-Sinai also has an active tech transfer division aimed at commercializing technologies developed internally, primarily in diagnostics, therapeutics and devices.

Other strategies

In addition to these five types of healthcare corporate strategic investors, we also identified two related strategies that aren’t, strictly speaking, venture investing strategies. One of these, new business development, is exemplified by Advocate Aurora Enterprises (AAE) in Illinois, while the other, innovative users, is exemplified by Houston Methodist in Texas.

AAE

Scott Powder, president of AAE, began our interview by emphasizing that the entity “is not a corporate venture arm.” It is, instead, a new business capitalized by Advocate Aurora Health to help it diversify beyond its traditional healthcare delivery business.

AAE was formed in December 2020, and Powder stepped down as chief strategy officer of Advocate Aurora Health to take the reins as AAE’s president in April. AAE is a business-to-business and business-to-consumer company that participates in the growing consumer health and wellness ecosystem. Its vision is to become a national leader in consumer health and wellness, thereby contributing to Advocate Aurora Health’s goal of helping people live well and diversify the company beyond its core in healthcare delivery.

AAE is investing in three sectors:

- Aging independently

- Parenthood

- Personal performance through integration of mind, body and nutrition

AAE has made two major investments so far:

- The acquisition of Senior Helpers, a provider of in-home personal care

- An investment in FoodSmart, a telenutrition platform

In addition to positively impacting the health of its customers, Powder’s long-term financial goals are to become an accretive operating company that broadens its parent’s product offerings and diversifies it beyond healthcare delivery. In contrast to solution finders, AAE does not expect to sell much to health systems, which Powder said is “almost as challenging as selling to the Department of Defense.”

Houston Methodist

Another strategy we simply call innovative users, is exemplified by Houston Methodist. Rather than investing its own capital, innovative users believe there are enough startups available in the market today that innovation is better achieved by partnering with existing companies rather than funding new ones. Innovative users pay close attention to healthcare ventures developed by others and move quickly to test them out to see whether they can add value to their system, and scale them internally if they do.

Roberta Schwartz, Houston Methodist’s chief innovation officer, sees her job as disrupting and transforming every area of the health system in ways that improve the patient experience. She has a long list of venture-backed companies the health system is experimenting with that disrupt existing clinical and business processes, including CareSense, MIC Sickbay, Well Health, Syllable, Intelligent Locations, Caregility, Blockit and many others.

To accelerate the process of trying out new solutions, Schwartz formed a broad-based committee she calls the “digital innovation obsessed people (DIOP)” to oversee the evaluation and adoption process for new technology ventures. Each venture is assigned an operational champion and moves through four defined stages:

- Graduate

- Pilot

- Pipeline

- Scaling or RIP

Champions know that if they don’t make ROI within a year, their venture will end up “resting in peace.”

Schwartz believes Houston Methodist is much better at helping companies scale their products (“B stage”) than at starting them up (“A stage”). As innovator-in-chief, she is in frequent contact with sophisticated investors and peers around the country identifying innovations that could potentially be useful to Houston Methodist, planning and evaluating pilot implementations and scaling up those that add value.

Schwartz has essentially created a massively parallel innovation process that minimizes upfront investment and ensures a rich portfolio of disruptive new solutions that add real value to the health system.

Footnote

a. Since our interview, Dworkin moved to Press Ganey, where he is now chief strategy officer and managing partner, PG Ventures.

Appendix A: 2021 survey respondents

|

Company |

Interviewee |

Title |

|

Advocate Aurora Enterprises |

Scott Powder |

President |

|

Ascension Ventures |

Matt Hermann |

Senior Managing Director |

|

Cedars-Sinai |

Darren Dworkin |

Managing Director, CS Ventures |

|

Cleveland Clinic |

Akhil Saklecha, MD |

Managing Director, Cleveland Clinic Ventures |

|

CommonSpirit Health |

Rich Roth |

Chief Strategic Innovation Officer |

|

Health Enterprise Partners |

Pete Tedesco |

Managing Partner |

|

Houston Methodist |

Roberta Schwartz |

Chief Innovation Officer |

|

Illinois Ventures |

Nancy Harvey |

Senior Director, Principal |

|

Innovation Institute |

Joe Randolph |

Chief Executive Officer |

|

Larry Stofko |

EVP, Innovation Lab | |

|

Intermountain Ventures |

Nickolas Mark |

Managing Director & Partner |

|

KP Ventures |

Sam Brasch |

Senior Managing Director |

|

Longitude Capital |

Marc Galletti |

Managing Director |

|

McKesson Ventures |

Michelle Snyder |

Partner, McKesson Ventures |

|

OSF Ventures |

Stan Lynall |

Vice President of Venture Investments |

|

Providence Ventures |

Aaron Martin |

Managing General Partner, Providence Ventures |

|

Jeff Stolte |

Senior Partner, Providence Ventures | |

|

Silicon Valley Bank |

Chris Moniz |

Director, Life Science & Healthcare Practice |

|

Jon Norris |

Managing Director |

Appendix B: Health system strategic venture investors

|

Health System |

Venture Arm |

Other Known Investor Relationships |

|

AdventHealth |

Ascension Ventures, Heritage Group | |

|

Advocate Aurora Health |

Corporate Ventures & Innovation |

HIMSS Healthbox, StartUp Health, Heritage, Flare Capital Partners, Greenspring Associates, Maverick Capital |

|

Allina Health |

HEP, AVIA | |

|

Arkansas Children’s |

AVIA | |

|

Ascension Health |

Ascension Ventures |

HIMSS Healthbox, StartUp Health |

|

Ascension St. Vincent Kokomo |

HIMSS Healthbox | |

|

Avera Health |

Innovation Institute | |

|

Banner Health |

Heritage Group | |

|

BayCare |

AVIA | |

|

Baylor Scott & White Health |

HIMSS Healthbox | |

|

BJC Healthcare |

AVIA | |

|

Beacon Health System (IN) |

AVIA | |

|

Bellin Health (WI) |

AVIA | |

|

Bon Secours Mercy Health |

Ascension Ventures, AVIA, Innovation Institute | |

|

Boston Children’s Hospital |

Rock Health | |

|

Boston Medical Center |

AVIA | |

|

Carle Foundation |

|

Ascension Ventures |

|

Catholic Health East |

Ascension Ventures | |

|

Cedars-Sinai |

AVIA | |

|

CentraCare |

|

Ascension Ventures |

|

CHI |

Ascension Ventures | |

|

Children’s Health (Dallas) |

|

Ascension Ventures |

|

Children’s Health Orange County |

Innovation Institute | |

|

Children’s Hospital Colorado |

AVIA | |

|

Children’s Mercy Kansas City |

AVIA | |

|

Children’s Minnesota |

AVIA | |

|

Christiana Care Health System |

AVIA | |

|

CHS |

Heritage Group | |

|

Cincinnati Children’s Hospital Medical Center | ||

|

Cleveland Clinic |

Cleveland Clinic Ventures |

Flare Capital Partners, HEP |

|

CommonSpirit Health |

| |

|

Edward-Elmhurst Health |

HIMSS Healthbox, AVIA | |

|

Franciscan Missionaries of Our Lady HS (LA) |

Innovation Institute | |

|

Frederick Health (MD) |

AVIA | |

|

Froedtert & MCW |

AVIA | |

|

Geisinger |

AVIA | |

|

HCA |

HIMSS Healthbox, Health Insight Capital | |

|

Henry Ford Health System |

Henry Ford Innovations |

Heritage Group, AVIA |

|

Henry Mayo Newhall Hospital |

HIMSS Healthbox | |

|

Honor Health (AZ) |

AVIA | |

|

Health System |

Venture Arm |

Other Known Investor Relationships |

|

Houston Methodist |

AVIA | |

|

Imperial College Health Partners (UK) |

AVIA | |

|

Inova Health System | ||

|

Integris Health |

Heritage Group, AVIA | |

|

Intermountain Healthcare |

Intermountain Ventures |

Ascension Ventures, Rock Health, Heritage Group, HEP |

|

IU Health |

CHV Capital | |

|

Jefferson Health |

Jefferson Innovation |

AVIA |

|

Johns Hopkins Medicine |

Johns Hopkins Technology Ventures | |

|

Kaiser Permanente |

KP Ventures |

KP Ventures, Rock Health, StartUp Health |

|

Kettering Health Network |

HEP | |

|

Lee Health |

AVIA | |

|

LifeBridge Health |

AVIA | |

|

LifePoint Health |

Heritage Group | |

|

Luminis Health |

|

Ascension Ventures |

|

MD Anderson |

Strategic Industry Ventures, AVIA | |

|

Main Line Health |

AVIA | |

|

Mass General Brigham |

Mass General Brigham Ventures |

AVIA |

|

Mayo Clinic |

Mayo Clinic Ventures |

StartUp Health |

|

Memorial Hermann HS |

Heritage Group, AVIA | |

|

MemorialCare Health System |

MemorialCare Fund |

HEP, AVIA |

|

MercyOne (IA) |

AVIA | |

|

Miami Children’s Health System | ||

|

Montage Health |

HEP | |

|

Mount Sinai (NYC) |

Mount Sinai Ambulatory Ventures | |

|

MultiCare (WA) |

Innovation Institute, AVIA | |

|

Navicent Health |

AVIA | |

|

NewYork-Presbyterian |

NYP Ventures | |

|

Northeast Georgia Health System |

AVIA | |

|

NorthShore Univ Health System |

|

Ascension Ventures |

|

Northwell Health |

Northwell Ventures | |

|

Northwestern Medicine |

Heritage Group | |

|

Novant Health |

|

Ascension Ventures |

|

Ochsner Lafayette General MC |

|

AVIA |

|

OhioHealth |

|

Ascension Ventures |

|

Orlando Health |

Orlando Health Ventures |

HIMSS HealthBox |

|

OSF Healthcare |

OSF Ventures |

Ascension Ventures, LRV Health, AVIA |

|

Palmetto Health |

AVIA | |

|

Penn Medicine | ||

|

Piedmont Healthcare |

AVIA | |

|

Presbyterian |

AVIA | |

|

Prisma Health |

AVIA | |

|

Health System |

Venture Arm |

Other Known Investor Relationships |

|

Providence St. Joseph Health |

Providence Ventures |

Innovation Institute, AVIA |

|

Ridgeview MC (MN) |

HIMSS Healthbox | |

|

Rush Health |

HIMSS Healthbox, AVIA | |

|

Sanford Health |

HEP | |

|

Sentara |

HEP, AVIA | |

|

Shannon Medical Center |

HEP. AVIA | |

|

Silver Cross Hospital (IL) |

AVIA | |

|

Sinai Health System | ||

|

Spectrum Health |

Heritage Group | |

|

St. Luke’s University Health Network (PA) |

AVIA | |

|

St. Vincent |

HIMSS Healthbox | |

|

Stanford Hospital & Clinics | ||

|

Sutter Health |

Heritage Group, HEP, Rock Health | |

|

Tenet Health |

Heritage Group | |

|

Texas Medical Center |

TMC Venture Fund | |

|

Trinity Health |

Ascension Ventures, Heritage Group | |

|

UCLA |

HIMSS Healthbox | |

|

UNC |

Rex Health Ventures | |

|

UnityPoint Health (IA) |

UnityPoint Health Ventures |

Heritage Group |

|

University College London Hospital Trust (UCLH) |

HIMSS Healthbox | |

|

University Hospitals (OH) |

UH Ventures |

AVIA |

|

University of Chicago | ||

|

University of Kansas Health System |

AVIA | |

|

UPMC |

UPMC Enterprises |

Health Velocity Capital |

|

USC Keck School of Medicine |

HIMSS Healthbox | |

|

UVA Health System |

AVIA | |

|

Valley Children’s Healthcare |

Innovation Institute |

Appendix C: Other healthcare strategic investors

|

Other Healthcare Investors |

Venture Arm |

Other Known Investor Relationships |

|

Accenture |

Accenture Ventures |

Rock Health |

|

Aetna |

Aetna Ventures |

StartUp Health |

|

Amedisys |

Heritage Group | |

|

Astellas Pharma |

Astellas Venture Management |

Rock Health |

|

Anthem |

Anthem Corporate Venture Capital | |

|

AXA (France) |

Kamet Ventures | |

|

BCBS of Alabama |

Heritage Group | |

|

BCBS of Arkansas |

USAble Corporation |

Echo Innovation Alliance |

|

BCBS of Kansas City |

Cobalt Ventures | |

|

BCBS of Massachusetts |

HIMSS Healthbox | |

|

BCBS North Carolina |

Echo Innovation Alliance | |

|

BCBS of Tennessee |

Heritage Group, HIMSS Healthbox | |

|

BCBS Association |

Blue Venture Fund |

HIMSS Healthbox |

|

Blue Shield of California |

Seae Ventures | |

|

Boehringer Ingelheim |

Boehringer Ingelheim Venture Fund |

Rock Health |

|

BUPA (UK) |

HIMSS Healthbox | |

|

California HC Foundation |

Heritage Group, HIMSS Healthbox | |

|

Cambia Health Solutions | ||

|

Cardinal Health |

Cardinal Partners |

StartUp Health |

|

CareFirst BCBS (MD) |

Healthworx |

Rock Health |

|

Centene |

AVIA | |

|

Cerner |

Cerner Capital |

Heritage Group |

|

Cigna |

Cigna Ventures |

Heritage Group, StartUp Health, Health Velocity Capital |

|

Commonwealth Care Alliance |

Winter Street Ventures | |

|

CVS Health |

CVS Health Ventures |

Rock Health |

|

ExpressScripts |

HIMSS Healthbox | |

|

Florida Blue |

HIMSS Healthbox | |

|

Fujitsu BSC |

Fujitsu Ventures Fund |

Rock Health |

|

Genmab |

|

Rock Health |

|

Glaxo Smith Kline |

SR One Capital Management |

Rock Health |

|

GuideWell |

GuideWell Innovation |

HIMSS Healthbox, StartUp Health |

|

HCSC |

HCSC Ventures |

Heritage Group, HIMSS Healthbox |

|

Horizon BCBS |

Heritage Group | |

|

Humana |

Humana Ventures |

StartUp Health |

|

Labcorp |

Labcorp Venture Fund |

Rock Health |

|

McKesson |

McKesson Ventures |

Rock Health |

|

Novartis |

Novartis Venture Fund | |

|

Novo Nordisk Holdings (Denmark) |

Novo Ventures | |

|

Optum Healthcare |

Optum Ventures | |

|

Pfizer |

Pfizer Ventures |

Rock Health |

|

Ping An Insurance (China) |

Ping An Ventures |

StartUp Health |

|

Roche |

Roche Venture Fund |