Fast Finance

Concerns raised over copay-only plans

UnitedHealthcare reported rapid growth in copay-only plans in recent years among large employers.

Published

May 19, 2026

8:59 am

Fast-growing copay-only health plans can have adverse financial effects for health systems, an adviser warned.

Health system CFOs have told Mike Ruiz, senior director, financial transformation advisory services at Premier, that the requirements around the use of copay-only plans have left a growing number of patients with uncovered bills that are turning into bad debt.

“If the consumer doesn’t follow any of those [required steps] and the provider doesn’t keep track of them and sees them, then [providers] are ultimately stuck with that bill,” said Ruiz, “because the consumer gets it and they are supposed to pay it. But are they paying it? Chances are probably not. At least that’s what our CFOs are telling us.”

Copay-only plans, which also are known as variable copay plans, replace high deductibles and co-insurance with copays that vary by service. Critically, the copay-only provisions usually are offered only for in-network providers, and coverage for specific services can vary by facility.

Growing option

The plans are supported by some industry advisers to avoid the large patient costs under high-deductible health plans (HDHPs). That appeal to employers and enrollees has led to the proliferation of copay-only plans in employer-sponsored health insurance.

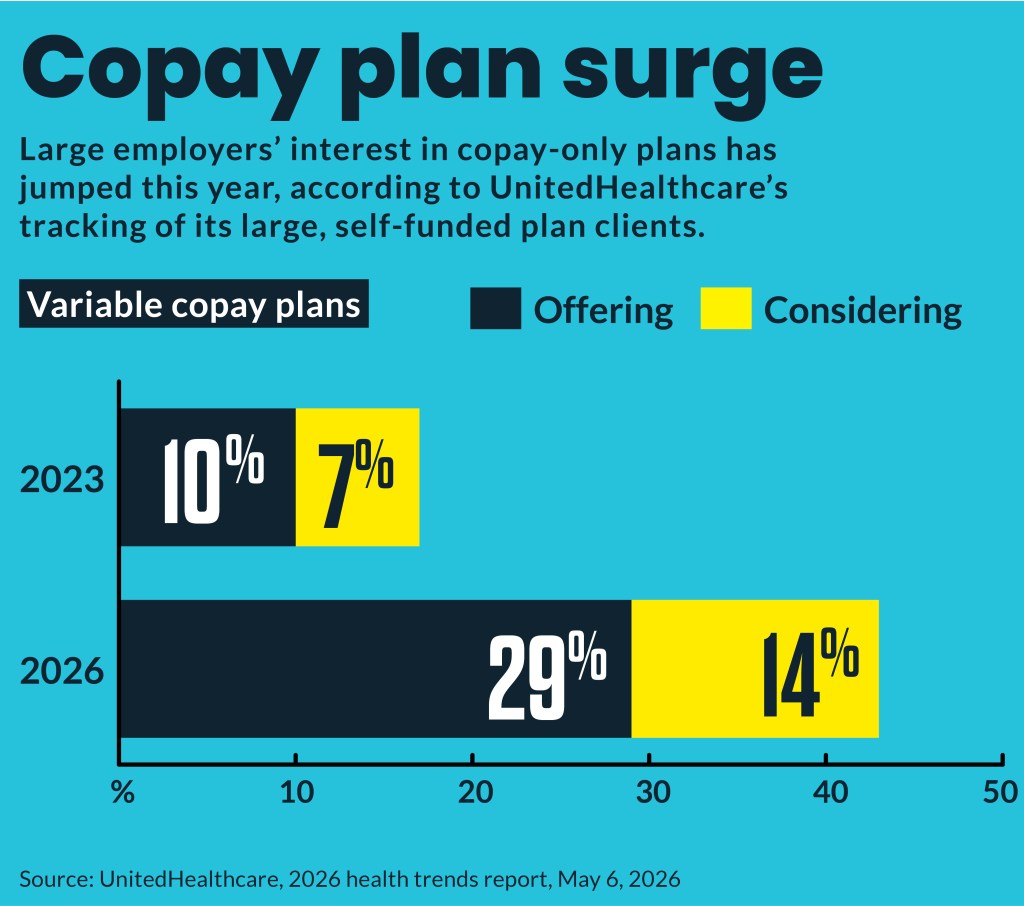

Fewer large employers are offering HDHPs, according to the recent UnitedHealthcare 2026 health trends report. Instead, the share of those companies offering variable copay plans — either as the only option or one choice — has increased from 10% in 2023 to 29% of large employers.

Another 14% are considering adding them within two years.

UnitedHealthcare’s Surest variable copay plan is the company’s fastest growing commercial plan, according to Alison Richards, CEO of Surest.

The growth in UnitedHealthcare’s plan is up from only 7% of employers using copay-only plans in 2024, according to a Mercer survey.

Similar variable copay plans include SimplePay from Aetna and Coupe Health from Blue Cross plans.

Variable copay plans have garnered so much interest because they have been able to control payer costs and steer patients toward the preferred providers, according to Jocelyn Herrington, vice president of strategic partnerships for the Advisory Board.

Employers increasingly are considering and adopting such alternative health plans to counter historic cost increases.

Collections required

Even if a provider is in network for a variable copay plan, each service can have widely varying copays based on varying payer quality scores. Collecting those copays, which sometimes involves substantial dollars, can prove a challenge.

“Anecdotally, what we’re hearing from CFOs, what we’re hearing from the revenue cycle folks is [that] it’s absolutely this inability to collect these copays that are increasing, and then they just go to collections. More often than not, you’re never seeing those dollars. So that’s growing,” Ruiz said.

In addition, the failure of plan enrollees to check on their payer app or by calling the payer in advance to ensure the provider and service qualify as a copay-only visit can result in coverage denials. The large resulting bills are sent to the patients. And when they cannot pay those bills, they become bad debt for health systems, Ruiz said, who previously worked for UnitedHealthcare.

Bad debt and charity care per calendar day have increased 45% year-to-date compared with that of year-to-date 2023, according to the latest Kaufman Hal hospital flash report, which uses data from Strata Decisions Technology. More recently, bad debt and charity care increased 17.0% year over year and increased 27% at Midwest hospitals, according to a separate Strata report.

Contracting effect

And bad debt hits from variable copay plans often are compounded by the discounts providers agree to give them when contracting with insurers — discounts that go beyond normal, self-insured large group discounts, said Ruiz.

“So, it’s a one-two punch, if you’re a CFO,” Ruiz said about the combined discount and bad debt financial hit on providers.

He urged finance leaders to undertake the necessary analysis of adverse financial effects of those plans on their organizations to provide quantified data to push back on them in payer negotiations.

Herrington agreed that variable copay plans create a lot of contracting complexity.

“Because you’re now not contracting as a health system with a particular payer, you’re not contracting as a particular specialty,” Herrington said in a December webinar. “You’re now contracting based on individual providers for individual services.”

Such plans are good for shoppable procedures in a competitive market, but they also require patients to go to different providers for different services.

“I don’t care which provider I go to; I only care about costs — I don’t know that patients make decisions that way and it fragments care,” Herrington said. “If those two health systems don’t have an [electronic health record] that talks to each other, the right hand and the left hand don’t know what is happening to that patient.”