Costing and Managerial Accounting

Why a more modern cost accounting approach in healthcare is needed post-COVID-19

Published

April 29, 2020

8:53 pm

|

Updated

December 13, 2022

5:08 pm

Sponsored by Strata Decision Technology

The ability to accurately measure costs of care and use this data to bend the healthcare cost curve is a vital factor for hospitals’ survival — now and in a post-COVID-19 world.

When it comes to understanding the total cost of care during COVID-19, the world has changed.

Today, many hospitals have canceled elective procedures to save resources for patients suffering from COVID-19 and others with urgent care needs. Meanwhile, the costs themselves are higher.

“The expenses for COVID-19 cases are going to be considerably higher than what your average case would be simply because of the need for supplies, the scarcity of supplies available and the need for additional resources to treat patients, including labor,” said Chad Mulvany, director of healthcare financial practices, perspectives and analysis for HFMA.

Even with a 20% increase in Medicare payment for COVID-19 discharges under the CARES Act passed by Congress, a Strata Decision Technology analysis projects an average loss of about $1,200 per case and up to $6,000 to $8,000 per case for some hospital systems, depending on their payer mix.

Meanwhile, researchers estimate that 90% of hospitals that cancel all elective procedures will soon begin to experience negative profit margins from COVID-19 cases.

Although the CARES Act provides $100 billion in funding for hospitals and other healthcare organizations responding to the coronavirus pandemic — which averages out to $108,000 per hospital bed, according to a Kaiser Family Foundation analysis — the degree to which a hospital can access those funds could come down to its ability to demonstrate COVID-19 costs of care.

As requests for funding are reviewed, those hospitals that can pull together cost data to justify the funds they are requesting will be ahead of the curve, Mulvany said.

More than ever, healthcare finance teams need to be nimble, facile and skilled in their use of cost data to model the impact of COVID-19 on their organization — now and in the months ahead — and make the right decisions for their future.

Top-of-mind cost concerns for healthcare leaders

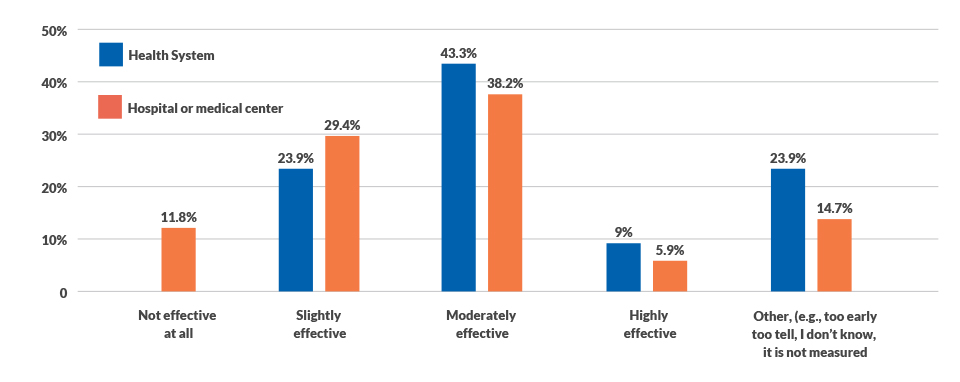

A recent survey by HFMA and Strata found that while 85% of health systems and 57% of hospitals and medical centers have a cost accounting system, most do not have strong proficiency in using cost data to reduce total cost of care.

Just under 44% of all organizations surveyed consider themselves “moderately effective” at getting clinicians and physicians to use cost data to reduce care costs, while only 7% considered their cost data effectiveness to be “highly effective.” Health systems rated their ability to engage clinicians and physicians around cost data slightly higher than hospitals (see the exhibit below for responses from these two large subsets of the respondents).

Effectiveness in using cost data, by organization type

How effective have your efforts been at getting clinicians and/or physicians to use cost data to identify and take advantage of opportunities to reduce the total cost of care?

Source: HFMA and Strata Decision Technology cost accounting survey, April 2019.

But if “moderate effectiveness” in using cost data raised concerns prior to the COVID-19 crisis, those concerns have intensified in the current environment, given the significant proportion of hospital resources required to test, triage and care for individuals during the pandemic.

Among healthcare leaders Strata has spoken with, many are wrestling with the following questions:

- How are other healthcare organizations defining “elective” cases?

- How are organizations measuring the current and projected impact of COVID-19 populations on their inpatient financials?

- What is the best way to model the deferral of elective surgeries and other cases that were previously included in our financial forecast or plan?

- How can we best incorporate the volume and revenue impact of COVID-19 cases into our forecast?

- What is the easiest way to reflect the additional expenses our organization faces related to labor, supplies and non-labor expense?

- What are the potential impacts to our balance sheet of our COVID-19 response?

- What is the updated guidance on financial modeling assumptions for healthcare organizations in 2020?

- How should we isolate COVID-19-related data for analysis and planning?

- Since my budget is no longer applicable, how can I most effectively update my targets and financial plan moving forward?

“These are tough questions, and our research suggests many healthcare organizations may not be able to quickly and easily answer them,” said Alina Henderson, senior director of professional services for Strata Decision Technology. “While most healthcare organizations interviewed last year planned to elevate their cost accounting capabilities by the end of 2022, the cost pressures these organizations now face demand that leaders adopt a more sophisticated approach sooner rather than later.”

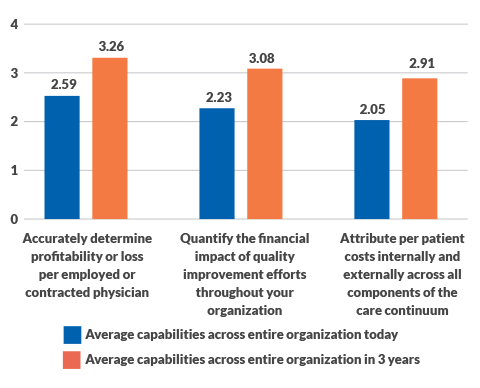

Cost accounting expertise is a rising priority — but will investment come soon enough?

Organizational costing capability today and in three years. (4 = Significant capability, 1 = No capability)

Source: HFMA and Strata Decision Technology cost accounting survey, April 2019.

A comparison of 2019 survey data with data from a 2011 survey shows many organizations’ efforts to adopt more advanced cost accounting capabilities were stuck in a holding pattern for nearly a decade — even in the face of increasing pressures to control healthcare costs.

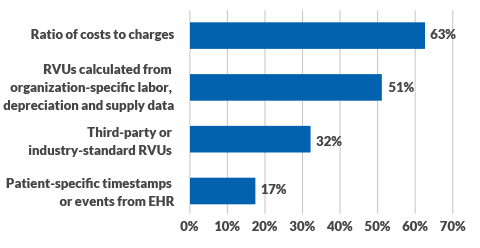

As a result, many healthcare organizations (63%) remain largely reliant on the traditional ratio-of-costs-to-charges (RCC) approach to calculate labor costs, according to the cost accounting survey (see the exhibit below). To calculate supply costs, 68% of respondents still use patient-specific acquisition costs for supplies, drugs and implants, while 52% also use the RCC method.

Methods used to calculate labor costs

Source: HFMA and Strata Decision Technology cost accounting survey, April 2019.

After the immediate challenges of COVID-19 have passed, the long-term financial challenges for healthcare organizations will be daunting.

“Hospitals will face dual pressures around cost containment and increased societal demands to maintain expensive standby capacity,” Mulvany says. “The only way to meet these demands is to become really efficient by understanding your cost to deliver care and making decisions based on cost data. The future will favor those organizations that have advanced cost-data capabilities and are adept at engaging key decision-makers around the ways in which care is delivered.”

In the new normal, cost accounting intelligence — across the entire enterprise — will be a strategic imperative for healthcare organizations.

“COVID-19 has created a mandate for healthcare leaders to move beyond ad hoc cost accounting functions to more advanced practices and platforms,” Henderson said. “Without timely, actionable data around total cost of care, healthcare leaders will have limited ability to make informed decisions around which services to provide in a changing environment and where opportunities exist to reduce costs without impacting quality of care. They also will struggle to prepare for and overcome the financial challenges that COVID-19 presents for all organizations — some more severe than others.”

4 steps to adopting a more modern cost accounting approach

How can healthcare organizations advance their cost accounting approach to move at the speed that an ever-changing world requires? The experiences of leading healthcare organizations point to the following lessons learned.

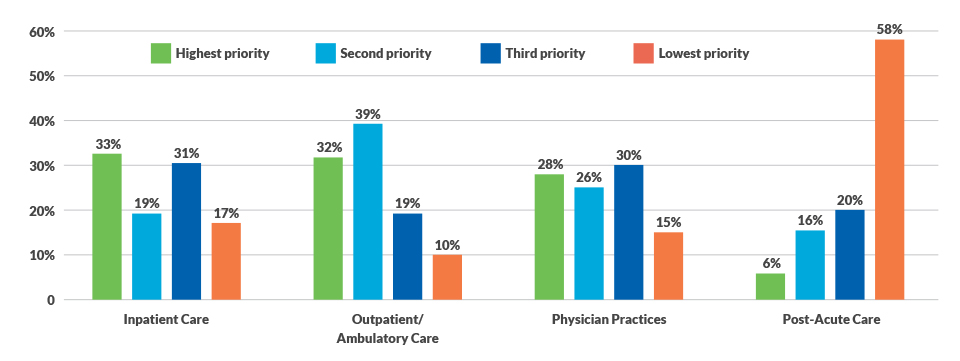

1. Aim to identify the total cost of treatment. Currently, understanding post-acute care costs is a low priority for health systems, even as more value-based payment contracts emphasize post-acute care coordination because of the potential for savings. One health system estimates that comprehensive cost-of-care data will position the organization to link 80% to 90% of its revenue to risk-based contracts — and potentially qualify for value-based incentive payments. It also supports more informed clinical and business decisions that strengthen clinical and financial performance and reputation — critical in an era of consumerism.

“We can really be successful as an organization and drive cost down for the community,” the executive said. “That’s really what our mission is over time: to keep costs in check for the community that we serve.”

Areas of focus for business intelligence investment

In which of the following areas do you most need to focus your business intelligence investment?

Source: HFMA and Strata Decision Technology cost accounting survey, April 2019.

2. Ramp up physician engagement around cost data. One in four organizations surveyed say engaging and including physicians very early in the cost accounting process is key to reducing total costs of care. In one health system, increased communication with physicians around cost-of-care data led to costs that are 15% lower than Medicare costs nationally and a 19% improvement in quality of care for this population. A multidisciplinary committee on cost performance meets quarterly, and communication with physicians varies.

“When we started out with this model, most of our work was with our primary care physicians,” one health system leader said. “Then, we began working with specialty physicians, such as around bundled care for hip and knee replacements. We set a rate for a given service. Initially, there was a lot of variation in costs. Now we are bringing our costs into the middle range and are holding physicians accountable for pre- and post-operative care.”

3. Develop a governance structure to support data gathering and decision-making. “When there is a motivated governance organization, these representatives will have the crucial conversations needed to break through obstacles to cost transparency,” one health system leader said. “If you have loose governance, you may not have those tough conversations with physicians and other stakeholders around cost. Organizations that have a governance structure achieve higher gains.”

Creating transparency into physician performance around cost also is key to success, the leader said.

4. Incorporate feedback from numerous stakeholders. Develop the infrastructure for real-time data sharing, with live support internally or externally, and include stakeholders from clinical, operations and business teams in discussions around bending the cost curve.

“To effectively set up a program like this, you need the business and clinical sides in the room from the get-go,” one leader said. “You need the employer perspective in the room as well.”

All stakeholders should agree on the drivers and incentives for change and how the benefits and risks around cost performance initiatives will be shared. “If you don’t gain alignment from the beginning of the initiative, you could be looking at a restart later,” the leader said.